Learn about “excess deferrals” for those who contributed to both a TSP account and another qualified retirement account last year.

Edward A. Zurndorfer

Almost all federal employees participate and contribute to the Thrift Savings Plan (TSP). In addition to the TSP, some employees also participate in other qualified retirement plans including 401(k), 403(b), and 408(k) qualified retirement plans.

The Internal Revenue Code imposes a limit each year with respect to the amount an employee can contribute (via payroll deduction) in total to all qualified retirement plans during the calendar year. For the year 2021, this annual limit (called the IRS’ “elective deferral limit”) was $19,500. If an employee was over age 49 as of Dec. 31, 2021, the employee was eligible to contribute (also via payroll deduction) an additional $6,500 in “catch-up” contributions.

This column discusses what happens in the event a federal employee contributed during 2021 in total to both the TSP and to another qualified retirement more than the $19,500 ($26,000 if the employee was over age 49 as of Dec. 31, 2021). According to the Internal Revenue Code, the employee made “excess deferrals”.

It is important to mention that contributions made during the year to contributory Individual Retirement Arrangements (IRAs) are not included as part of quailed retirement plan deferrals. IRAs have their own annual contribution limits (during 2021, the IRA contribution limit was $6,000 for individuals younger than age 50 as of Dec. 31, 2021, and $7,000 for individuals over age 49 as of Dec. 31, 2021). A recent FEDZONE column entitled “Remedies for Federal Employees Who Made Excess Contributions to Their IRAs During 2021” discusses the consequences and remedies for making excess contributions to IRAS.

Two scenarios are presented in which a federal employee could have exceeded the 2021 elective deferral amount of $19,500 ($26,000 if the employee was over age 49 as of Dec. 31, 2021). The first scenario is the case of a federal employee who contributes to a civilian TSP amount and to uniformed services TSP account. The second scenario is the case of a federal employee who contributes to the TSP and to another qualified retirement plan (such as a 401(k) qualified retirement plan).

Scenario #1. Federal employee in the same year contributes to both the civilian TSP and to the uniformed services TSP account.

A federal employee is eligible to contribute the maximum amount allowed to the TSP. For 2021, the maximum amount allowed was $19,500 for employees younger than age 50 as of Dec. 31, 2021; $26,000 for employees over age 49 as of Dec. 31, 2021. Note for FERS-covered employees who receive an automatic 1 percent of SF 50 salary contribution and matching contributions (maximum 4 percent) from their agencies, the agency automatic 1 percent of SF 50 salary and agency matching contributions are not part of the $19,500 or $26,000.

Employee TSP contributions include those made via payroll deduction to the traditional TSP and to the Roth TSP, or in combination to both TSP accounts. The amount that a federal employee contributed to the traditional TSP during 2021 will appear on the employee’s 2021 W-2 statement Box 12 (Code D). The amount that the employee a federal employee contributed to the Roth TSP during 2021 will appear on the employee’s 2021 W-2 statement Box 12 (Code AA).

A federal employee could have also contributed during 2021 to a uniformed services TSP account. For example, during 2021 a federal employee who serves in the Ready Reserves was called up for active duty. While serving on active duty during 2021, the employee contributed to his or her uniformed services TSP account. When the employee returned to federal service, the employee contributed to his or her civilian TSP account.

During January 2022, the TSP Service Office will check to see whether the employee’s combined contributions to their civilian TSP account and to their uniformed services TSP account exceeded the IRS’ 2021 “elective deferral limit”. To do so, the TSP will add the traditional TSP and Roth TSP contributions made to both accounts, as shown on the employee’s civilian 2021 W-2 statement and uniformed services 2021 W-2 statement. The TSP will then return any contributions that exceeded the annual elective deferral limit, along with attributable earnings on those contributions. The TSP will do this before April 15, 2022. The employee need not take any action, including filing Form TSP-44 (Request for Refund of Excess Contributions).

Excess elective deferrals and their associated earnings in the uniformed services TSP account will be returned before any elective deferrals and associated earnings in the civilian TSP account are returned.

Scenario #2. During the same year, a federal employee contributes to both the TSP and to a qualified retirement plan sponsored by a private employer.

Consider the example of an individual who retired from federal service during 2021, say June 30, 2021. Prior to retiring from federal service, the individual contributed the maximum possible to the TSP during 2021 – $26,000 ($19,500 in regular contributions and $6,500 in “catch-up” contributions because the individual was over age 49 as of Dec. 31, 2021).

Shortly after retiring from federal service, the individual started employment in a private industry job and contributed to the employer-sponsored 401(k) plan during the period July 1 through Dec. 31, 2021. The individual did not realize that he or she could not contribute anything to the 401(k) plan during the remainder of 2021. This is because the individual had already contributed during 2021 the maximum possible $26,000 to the TSP. In fact, the individual contributed another $19,500 to the company 401(k) plan because of the rather generous 10 percent employer matching 401(k) contributions.

In January 2022, the employee received a 2021 W-2 from his federal agency showing $26,000 of elective deferrals to the traditional TSP. The individual also received a 2021 W-2 from their private industry employer showing elective deferrals of $26,000 during 2021. The employee exceeded for 2021 the elective deferral limit of $26,000 and will need to request a refund of excess deferrals – either from his or her TSP account or from his or her 401(k) account.

The employee elects to request a refund of $26,000 from his TSP account because the TSP matching contributions from the employee’s federal agency were 4 percent, whereas the private employer matching contributions totaled 10 percent.

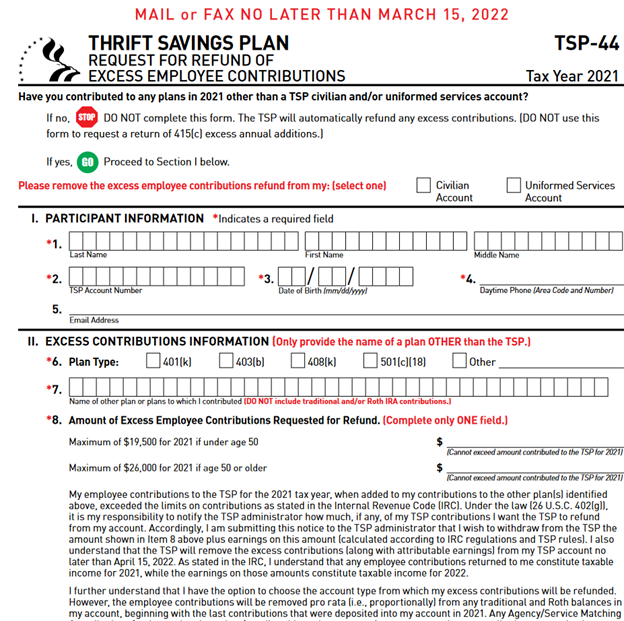

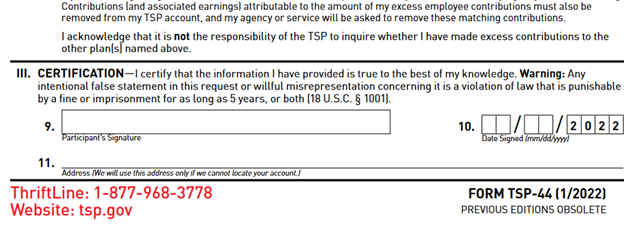

How the TSP Refund Process Works Every January the TSP attaches Form TSP-44 (Request for Refund of Excess Employee Contributions) to the TSP Fact Sheet “Annual Limit on Elective Deferrals”. The fact sheet can be downloaded here. A copy of Form TSP-44 is shown here:

Form TSP-44 is filled out by a TSP participant who made excess deferrals during the previous year. Once completed, it is either mailed or FAXED to the TSP Service Office for processing. If submitted in a timely manner, the TSP will return the excess deferrals and associated earnings to the TSP participant.

To request a refund of excess deferrals and associated earnings, a TSP participant must submit the most recent version of Form TSP-44 as previous year versions are obsolete and will not be processed. To know whether a TSP participant has the most recent version of Form TSP-44, the participant needs to look at the upper right-hand corner of Form TSP-44 (under the form name) which says “Tax Year _ _ _ _”.

In the example above, in which an individual contributed the maximum $26,000 to the TSP for the year 2021 before retiring from federal service and then contributed another $26,000 to a 401(k) qualified retirement plan, the individual will need to complete and submit the Form TSP-44 which has “Tax Year 2021” under TSP-44 in the upper right-hand corner, as illustrated on the form above.

Form TSP-44 must be faxed or postmarked and mailed to the address provided on the form no later than March 15 of the year after the excess deferrals were made. The TSP will then process the refund by April 15. Note that the TSP will remove Form TSP-44 on its Web site after March 15.

Tax Consequences of Contributing More than the Elective Deferral Limit in Any Tax Year

Excess deferrals are treated as income in the year in which the employee made the contributions, whether or not the contributions are refunded to the employee. The total amount of deferred income is reported on the employee’s Form W-2.

Employees who have made traditional TSP account excess deferrals must report the total amount of the excess on their individual income tax return as taxable wages for the year in which the employee made the excess deferrals. Roth excess deferrals are also taxable wages for the year in which an employee made the excess deferrals. However, the amount that the employee contributed to his or her Roth TSP account is already included as income in Box 1 on the employee’s Form W-2.

An employee or retiree who elects to receive excess deferrals as a refund from the TSP will receive IRS Form 1099-R (Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.), which will indicate the amount of the excess deferrals refunded to the employee or annuitant. The distribution will also be reported to the IRS. An employee or annuitant who has filed his or her individual tax return for the year in which the excess deferrals were contributed and this amount was not included as taxable, wages will need to file an amended tax return.

Treatment for Tax Purposes of the Earnings on Excess Deferrals

Earnings distributed with excess deferrals are considered taxable income in the year the earnings are distributed. This is unlike the excess deferrals themselves, which are considered taxable income in the year they are contributed. If there are Roth contributions as part of excess deferrals, the Roth TSP participant will owe tax on the Roth TSP earnings as well. This is the case if the Roth TSP participant meets the IRS requirements to receive Roth earnings tax-free.

The TSP participant will receive a separate IRS Form 1099-R indicating the amount of the earnings. The amount shown on the 1099-R must be reported as income in the year in which the distribution of earnings is made.

What Happens to Agency Matching Contributions for FERS Employees that were Associated with Excess Deferrals that were Returned to the FERS Employee?

A FERS employee’s agency will be notified that the employee has requested to have excess deferrals and associated earnings returned to the employee. The agency is then required to remove the agency matching contributions associated with these excess deferrals. If the agency fails to remove the agency’s matching contributions within one year of the date the contributions were made, then the TSP will remove them and use them to offset TSP administrative expenses.

Other items related to a distribution of TSP excess deferrals:

- If the distribution of TSP excess deferrals is made by April 15 of the tax year in which the excess deferrals were made, it will not be considered an early withdrawal subject to the IRS’ early withdrawal penalty.

- In the event the distribution of TSP excess deferrals is not made by April 15 of the following year, then: (1) The distribution will remain in the account; and (2) if the distribution is traditional (before-taxed TSP), the TSP participant will be taxed twice on the distribution – once in the year in which the excess deferrals were made, and then again when the excess deferrals are withdrawn. If the distribution is composed of Roth contributions (after-taxed) then the excess deferrals will not be treated as after-taxed contributions. This means that the double-taxation rule previously mentioned for the traditional TSP will also apply to excess Roth contributions. The Roth TSP participant will also owe taxes on the earnings attributable to the excess Roth TSP contributions, even if the Roth TSP participant already meets the qualified distribution requirements.

Contribute to 401k and TSP, excess deferrals

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.