Learn about excess contribution penalties and instructions on how to submit a correction to the IRS.

Edward A. Zurndorfer

Those individuals who made excess contributions to their IRAs for the year 2021 have until Monday, October 17,2022 to correct their excess contributions and not be subject to the IRS’ “excess contribution” penalty. The IRA “excess contribution” penalty is equal to 6 percent of the amount of the excess contribution. This column discusses what an excess contribution penalty is and how the penalty can be avoided.

What Is an IRA “Excess Contribution” Penalty?

The following are three examples of excess contributions to an IRA: (1) An individual made a Roth IRA contribution for 2021, but the individual’s modified adjusted gross income (MAGI) for 2021 was too high, resulting in the individual being ineligible to contribute to a Roth IRA for 2021; (2) An individual contributed to an IRA for 2021 and did not have any earned income either himself or herself, and if married, his or her spouse had no earned income during 2021; and (3) An individual contributed to an IRA more than the permitted amount, which for the year 2021 is the lower of: (a) $6,000 (if younger than 50 as of December 31,2021) or $7,000 (if older than age 49 as of December 31, 2021) and (b) the individual’s 2021 earned income (salary, wages or net-self-employment income).

What is the Importance of the October 17,2022 Deadline?

When it comes to correcting an IRA excess contribution for 2021, the key deadline is October 17, 2022. The statutory deadline is actually the tax-filing deadline including extensions for 2021 federal income tax returns. The IRS has said that the applicable deadline for individuals who file a timely individual tax return is six months after the original due date for filing the tax return, even if a filing extension was not filed. The original due date for filing 2021 federal income tax returns was April 18, 2022. This year, October 15th is on a Saturday; therefore, the deadline is the next business day, Monday, October 17,2022.

The October 17,2022 deadline is important because a 6 percent penalty applies to IRA excess contributions. This penalty is not a once-and-done penalty. The penalty applies every year that an excess contribution remains in the IRA. The only way to avoid the penalty is to correct it by the deadline.

Complimentary Webinar featuring Ed Zurndorfer:

The following are two examples of IRA excess contributions and the resulting 6 percent penalty if not corrected by the October 17,2022 deadline:

Example 1. Eric, age 55, single and a federal employee, had a 2021 modified adjusted gross income of $175,400. Eric contributed the maximum $7,000 to his Roth IRA during 2021. The modified adjusted gross income for single tax filers to contribute to a Roth IRA during 2021 is $140,000. Since Eric’s 2021 modified adjusted gross income was $175,000, Eric is not eligible to contribute to a Roth IRA. He therefore made a $7,000 excess IRA contribution and is subject to an excess contribution penalty of 6 percent of $7,000, or $420 unless he corrects the excess IRA contribution no later than October 17,2022. The $420 penalty applies every year that the $7,000 remains in Eric’s Roth IRA.

Example 2. Daniella, age 45, single and a federal employee, owns two IRAs. One IRA is a nondeductible traditional IRA which has no modified adjusted gross income limitation for contribution purposes. The other IRA is a Roth IRA which does have a modified adjusted gross income limitation. During 2021 Daniella’s modified adjusted gross income was $132,500 which according to the worksheets in IRS Publication 590-A (Individual Retirement Arrangements – Contributions) allows her to contribute a maximum $3,000 to her Roth IRA for 2021.She contributed $3,000 to her Roth IRA for 2021. She also contributed $6,000 to her nondeductible traditional IRA for 2021. The total of both IRA contributions for 2021 was therefore $3,000 plus $6,000, or $9000. The $9,000 total contribution exceeds the limit of $6,000 by $3,000. If Daniella does not correct the excess $3,000 IRA contribution by October 17, 2022, she will be subject to an IRA excess contribution penalty of 6 percent of $3,000, or $180. The $180 penalty applies every year that the $3,000 remains in either Daniella’s nondeductible traditional IRA or Roth IRA.

How To Fix an IRA Excess Contribution

When an IRA excess contribution is discovered before the deadline (this year October 17,2022 for 2021 IRA excess contributions), the IRA owner has two choices with respect to fixing the error and avoiding the 6 percent penalty, namely: (1) Recharacterizing the contributions; or (2) Withdrawing the contribution. With either choice when completely successfully, the “slate is wiped clean,” and the excess contribution is treated as though it was never made to the IRA in which the excess contribution occurred.

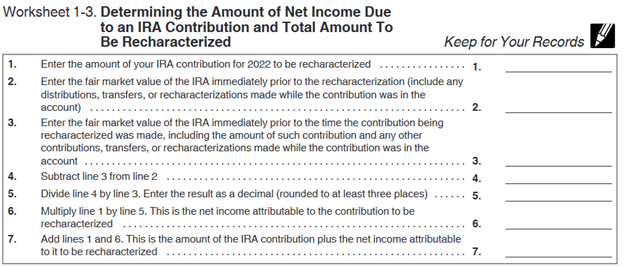

In addition, with either a recharacterization or a withdrawal, the net income attributable (NIA) to the IRA excess contribution must accompany the excess contribution amount. The NIA can be a loss (nondeductible) if the IRA has lost value. The calculation of the NIA is based on the entire value of the IRA during the period in which the excess contribution was in the IRA. The NIA is calculated using a special IRA-approved formula. Some IRA custodians will perform the NIA calculation. A worksheet with the formula to calculate the NIA can be found in IRS Publication 590-A (Individual Retirement Arrangements – Contributions). The worksheet from the 2021 IRS Publication 590-A is reproduced here:

More information on the recharacterization and withdrawal options is presented:

• Withdrawal. This option is only available to nondeductible traditional IRA and Roth IRA excess contributions. It is important for an affected IRA owner to notify his or her IRA custodian that the requested withdrawal is for a return of excess contributions made to a nondeductible traditional IRA or to a Roth IRA. The withdrawal of the IRA contributions is not taxable income (because with both the nondeductible traditional IRA and the Roth IRA contributions were made with after-taxed dollars) but any income associated with a positive NIA that is taxable in the year received. If the IRA owner is younger than age 59.5, then the amount of the positive NIA would also be subject to the 10 percent early withdrawal penalty with no exception. The IRA custodian will use special reporting on Form 1099-R to reflect the fact that the withdrawal is a corrective distribution before the deadline (October 17,2022).

• Recharacterization. Recharacterization is a way to move an unwanted IRA contribution from a traditional IRA to a Roth IRA, or vice versa. If an IRA contribution is recharacterized, it will move from one type of IRA to another type of IRA in a reportable but not taxable transfer. The contribution will be treated as though it had originally been made to the IRA which it is recharacterized.

Those individuals who think that they may have made an IRA excess contribution for 2021 have less than one week to correct the excess contribution. The situation associated with an IRA excess contribution and how to correct the excess contribution can be complex. It is therefore highly recommended that a tax professional be contacted as soon as possible for additional guidance and the specific steps to be followed in order to properly return any IRA excess contributions in the least costly and most efficient way.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.