Tax season is now in full swing. This article breaks down the federal taxation of federal government pensions – both FERS and CSRS.

Edward A. Zurndorfer

Both a CSRS/CSRS Offset and FERS employees make nondeductible contributions to their respective retirement systems. Each pay period, an employee contributes to his or her retirement system via payroll deduction. A portion of the employee’s after-tax salary is contributed. The following table summarizes how much an employee contributes on an after-tax basis:

Employee Contributions to the CSRS or the FERS Retirement and Disability Fund

| Retirement System | Percentage of After-Taxed Salary Contribution |

| CSRS | 7.0% |

| CSRS Offset | 0.8% |

| FERS (hired before 1/1/2013) | 0.8% |

| FERS-RAE (hired during 2013) | 3.1% |

| FERS-FRAE (hired after 12/31/2013) | 4.4% |

No-Cost Webinars, ft. Ed Zurndorfer:

Rules for CSRS/CSRS Offset and FERS Retirees

CSRS/CSRS Offset and FERS employees who retire on a non-disability retirement go by the following rules with respect to how much of their CSRS or FERS annuity is federally taxed:

First, some important terms related to employees once they have retired from federal service:

- Annuity statement. The statement that a recently retired federal employee receives from the Office of Personnel Management (OPM) Retirement Office shows the commencing date, the annuity starting date, the gross monthly rate of the annuity benefit, and the recently retired employee’s Total CSRS or FERS contributions to the CSRS or FERS Retirement and Disability Funds, respectively. Since these contributions (see table 1 above) were made with after-taxed dollars, these contributions represent the retired employee’s “cost” in the retirement. The total contributions are reported to the retired employee and will be recovered by the retiree, tax-free, throughout retirement.

- Gross monthly rate. This is the amount that a recently retired employee will receive after any adjustment for electing a survivor’s annuity.

- Annuitant’s cost in the CSRS or FERS retirement. A CSRS or a FERS retiree’s monthly annuity payment contains an amount in the retiree’s previously paid income tax. This amount represents part of the retiree’s contributions to the CSRS or FERS retirement plan (see Table 1). Even though the retiree did not receive the money that was contributed to the CSRS or FERS Retirement and Disability Fund, the contribution was included in the, then employee’s, gross income for federal and state income tax purposes in the years it was taken out of the employee’s pay. Included in the employee’s cost in the retirement are deposits, including interest, for military service and temporary (non-deduction) service. Those employees who repaid contributions that the employee had withdrawn from the CSRS or FERS retirement plans earlier in their careers and redeposited the withdrawn funds, with interest.

Recovering an Annuitant’s Cost in the Retirement Tax-Free

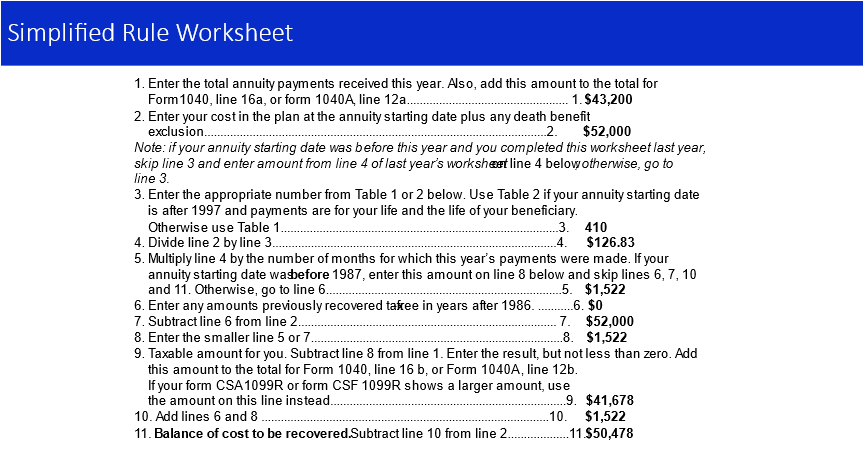

Any employee who retires after November 18,1996 and whose annuity’s starting date is November 19,1996 or later, must use the IRS Simplified Method to calculate the tax-free portion of their CSRS or FERS annuity. The following presents the Simplified Method Worksheet for calculating the taxable amount of CSRS or FERS annuity payments.

Note the following from the Simplified Method Worksheet:

- Line 1 – Total pension or annuity payments received this year. This line is the CSRS or FERS annuitant’s gross annuity payments, received in a particular year. These payments are reported to a CSRS or FERS annuitant, each January, on their CSRS 1099-R. The CSA 1099-R shows the amount of an annuitant’s gross CSRS or FERS annuity that the annuitant received in the previous year, shown in the box entitled “Gross Distribution”.

- Line 2 – investment in the contract (basis) at the annuity starting date. This line represents the CSRS or FESR annuitant’s “cost” in his or her retirement, as explained above under” annuitant’s cost”. Note that OPM’s retirement office reports that amount to a CSRS or FERS annuitant each January on their CSA 1099-R in a box entitled “Total Employee Contributions”.

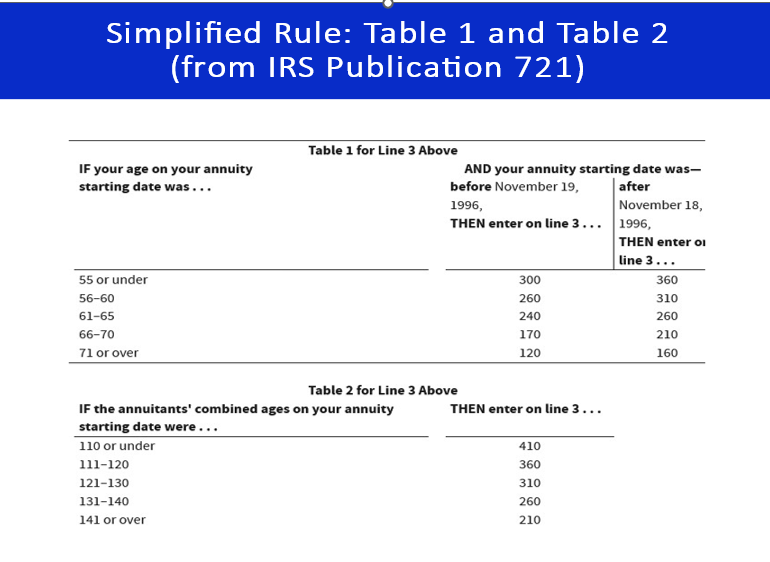

- Line 3. An annuitant must choose a life expectancy factor that depends on the following: (1) the annuity starting date, before November 19,1996 or after November 18, 1996; (2) whether the annuitant is giving a survivor annuity to one person. If the annuitant is giving a survivor annuity to one person, the total of the combined ages of the annuitant and survivor annuitant in the year the annuitant receives his or her first CSRS or FES annuity check; and (3) the age of the annuitant in the year he or she will receive his or her first CSRS or FERS annuity check.

The following example illustrates the Simplified Rule for calculating the taxable portion of a FERS annuity.

Donald, a FERS-covered employee, retired from federal service on November 30, 2021 under an annuity that provides a full 50 percent survivor benefit to his wife, Kathy. Donald’s first annuity check was dated January 1, 2022. Donald uses the Simplified Rule to determine the tax-free portion of his FERS annuity that he received during 2022.

Donald’s monthly FERS gross annuity is $3,000 for a total of 12 months times $3,000 per month or $43,000 during all of 2022. Donald has contributed a total of $52,000 of his after-taxed salary to the FERS Retirement and Disability Fund while in federal service. During 2022, Donald was 56 years old, and Kathy was 54 years old when Donald received his first FERS annuity check.

Donald’s completed worksheet is shown below. To complete line 3 of the worksheet Donald used Table 2 and found the number in the second column opposite the age range that includes 110 (his age during 2022 of 56 plus Kathy’s age of 54 during 2022 which equals 110). Donald keeps a copy of the complete worksheet for his records. It will help him and Kathy to determine the taxable amount of the survivor annuity in the event Donald predeceases Kathy.

Note the following from Donald’s Simplified Rule worksheet:

- The taxable portion of Donald’s FERS annuity for the year 2022 is $41,678, as shown on line 9.

- The difference between the gross annuity ($43,200) and the taxable annuity ($41,678) or $1,522 represents the amount that Donald is receiving each year that is a return of his $52,000 that he contributed on an after-tax basis via payroll deduction to the FERS Retirement and Disability Fund while he was in federal service.

- The $1,522 – the annual return of Donald’s FERS contributions – does not change from one year to the next, even when the FERS annuity is receiving cost-of-living adjustments (COLAs).

- The $52,000 total contribution that Donald made to the FERS Retirement and Disability Fund will be recovered by Donald over a period of 410 months (see line 3 of the worksheet). Dividing $52,000 by 410 is $126.83 (line 4 of the worksheet) which means that Donald will recover $126.83 of his $52,000 contribution each month. If he lives and recovers 410 FERS annuity payments he would recover his entire cost in his retirement. But if he dies before that 410 month, then the same $126.83 “recovery of cost”, will be deducted from Kathy’s 50 percent survivor annuity until it is recovered in full.

You Might Also Enjoy This Podcast:

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.