Here are the options for reversing a social security benefits claiming decision and their consequences

Edward A. Zurndorfer–

Throughout much of the 2.5 years of the COVID-19 pandemic, many federal employees who were eligible to retire decided to retire. Some of these retirees elected to start receiving their Social Security monthly retirement benefits as early as age 62, resulting in a permanent reduction to their Social Security monthly retirement benefit. Some federal retirees elected not to start receiving their Social Security monthly retirement benefits until they reached their full retirement age (FRA) (age 65 to 67, depending in which year a retiree was born) thereby not incurring any permanent reduction to their Social Security monthly retirement benefit.

With rampant inflation over the past year and a down stock market in which many Thrift Savings Plan (TSP) participants have seen the value of their TSP accounts drop by as much as 20 to 25 percent, some of these early retirees have asked the question whether it is possible to reverse an earlier decision to start receiving their Social Security benefits. They are asking this question because they have been told that if they reverse their earlier decision to start receiving their Social Security monthly benefit, then the reduction they incurred will stop. Furthermore, when they reapply to receive their monthly benefit, their benefit should be higher. In fact, if they then wait until at least their FRA to resume receiving their monthly benefit, then for every year they wait past their FRA until age 70 to resume their monthly retirement benefit, their monthly benefit is guaranteed to increase 8 percent per year.

The answer to these Social Security recipients’ question is yes. It is possible to reverse a previous decision to claim one’s monthly Social Security retirement benefit. There are two options available to reverse a prior claiming decision. One option is called a withdrawal and the other option is called a suspension. Both options are discussed and explained including specific rules and consequences.

No-Cost Webinar featuring Ed Zurndorfer:

Withdrawing a Social Security Benefits Claiming Decision

Under the withdrawal option, an individual who elected to receive his or her Social Security monthly retirement benefit at any age can change his or her mind within the first 12 months of claiming their monthly benefit. Once the Social Security participant notifies the Social Security Administration (SSA) of his or her decision to withdraw an earlier claiming decision, the SSA will stop the participant’s monthly benefit. The monthly benefit will resume only when the individual formally applies again to claim his or her monthly benefit.

Like other Social Security options, there are a number of rules and consequences of associated with the Social Security withdrawal option. They are:

- One withdrawal request per lifetime: An individual is allowed to make one Social Security withdrawal request per lifetime.

- Time limit to request a withdrawal. A withdrawal request must be made within the first 12 months of claiming Social Security retirement benefits, at whatever age the individual started receiving benefits (as early as age 62).

- All Social Security monthly retirement benefits previously received must be repaid in the entirety. An individual who requests a withdrawal of Social Security during the first 12 months of receiving the benefits must repay all benefits previously received with no interest charges.

- Options for Reversing a Social Security Benefits Claiming Decision and Their Consequences

- Family benefits will be withdrawn. Any family members such as minor children or a spouse receiving monthly benefits based on the individual’s Social Security retirement benefits will have their benefits stopped and any previous benefits received within the first 12 months must be repaid.

- Repayment of monthly benefits includes federal income taxes and Medicare Part B and Medicare Part D premiums. Besides the amount of the monthly Social Security retirement benefit an individual must repay, any Medicare Part B and Medicare Part D monthly premiums deducted and/or voluntary federal income tax withholding that was deducted from the Social Security beneficiary’s monthly retirement benefit check must be repaid.

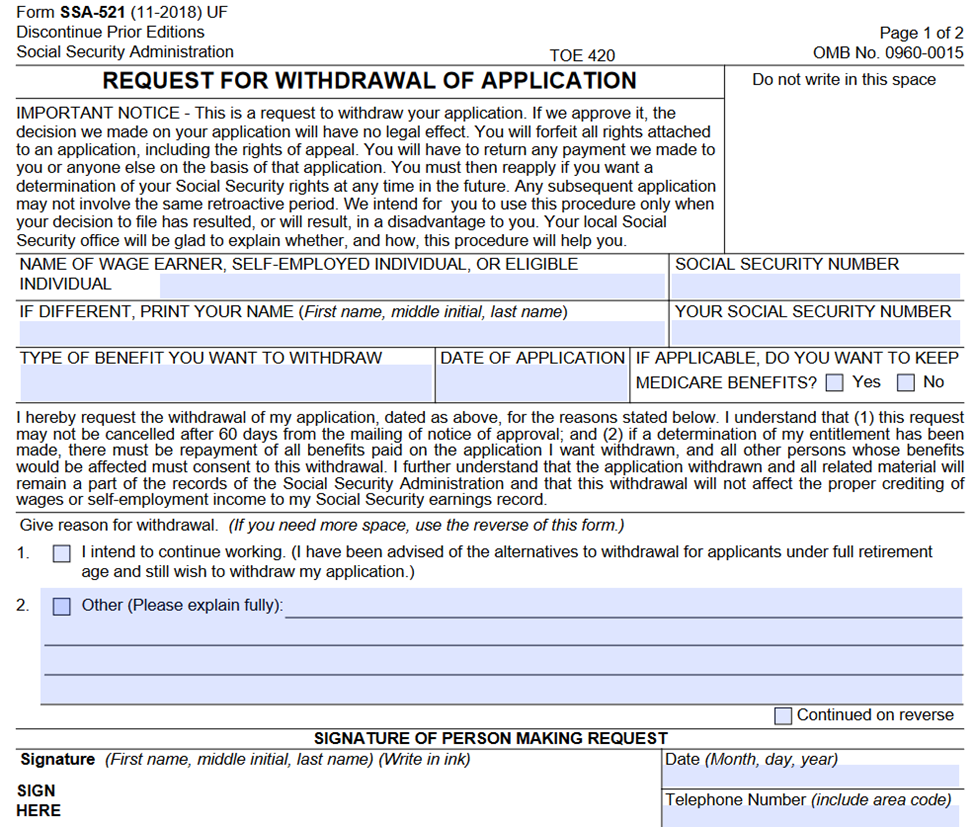

An individual can request a cancellation of claiming Social Security benefits by filling out and submitting Social Security Form SSA-521 (Request for Withdrawal of Application, can be downloaded here.). Once the individual wants to resume receiving his or her monthly retirement benefit, he or she has to go through the usual process of applying for Social Security benefits. The recommended way to reapply for benefits is online.

Individuals eligible for Social Security retirement benefits are reminded that although benefits can be applied for as early as age 62, the benefits are reduced by 25 to 30 percent compared to claiming one’s benefit starting at their FRA. The amount of the reduction depends on an individual’s full retirement age.

There is also a “delayed retirement credit” (DRC) in which an individual who postpones the start of retirement benefits past his or her FRA will receive an increase of 8 percent per year in their monthly benefit for every year postponed until age 70. The difference between claiming benefits as early as age 62 and the maximum age of 70 is a sizeable 76 percent of the individual’s Social Security monthly benefits for life.

Paying Medicare Part B Premiums

Those individuals enrolled in Medicare Part B, (medical insurance) must pay a monthly premium for Medicare Part B. To pay that premium, most Part B beneficiaries have their monthly premium deducted from their monthly Social Security monthly retirement check.

Medicare Part B beneficiaries who decide to withdraw their application for Social Security must clearly state on Form SSA-521 whether they want to keep their Medicare Part B benefits. There is a box on Form SSA-521 to be checked “yes” or “no” indicating whether a beneficiary wants to retain Medicare Part B coverage. If so, then the beneficiary will pay monthly Part B premiums directly to the Centers for Medicare and Medicaid Services. See below for a portion of Form SSA-521.

Suspending a Social Security Benefits Claiming Decision

A Social Security monthly retirement benefit recipient who misses the 12-month window to withdraw his or her application or did not repay his or her benefits in its entirety has another option available to him or to her in order to reverse a prior Social Security claiming decision. It is called suspension of benefits.

Suspension of Social Security retirement benefits can be done if the individual who previously claimed the monthly retirement benefit has reached his or her full retirement age and is younger than age 70. By suspending his or her Social Security monthly retirement benefit, an individual earns delayed retirement credits equal to 2/3 of one percent per month or 8 percent per year starting from the month the individual becomes age FRA and until the month the individual becomes age 70. Monthly retirement benefits will automatically start when the individual reaches age 70. This is unless the individual requests monthly benefits to be reinstated before one’s 70th birthday.

Suspending one’s Social Security monthly benefits has consequences similar to consequences associated with the Social Security withdrawal option including:

- If a Social Security monthly retirement benefit recipient is enrolled in Medicare Part B and suspends the monthly benefit, then the Center for Medicare and Medicaid Services will bill the recipient in order for the “suspended” recipient to pay future Medicare Part B monthly premiums.

- If a Social Security monthly retirement benefit recipient has family members such as a spouse and children who receive monthly benefits based on the recipient’s record, then if the benefits are suspended by the recipient, then all family member monthly benefits will also be suspended. The only exception is a divorced spouse who is able to continue receiving benefits.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.