Social Security Administration and the Internal Revenue Service Announce Benefit and Contribution Limits for 2023

Edward A. Zurndorfer

This column summarizes the 2023 Social Security changes recently enacted by the Social Security Administration (SSA) and the 2023 inflation-adjusted IRA and qualified retirement plan contribution limits. The highest inflation rate in 40 years has resulted in record increases in some retirement plan contribution limits.

2023 Social Security Changes

Based on the increase in the Consumer Price Index (CPI-W) from the third quarter of 2021 through the third quarter of 2022, Social Security beneficiaries will receive an 8.7 percent COLA for 2023. Other important 2023 Social Security are summarized:

| 2022 | 2023 | |

| Maximum Taxable Earnings | ||

| Social Security (FICA Tax) | $147,000 | $160,200 |

| Medicare (Hospital Insurance Tax) | No limit | No Limit |

| 2022 | 2023 | |

| Quarter of Coverage | $1,510 | $1,640 |

No-Cost Webinar ft. Ed Zurndorfer:

Retirement Earnings Test Exempt Amounts

| 2022 | 2023 | |

| Under full retirement age: Note: One dollar in benefits will be withheld for every $2 in earnings above the limit | $19,560/year ($1,630/month) | $21,240/year ($1,770/month) |

| The year an individual reaches full retirement age: Note: Applies to earnings for months prior to the month attaining full retirement age. One dollar in benefits will be withheld fore very $3 in earnings above the limit. | $51,960/year ($4,330/month) | $56,520/year ($4,710/month) |

| Beginning the month an individual attains full retirement age | None | None |

2023 Retirement Plan Contribution Limits

On October 21, 2022, the IRS released inflation contribution limits, phase-out ranges, and income limits for various retirement accounts.

For 2023, the amount an individual can contribute via payroll deduction to defined contribution plans (a 401(k), 403(b), 457 retirement plan or the Thrift Savings Plan) increases to $22,500, an increase of $2,000 from 2022. The “catch-up” contribution amount for employees aged 50 and older during 2023 (employees born before January 1, 1974) increases to $7,500, an increase of $1,000 from the $6,500 catch-up contribution limit during 2022.

For IRAs, the amount an individual can contribute to an IRA during 2023 increases to $6,500, an increase of $500 from the $6,000 contribution limit during 2022. The IRA catch-up contribution limit (for individuals aged 50 aged 50 and older during 2023) remains $1,000. Other important information concerning IRA contributions during 2023:

- The deductible traditional IRA modified adjusted gross income (MAGI) phase-out range for a single individual covered by a workplace retirement plan (such as the TSP) begins at $73,000 and ends at $83,000. This is up from $68,000 and $78,000 respectively during 2022.

- For married couples filing jointly, if the spouse making the traditional IRA contributions is covered by a workplace retirement plan (such as the TSP) the phase-out MAGI range increases to between $116,000 and $136,000. This is up from $109,000 and $129,000 respectively during 2022.

- For an IRA contributor who is not covered by a workplace retirement plan and is married to someone who is covered by a workplace retirement plan, the MAGI phase-out range increases to between $218,000 and $228,000, up from $204,000 and $214,000 respectively during 2022.

- For a married individual filing a separate return who is covered by a workplace retirement plan, the phase-out range is not subject to an annual cost-of-living adjustment and remains between $0 and $10,000.

- The phase-out MAGI ranges for Roth IRA contributions during 2023 are:

- For individuals who file their taxes as single or head of household, the Roth IRA modified adjusted gross income (MAGI) phase-out begins at $138,000 and ends at $153,000. This is up from between $129,000 and $144,000 respectively during 2022.

- •For married couples filing their taxes s married filing jointly, the Roth IRA phase-out range begins at $218,000 and ends at $228,000. This is up from between $204,000 and $214,000 during 2022.

- For married couples filing their taxes as married filing separate, the phase-out range remains at between $0 and $10,000 which is the same as it was during 2022.

No-Cost Webinars ft. Ed Zurndorfer:

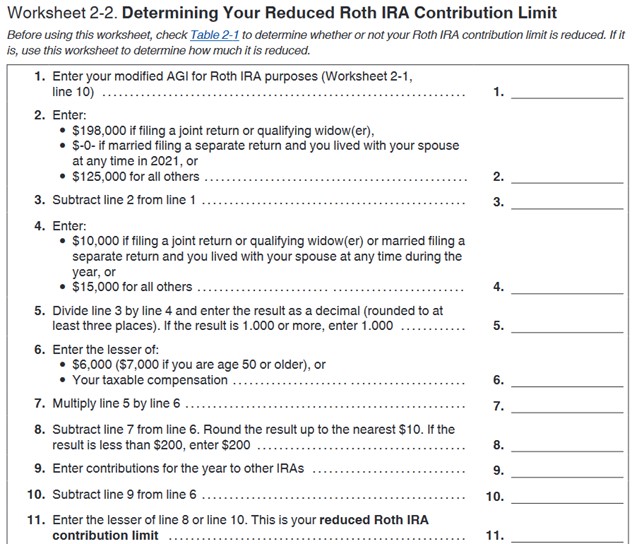

In IRS Publication 590-A (Individual Retirement Accounts – Contributions; may be downloaded here), there are worksheets that allow individuals to calculate how much they can contribute to a Roth IRA based on their Roth MAGI. The following is a copy of the worksheet used to determine how much an individual can contribute to a Roth IRA for 2021:

The nondeductible traditional IRA (in which contributions are not deductible for federal and state income tax purposes) has no income limitations. With the passage of the SECURE Act in December 2019 and effective January 1, 2020, there is also no age limitation for contributing to a traditional IRA, either to a deductible or to a nondeductible traditional IRA. Prior to the SECURE Act passage, there was an age limitation of 70.5 for contributing to a traditional IRA. The Roth IRA has never had and continues to have no age limitations. The one requirement for an individual to contribute to any IRA is that the individual, or the individual’s spouse if married, must have earned income. Earned income includes wages, salary, or net income from self-employment.

Additional information about IRS 2023 inflation-adjusted contribution limits, phase-out ranges, and income limits may be found in IRS News Release IR 2022-188 and IRS Notice 2022-55.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.