While Gathering Documents to Prepare 2020 Income Tax Returns, Employees Are Reminded to Check Their Social Security Statements

Edward A. Zurndorfer –

Like individuals who work in private industry, nearly all federal employees will receive some form of Social Security benefits following their retirement from federal service. Employees who are covered by the Federal Employees Retirement System (FERS) pay into Social Security and will certainly have sufficient years of coverage to qualify for Social Security retirement benefits, starting as early as age 62. Those employees who are covered by the Civil Service Retirement System (CSRS) (and who do not pay into Social Security while they are CSRS employees) and current CSRS annuitants may have accumulated the minimum number of Social Security credits from private industry employment to qualify for Social Security retirement benefits.

The Social Security Administration (SSA) provides individuals a Social Security statement. The statement is called the Personal Earnings and Benefit Estimate Statement (PEBES) and is full of valuable information. Most importantly, the PEBES provides a summary of the Social Security benefits that an individual can expect to receive (in today’s dollars) during retirement or if they were disabled.

The SSA updates a working individual’s PEBES annually. The reason for the update is because as an individual continues to work in Social Security-covered employment, the individual’s future Social Security disability and retirement benefits increase. Individuals are therefore encouraged to view the change of their benefits. They may do so by checking their PEBES and are encouraged to do so at least annually.

It is unfortunate that many individuals are confused as to whether SSA sends them their PEBES or how to obtain their PEBES. That is because the SSA has changed its PEBES distribution policies over the last 20 years.

Starting in 1999, the SSA mailed the PEBES annually to all future Social Security beneficiaries. But these mailings were suspended in 2011 because of budget cuts at the SSA. In May 2012, PEBES mailings were restarted but only for individuals over age 60. Later in 2012, those mailings were suspended.

Currently, the SSA mails the PEBES to individuals over age 60 provided the individuals: (1) Have not filed for Social Security benefits; and (2) have not established an online Social Security account. All individuals are therefore encouraged to set up their own Social Security online account. They may do so by going here. By establishing an online Social Security account, an individual can review his or her PEBES anytime and check the statement for any incorrect entries and information.

What Type of Information is Provided in the PEBES?

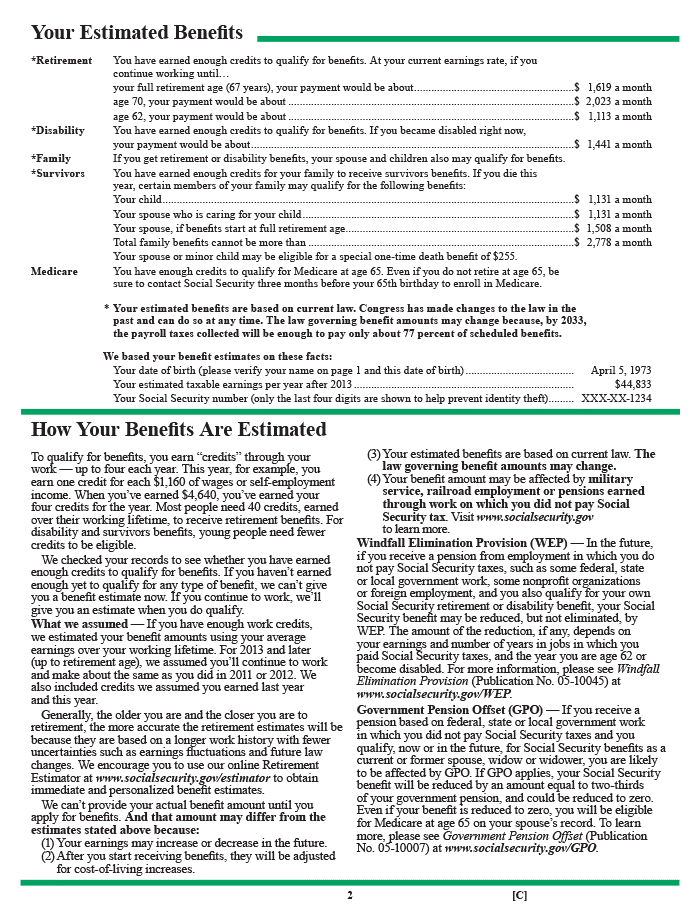

The purpose of the PEBES is to allow an individual to know what his or her future Social Security benefits will be. It is important to understand that the information provided is just an estimate. Future Social Security benefits are provided on page 2 of the PEBES. A sample of the information on page 2 of the PEBES is shown below. The benefits are computed based on an individual’s Social Security earnings history. Page 3 of the PEBES contains the exact yearly Social Security earnings in the SSA records that are used in calculating an individual’s estimated benefits each year.

The first line on page 2 (“Retirement”) is the “primary insurance amount” (PIA) which is the amount of the individual’s monthly Social Security retirement benefit at his or her full retirement age (FRA). FRA depends on the year an individual was born. Any individual born between 1943 and 1954 has an FRA of age 66. Starting with individuals born in 1955, FRA increases by two months (that is, individuals born in 1955 have an FRA of age 66 years and 2 months, individuals born in 1956 have an FRA of 66 years and 4 months, etc.), resulting that any individual born after 1959 has an FRA of 67 years.

The next two numbers shown the FRA amount are the estimated Social Security monthly retirement benefits at age 70 and at age 62, respectively, which are calculated relative to the PIA base number. If an individual is over age 62, there will be listed a “current year” retirement benefit estimate instead of an estimate at age 62.

Below the retirement estimate at age 62 (or current year), are the individual’s estimated Social Security disability monthly benefit in the event the individual becomes disabled. Also listed are “Family” benefits (spouse and children) that would be paid to these eligible family members as well as listed are “Survivor” benefits paid to these eligible family members if the individual were to die. Finally, below “Survivor” benefits is “Medicare” in which it is mentioned whether the individual has enough credits to qualify for Medicare starting at age 65.

It needs to be emphasized that retirement benefits at age 62, FRA and at age 70 shown on page two of the PEBES are only estimates. The following are three important factors that can have an impact on the amount of an individual’s future Social Security monthly retirement benefits: (1) Social Security earnings after age 62. As will be explained, an individual’s Social Security earnings history is crucial in determining an individual’s retirement benefits. Those individuals working past age 62 will have not have any post-age 62 earnings included in those estimates. When these individuals apply for their Social Security retirement benefit, a recalculation of benefits will be made that will consider post-age 62 Social Security earnings, thereby increasing their benefits (2) Cost-of-living adjustments (COLAs). The statement’s estimate does not reflect the impact of future Social Security COLAs; and (3) Public sector employment. Individuals who work in the public sector for federal, state, or local governments in which they do not pay into Social Security (for example, federal employees covered by CSRS will have their Social Security retirement benefits reduced by as much as $300 to $600 a month because of the Windfall Elimination Provision (WEP). The bottom of page 2 of the PEBES explains the two regulations that affect these individuals: namely, the WEP and the Government Pension Offset (GPO). The GPO can result in a total elimination of spousal Social Security benefits that a public sector worker could be eligible for.

An Individual’s Social Security Earnings History is Tantamount in Determining the Individual’s Social Security Retirement Benefit

The SSA calculates an individuals’ Social Security benefits based upon the individual’s 35 highest years of Social Security wages for which the individual paid Social Security (FICA) taxes. Currently, the FICA tax is equal to 6.2 percent of an employee’s wages, deducted from the employee’s gross salary and matched by the employer. The SSA obtains the individual’s Social Security earnings from the individual’s Form W-2 (box 3) each year. Employers send their employees’ W-2 forms to the SSA each year by January 31.

Page 3 of the PEBES lists by years the yearly Social Security earnings in which an individual paid FICA tax. In calculating an individual’s PIA (see above), SSA used the individual’s current 35 highest years of Social Security earnings. Note that the 35 highest years do not have to be consecutive and that Social Security earnings that occurred more than five years in the past are indexed to inflation, in order to bring the calculated benefits into current dollar value.

It is also important to emphasize that the information presented on page 2 of the PEBES, is calculated based on the Social Security earnings history shown on page 3 and is just an estimate. While the SSA has a record of an individual’s earnings and FICA taxes paid up to this point, the SSA does not know what an individual’s future Social Security earnings will be. The benefits estimate as presented assumes that an individual’s Social Security earnings will continue at the same level as it was for the most recent earnings year. If an individual’s future Social Security earnings are higher, that will naturally increase the amount of an individual’s Social Security benefits that will eventually be paid. However, since an individual’s benefits are calculated based on an individual’s 35 highest years of Social Security earnings, no matter when the earnings occurred, it is not equally true that lower future Social Security earnings, or no Social Security earnings, will result in lower benefits.

Individuals are encouraged to check page 3 of the PEBES for accuracy. This is because if Social Security earnings were reported incorrectly by an employer via Box 3 of Form W-2, then Social Security benefits will be reported incorrectly.

In addition to Social Security earnings reported by year on Page 3 of PEBES, Medicare earnings are also reported, as shown in Box 5 of Form W-2. An individual must have at least 10 years of Medicare earnings in order to qualify for Medicare A, Hospital insurance, starting at age 65. Finally, shown on page 3 are the estimated FICA taxes paid by the individual and the individual’s employer during the individual’s working years. The following is an example of the total Social Security and Medicare taxes paid over an individual’s working career through the last year as reported on the wage chart on the top of page 3 of the PEBES.

Total Social Security and Medicare taxes paid over your working career through the last year reported on the chart above:

| Estimated taxes paid for Social Security: | Estimated taxes paid for Medicare: | ||

| You paid: | $88,710 | You paid: | $21,433 |

| Your employers paid: | $91,671 | Your employers paid: | $21,433 |

Note the entry “Estimated taxes paid for Social Security – You paid: $88,710

The $88,710 is the cumulative FICA taxes the individual has paid over his or her work career. On page 2 of this individual’s PEBES (not the page 2 shown above), it states that the individual’s Social Security retirement benefit at his or her full retirement age will be $2,201 per month, or $26,412 annually.

If this individual were to divide the cumulative amount of FICA taxes paid ($88,710) by the amount of the expected annual benefit ($26,412) starting at age 66 years and 2 months, or $88,710/$26,412 per year, the result 3.36 years.

You Might Also Enjoy This Podcast:

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.