Ed Zurndorfer breaks down everything you need to know to prepare for the death of a spouse

Besides the emotional consequences of a spouse’s death, particularly if the death was sudden and unexpected, there can be some devastating financial consequences to the surviving spouse. This column reviews some of the steps that married couples should take in order for the surviving spouse to be financially prepared when the first spouse dies.

Consider a retired married couple, in which one spouse was a federal employee, now a federal annuitant, and the other spouse worked in private industry and is also retired. Both spouses are covered by Social Security. The spouse who was a federal employee was covered by the Federal Employee Retirement System (FERS), covered by Social Security, and contributed to the Thrift Savings Plan (TSP) The spouse retired from federal service and is receiving a FERS annuity. The spouse who was a federal employee also carries the health insurance (Federal Employees Health Benefits program) (FEHBP) that insures both the annuitant and the annuitant’s spouse. The other spouse worked in private industry and may be covered by an employer-sponsored retirement plan such as a 401(k) or 403(b) retirement plan. The other spouse is eligible for their own Social Security benefits. The spouse with the FERS annuity has chosen a full FERS survivor annuity benefit for the spouse. Among the reasons for choosing a full (maximum) survivor annuity is so that the surviving spouse can retain the FEHB health insurance and be able to afford the FEHBP premiums (self-only health insurance premiums (which are deducted from a spouse’s survivor annuity).

Both spouses are retired and are collecting their own Social Security retirement checks. The spouse who is a federal annuitant is also collecting a FERS annuity check and perhaps withdrawing from the TSP. The other spouse is perhaps collecting from his or her 401(k) or 403(b) retirement plan or IRAs, or both.

The spouse receiving the FERS suddenly dies. The full FERS annuity stops, and the surviving spouse applies for his or her 50 percent FERS spousal survivor annuity. The deceased spouse’s (the FERS annuitant’s) Social Security monthly retirement benefit stops.

Although the income of the surviving spouse is most likely lower compared to what it was when the other spouse was alive, the surviving spouse will usually be hit with a higher tax bill, starting the year after the spouse dies. That is because the surviving spouse will be filing as single (instead of married filing jointly) and higher marginal tax brackets kick in at lower income levels for single individuals. Also, if the surviving spouse decides to continue working or to go back to work, there is a certain amount of income the surviving spouse can earn so as not to push him or her into a higher marginal tax bracket.

Additional Tax Issues Related to the Death of a Spouse

A surviving spouse will potentially have additional tax-related issues to deal with upon the death of their spouse. One potential issue that may be overlooked that could cause problems during the preparation of the deceased spouse’s final tax return is related to “tax carryovers”. Note that as indicated above, in the year that the spouse died, the surviving spouse can still file as married filing joint. But that is the last year. Starting the year after spouse died, the surviving spouse must file as “single”.

“Tax carryovers” include any capital losses incurred solely by the deceased spouse in the year of death and charitable contributions made solely by the deceased spouse in the year of death. What should be done with these capital losses and the charitable contributions that were in the deceased spouse’s name only? What should be done with them in the year of death? Can the capital losses and charitable contributions be carried over to the subsequent year of death and beyond?

The answer is that “tax carryovers” have to be included on the decedent’s final income tax return (the tax return (the year in which the spouse died which is the last year that the couple can file as married filing joint). The capital losses and charitable contributions cannot be used on future year income tax returns. This is relatively easy to understand when a single individual dies. What is not used on the decedent’s final income tax return will simply “be lost”.

It is a little more complex for a married couple filing jointly when the first spouse dies. In the year of death, the surviving spouse can still file as married filing jointly. This means any capital losses that the deceased spouse incurred (on capital assets held solely in the deceased’s name) during that year the surviving spouse can use (to offset capital gains incurred by the deceased spouse, the surviving spouse, or both with capital assets held jointly), and any charitable contributions made by the deceased spouse during that year can be added to the surviving spouse’s charitable contributions made during that year. But any of the spouse’s capital losses not used and charitable contributions made during that year and not added to the surviving spouse’s charitable contributions for that year will be permanently lost. This is because starting in the year following the death of the spouse the surviving spouse must file as single.

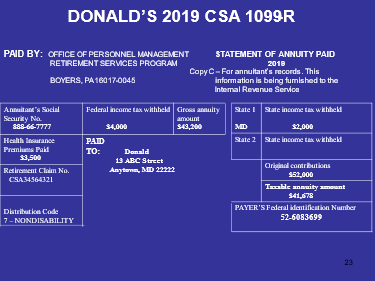

Another tax issue that will affect a surviving spouse of a deceased federal annuitant involves the taxation of a CSRS or a FERS spousal survivor annuity. A CSRS or a CSRS Offset annuitant (receiving a CSRS annuity) and FERS annuitant (receiving a FERS annuity) is not taxed on the full portion of the CSRS and FERS annuity. CSRS/CSRS Offset employees and FERS employees contribute each pay period of portion of their salary to the CSRS and FERS Retirement and Disability Funds, respectively. These employee contributions: (1) Are made with after-taxed dollars; and (2) are returned to the retired employee as part of their CSRS and FERS annuities, respectively. Because the contributions were made with after-taxed dollars, that portion of CSRS and FERS annuitant’s monthly annuity check that is a return of their contributions will not be taxed. It is OPM’s Retirement Processing Office that determines each year how much of a CSRS/CSRS Offset annuitant’s annuity check and a FERS annuitant’s annuity check is taxable. OPM’s Retirement Processing Office does this using the IRS’ Simplified Rule. Consider the following example of Donald, a FERS annuitant who retired from federal service on November 30, 2018 and received a gross monthly FERS annuity of $3,600 starting January 1, 2019 and throughout 2019. Below is a copy of Donald’s 2019 CSA 1099R that he received from OPM in January 2020:

Note the following:

- Donald’s gross annuity amount equals $43,200 (12 payments of $3,600 each)

- Donald’s taxable annuity amount equals $41,678

- Donald contributed $52,000 from his after-taxed salary to the FERS Retirement Fund

- The difference between Donald’s gross annuity and Donald’s taxable annuity is $43,200 less $41,678, or $1,522. The $1,522 is part of the already taxed $52,000 that Donald contributed to the FERS Retirement. Each year, the $1,522 will continue to be subtracted from Donald’s gross annuity until the full $52,000 is paid back. This will take $52,000/$1,522 or approximately 33 years. If Donald lives for at least 33 years after his retirement, then once he reaches the 33-year point he would have received all $52,000, and at that point, his FERS annuity would be fully taxable.

- If Donald dies any time before reaching the 33-year point, then the $1,522 return of his FERS contributions will be subtracted to the FERS survivor spousal annuity that he is giving to his wife Kathy.

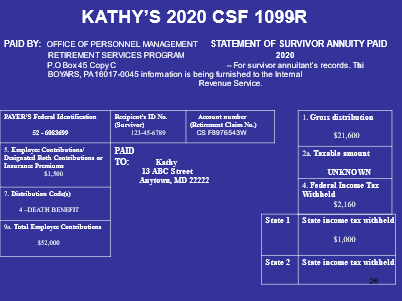

Unfortunately, Donald died suddenly on December 19, 2019. He had elected to give a 50 percent FERS spousal survivor annuity benefit to his wife Kathy. Because Donald died on December 19, 2019, Kathy received her first FERS survivor annuity check of $1,800 (50 percent of $3,600, which Donald was receiving at the time of his death) on Jan. 1, 2020, and throughout 2020. Kathy, therefore, received 12 monthly survivor gross annuity amounts of $1,800 during 2020 for a total of $21,600. OPM issued her a CSF 1099R for 2020 which is shown below:

Note the following:

- Kathy’s gross distribution (Box 1) equals $21,600 (12 payments of $1,800 each)

- Kathy’s taxable amount (2a) is shown as UNKNOWN

- Donald’s employee of contributions $52,000 from his after-taxed salary to the FERS Retirement Fund are shown in Box 9a.

As explained above, the $1,522 (return of employee contributions which has already been taxed) which was subtracted from Donald’s FERS gross annuity should have been subtracted from Kathy’s FERS survivor annuity. This is because Donald died before he reached the 33rd anniversary of his retirement from federal service. Kathy’s “taxable amount” in Box 2a should have been therefore $21,600 less $1,522, or $20,078.

As a rule, OPM’s Retirement Office (which issues the survivor annuitant’s CSF 1099R) does not compute the taxable amount of the survivor annuity (Box 2a of the CSF 1099R). This is not good, because many survivor annuitants (and/or their tax preparers) will assume that the gross distribution is fully taxable when in reality it is not fully taxable. The result has been that many spousal survivor annuitants have overpaid their federal and state income taxes through the years.

OPM does in fact know what the taxable portion of the survivor annuity is but refuses to show it. Survivor annuitants (and/or their tax preparers) have to know the annual dollar amount of the difference between the CSRS or FERS annuitant’s gross annuity and CSRS or FERS’s taxable annuity and apply that same difference to the CSRS or FERS spousal survivor gross annuity in order to determine the spousal survivor taxable annuity.

Estate Tax Return

A surviving spouse may have to file a federal estate tax return (Form 706) and/or state estate tax return which includes gathering asset and debt related information. They may need to work with an estate attorney for probate of the estate or transfer of estate assets.

Assets held jointly with the deceased spouse will need to be retitled solely in the name of the surviving spouse. These assets include checking and savings accounts, credit union accounts, brokerage accounts, and other investment accounts.

Sale of Principal Residence

A married couple who sells their principal residence and incur a capital gain are allowed to exclude from their taxable income up to $500,000 in the year of sale. To do so, at least one of the spouses must have owned the principal residence and both spouses must have lived in the principal residence for at least two of the five years, ending on the day the principal residence is sold. To exclude the maximum $500,000 of capital gain from taxable income, the spouses must file in the year of sale as married filing joint.

The $500,000 capital gain exclusion that applies to individuals filing as married filing joint tax return also applies to unmarried surviving spouses if the sale of the principal residence occurs within two years of the death of their spouses. If more than two years passes after the death of first spouse, then the surviving spouse will be entitled to a maximum $250,000 capital gain exclusion upon the sale of personal residence. The following example illustrates:

Howard and Wendy are married and have owned and used their principal residence since February 1, 2008. Howard was a federal retiree and died on March 31, 2020. Wendy inherited Howard’s interest in their jointly owned residence. If Wendy sells the principal residence before March 31, 2022, she will qualify for the $500,000 capital gain exclusion. If Wendy sells the residence any time after March 31, 2022, she will qualify for the $250,000 capital gain exclusion.

Financial Impact of a Spouse’s Death May Last for Years

The financial impact of a spouse’s death often is not clear for years. A surviving spouse has several financial issues that need to be addressed. Surviving spouses of federal annuitants need to consider and take appropriate action on the following:

1. Report the death of the spouse. This is done by completing the online form, Report the Death of a Retiree or Survivor Annuitant, which can be found here. The spouse needs to apply for his or her survivor benefits (survivor annuity, health, dental and vision benefits) by completing Form SF 2800 (Application for Death Benefits -CSRS) or Form SF 3104 (Application for Death Benefits-FERS). Both of these forms can be downloaded at www.opm.gov/forms.

2. Make a claim for FEGLI life insurance benefits if the deceased annuitant was insured under FEGLI. If the deceased owned an individual life insurance policy with a private insurance company, the surviving spouse needs to file a claim for with the private insurance company.

3. Make a claim for TSP benefits. Upon the death of a TSP participant, a representative of the estate (Executor or Trustee) needs to complete and submit Form TSP-17 (Information Relating to Deceased Participant). Form TSP-17 is used to provide information about potential beneficiaries of the deceased TSP participant. If the surviving spouse is a beneficiary, the question is what the spouse should do with the inherited TSP account. One option is to leave it in the TSP.

4. Social Security benefits. A deceased CSRS annuitant and more likely a deceased FERS annuitant was eligible for or receiving Social Security retirement benefits. If the surviving spouse is eligible for his or her own Social Security benefits, the surviving spouse needs to decide whether to continue receiving his or her benefit or instead apply for the full amount of their deceased spouse’s Social Security (widow/widower) benefit

5. Taxes and Medicare Part B. The surviving spouse is highly encouraged to speak with a qualified tax accountant regarding future federal and state tax liabilities as a result of their spouse’s death. Starting in the year after the spouse’s death, the surviving spouse must file as single.

Another issue is Medicare Part B. Medicare Part B premiums are determined each year on one’s modified adjusted gross income from two years ago. Even though the surviving spouse’s income will be reduced as a result of the spouse’s death, the surviving spouse will be subject to the lower single filing Medicare Part B income brackets. In addition, if the surviving spouse is the sole beneficiary of the spouse’s TSP account, when added to the surviving spouse’s own qualified retirement accounts and/or traditional IRAs, the result will be larger required minimum distributions (RMDs). This will add to the surviving spouse’s income with the likely result of additional taxes and higher Medicare part B premiums.

6. Possible future long-term care. Is the surviving spouse prepared for possible long-term care? Does the spouse own any long-term care insurance? If not, it is probably too late and too costly to buy long-term care insurance at that time. The surviving spouse needs to consider “self-insuring” for possible long-term care expenses.

7. Retitling of jointly owned assets. The surviving spouse will need to retitle jointly owned assets held by the surviving spouse and deceased spouse. These jointly owned assets include bank and credit union accounts, brokerage accounts, and real estate.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.