On January 5, 2025, H.R. 82, also known as the Social Security Fairness Act, previously passed in the House and Senate with bipartisan support, was signed into law by President Biden.

For CSRS and CSRS Offset Feds and survivors, it is an unqualified win.

Broadly, this piece of legislation repeals the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO), two rules that reduced or eliminated Social Security payments to individuals who served in employment not covered by Social Security, even if they had the necessary minimum quarters under Social Security from other employment.

What does it mean?

For this article, we will confine our discussion to the impact on civilian federal employees, specifically those within the CSRS and CSRS Offset retirement systems.

Who will benefit?

The obvious beneficiaries are current CSRS and CSRS Offset retirees who have had their Social Security income reduced due to the Windfall Elimination Provision. Even more significant will be the impact for spouses and survivors under the two systems who were denied spousal or survivor Social Security benefits under the Government Pension Offset.

Based on an estimate made by the Congressional Budget Office, as of 2025, the average increases to reduced or eliminated benefits as a result of the repeal of the WEP and GPO are:

Windfall Elimination Provision $ 360/mo

Government Pension Offset for spouses $ 700/mo

Government Pension Offset for survivors $1,190/mo

For many families, this increase could profoundly change their lifestyles!

What is the timetable for implementation?

Detailed information is limited at this time, but changes are expected to begin in 2025, including retroactive payments from Jan 1, 2024.

What steps should impacted Feds take?

If you are already receiving Social Security payments, the Social Security Administration asks that you log in to ensure your mailing address and direct deposit bank information are both current. You will not need to file for benefits again. Your payment should simply be adjusted.

If you have never filed for Social Security benefits, you will need to do so. The Social Security Administration is recommending that you file online at ssa.gov/apply or reach out to their office directly to schedule an appointment.

Be prepared with the following information when you apply:

- An original or certified copy of your birth certificate

- Your Social Security Card or record number

- Military service papers (if you served before 1968)

- W-2 forms or self-employment tax returns from the previous year

- Marriage certificate

- Final divorce decree, if applying as a divorced spouse.

The Social Security Administration’s dedicated Social Security Fairness Act website is: https://www.ssa.gov/benefits/retirement/social-security-fairness-act.html. Please check back regularly for updates and watch for any communications from the SSA for additional action to take.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

Better Safe than Sorry

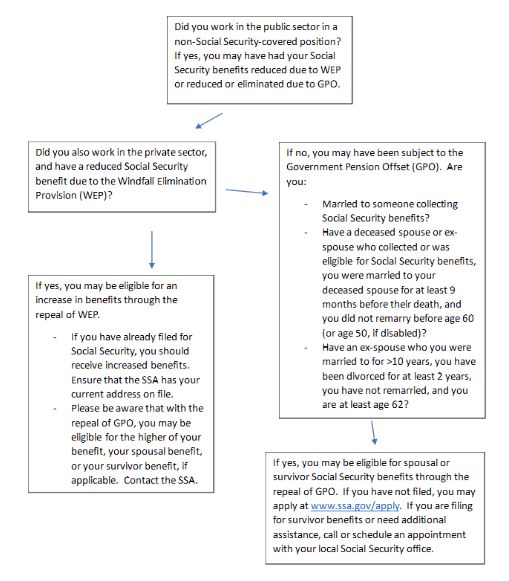

Understanding eligibility in the wake of the passage of the Social Security Fairness Act may be complicated – this is why we’ve included a helpful flowchart below to bring some clarity to the issue; however, there is no downside to inquiring about your benefits.

The bottom line: If you believe you may be eligible for an increase in benefits due to the repeal of GPO and new eligibility for spousal or survivor benefits, we recommend you contact the SSA.

Consult a Professional

If you have questions or want to discuss how the Social Security Fairness Act could impact you and your retirement planning, contact the team at Serving Those Who Serve for a 1-on-1 financial planning consultation at https://stwserve.com/contact-us/.

The information has been obtained from sources considered reliable but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Serving Those Who Serve writers and not necessarily those of RJFS or Raymond James. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy suggested. Every investor’s situation is unique and you should consider your investment goals, risk tolerance, and time horizon before making any investment or financial decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. **