This is the third of four FEDZONE columns discussing the withdrawal options that are available to separated Thrift Savings Plan TSP) participants. In these columns, a “separated” participant means a civilian employee or a member of the uniformed services who has separated from that employment.

Retirement account rollovers are an important part of a federal employee’s retirement savings management. Whether an employee is changing jobs – leaving federal service and working in private industry – or transitioning into retirement, an employee’s understanding of how rollovers work can help the employee make informed decisions about their financial future.

What is a rollover?

A rollover is the process of transferring funds from one retirement account to another. There are two ways for a federal employee or retiree to perform TSP rollovers, namely: (1) Direct (“trustee-to-trustee”); or (2) Indirect.

Using a direct rollover ensures that a TSP participant’s TSP account will be moved directly to a qualified retirement account (such as a 401(k) qualified retirement plan), or to an IRA. Direct rollovers also help avoid any tax penalties or missed deadlines.

With an indirect TSP rollover, the TSP participant receives a check or distribution which must be deposited into another qualified retirement account or IRA within 60 days to avoid taxes and penalties.

TSP distributions considered as eligible rollover distributions.

The following TSP distributions are considered “eligible” rollover distributions:

- A distribution of part or all of a TSP account after the participant separates from service.

- All “force-outs”, automatic payouts of TSP accounts that contain less than $200.

- Equal installment payments expected to be paid out in less than 10 years. This is true unless the installment payments are computed using the life expectancy table.

- Amounts paid to a participant after the total distribution of a TSP account. For example, a late contribution to a TSP participant’s account.

- An in-service age 59.5 withdrawal.

- Death benefits paid to the spouse of a deceased TSP participant.

- Death benefits paid to a non-spouse provided the non-spouse requests a direct rollover to an inherited IRA.

- Amounts paid to a current or a former spouse under a qualifying court order or legal process.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

How is a TSP direct rollover made?

The TSP makes direct rollovers daily by the issuance of a US Treasury check made out to the destination qualified retirement or IRA. The Employer Identification Number of the TSP is 52-1529691. A TSP participant’s financial institution or retirement plan administrator (to which the TSP directly rolls over the TSP funds on behalf of the TSP participant) must certify that the financial institution or retirement plan administrator will accept the TSP funds and provide rollover information on the TSP participant’s distribution request.

Before a TSP participant decides to directly rollover money from his or her TSP accounts to an IRA or to an eligible employer retirement plan, the TSP participant should find out whether: (1) The participant’s IRA or employer-sponsored qualified retirement plan accepts direct rollovers; (2) The minimum amount the IRA or employer will accept; and (3) Whether any tax-exempt or Roth IRA contributions will be accepted.

TSP participants should be aware that the rules for eligible employer-sponsored qualified retirement plans that receive the direct rollover will determine the TSP participant’s investment options, fees and rights to payment.

The type of retirement plan or account to which a TSP participant can rollover his or her TSP funds depends on whether the funds are from the traditional TSP balance or the Roth TSP balance.

Eligible traditional TSP rollover distributions may be directly rolled over to a traditional IRA or to a traditional eligible employer-sponsored retirement plan.

Eligible Roth TSP rollover distributions may be rolled over to a Roth IRA or to a Roth eligible Roth employer-sponsored retirement plan.

The following items cannot be rolled over:

- Excess deferrals – contributions made via payroll deductions.

- Distributions attributable to an unpaid TSP loan.

- “P.S. 58 costs” - the cost of life insurance.

- Any amounts in a TSP account attributable to contributions on behalf of a ‘key employee.” The TSP is a government plan, as defined in Internal Revenue Code (IRC) section 414(d). IRC section 401(a) provides that a government plan is exempt from IRC Section 416, which deals with “key employees”.

- Any annual traditional TSP required minimum distributions (RMDs).

Requesting TSP rollovers

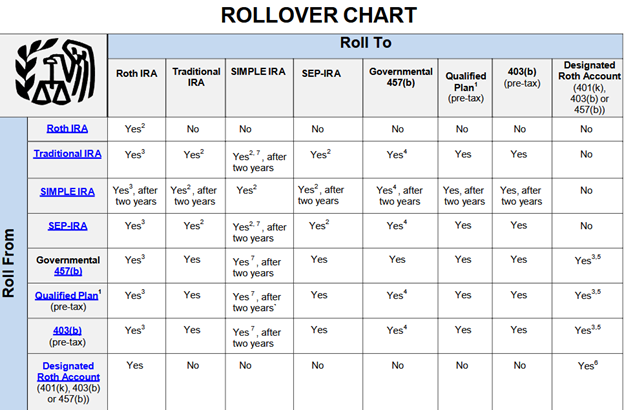

TSP participants who want to perform TSP direct rollover should request a direct rollover in MyAccount or by using one of the ThriftLine options . They should not use forms provided by the new qualified retirement, financial institution or IRA custodian. The following is a copy of the IRS “rollover chart.”

- Qualified retirement plans include, for example, profit-sharing, 401(k), money purchase, and defined benefit plans.

- Only one rollover in any 12-month period.

- Must include in income.

- Must have separate accounts.

- Must be an in-plan rollover.

- Any nontaxable amounts distributed must be rolled over by direct trustee-to-trustee transfer.

- Applies to rollover contributions after December 18, 2015. For more information regarding retirement plans and rollovers, visit Tax Information for Retirement Plans.

If you've recently left your job or are retiring, you may be wondering what to do with your old retirement plan. It's a common question — and one with several valid answers. This outlines the four most common options available to you, with an explanation of each option's potential benefits and limitations. Choosing the right path depends on your personal financial goals, timeline, and retirement plan.

OPTION 1: Leave the Money in Your Former Employer's Plan, if permitted by the plan

Pros:

- May prefer the investment choices already available

- No tax consequences

- May be no cost to maintain the account

Cons:

- May have fewer investment options than an IRA

- Potentially limited control or flexibility

OPTION 2: Roll Over to a New Employer's Plan, if available and permitted

Pros:

- Consolidates retirement accounts into one place

- Continuing tax-deferred growth

- No tax consequences

Cons:

- Not all plans accept rollovers

- Potentially fewer investment choices than an IRA

OPTION 3: Roll Over to an IRA

Pros:

- Potentially greater investment flexibility and access to a wider range of funds

- Consolidates accounts in one place

- May allow for more personalized management and advice

- No tax consequences if done correctly as a direct rollover

Cons:

- IRAs may involve management or custodial fees

- May lack creditor protection offered by ERISA-qualified employer plans

- Investment selection and guidance depend on the institution or advisor you choose

- Potential termination fees

OPTION 4: Cash Out the Account

Pros:

- Immediate access to funds if needed urgently

Cons:

- Subject to income taxes

- If under age 59½, may also incur a 10% early withdrawal penalty

- Permanently reduces retirement savings and potential long-term growth

This guide is intended to help you understand the most common retirement plan options. However, the right choice depends on your unique financial picture.

Before acting, be sure to consider:

- Fees and expenses

- Investment options

- Tax treatment

- Required minimum distributions

- Legal protections

- Your retirement timeline

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

You Might Also Enjoy This Podcast

Ed Zurndorfer, EA, ATA, CFP®, CLU®, ChFC®, CEBS®, ChFEBC℠: Federal Employee Benefits Expert

A former career Federal employee, Ed has published a staggering 1,200+ separate articles on Federal Benefits and Retirement!

Just “Google” his name, and you are likely to find a plethora of sites that contain his writings. Drawn to its mission to reach, teach

and serve Feds, Serving Those Who Serve is the only financial planning practice with which Ed has chosen to affiliate in over

20 years teaching. In addition to conducting Federal Benefits seminars for Serving Those Who Serve, you can find Ed’s

writings here on our blog in the FedZone, and on Fed-Soup, MyFederalRetirement, FederalNews Radio and NITP.

He is a member of the Maryland Society of Accountants, the National Association of Enrolled Agents, the International Society of Certified Employee Benefits Specialists, the Financial Planning Association, the National Association of Health Underwriters,

and the Society of Financial Service Professionals. Since 1999, Ed has taught many thousands of Federal employees about

their benefits, in person and at Federal agencies all over the country. Ed is a true national treasure.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.