Through the years, individuals have contributed to the different types of Individual Retirement Arrangements (IRAs). These different types of IRAs include deductible and nondeductible traditional IRAs and Roth IRAs. In order to contribute to any type of IRA for a particular year, an individual (if married, and/or the individual’s spouse) must have earned income. Earned income includes salary, wages, tips and net self-employment earnings during the year.

During 2025, all individuals with earned income can contribute a maximum $7,000 (if under age 50 as of December 31, 2025) or $8,000 (if over age 49 as of December 31, 2025) to a traditional IRA, Roth IRA, or to a combination of both.

Federal employees who were in federal service during 2025 are therefore eligible to contribute to an IRA for calendar year 2025. The deadline for contributing to an IRA for 2025 is the federal income filing deadline of April 15, 2026. Many federal employees prefer the Roth IRA over the traditional IRA for several reasons including potential tax-free investment growth and tax-free withdrawals. Also, unlike the traditional IRA, the Roth IRA is not subject to any required minimum distribution (RMD). A Roth IRA owner can enjoy the potential of tax-free growth knowing that nothing has to be withdrawn at a certain age. But it is reassuring that if a withdrawal has to be made from a Roth IRA, that all qualified withdrawals are income-tax free.

However, there are income limitations each year on who is eligible to contribute to a Roth IRA. The Roth IRA contribution limit is reduced when modified adjusted gross income (MAGI) reaches certain levels. The following table summarizes by tax filing status these contribution limitations:

Roth IRA Contribution “Phase-Out” (2025) Limitations

| Filing Status | MAGI1 “Phase-Out Range”2 |

| Married filing Joint, Qualified Surviving Spouse

Single, Head of Household Married Filing Separate |

$236,000 – $246,000

$150,000 - $165,000 $0 - $10,000 |

1 MAGI for Roth IRA contribution equals: Adjusted Gross Income (AGI)

- Income from Roth IRA conversions

+ Deduction for traditional IRA contributions

+ Student loan interest

+ Foreign earned income exclusion

+ Foreign housing exclusion or deduction

+ Exclusion of qualified bond interest used for education

2The IRS in IRS Publication 590-A (Contributions to IRAs) has worksheets to determine the contribution phase-out amount based on MAGI. Go to https://www.irs.gov/pub/irs-pdf/p590a.pdf, page 43.

Throughout 2025, many individuals including federal employees and retirees made contributions to their Roth IRAs. They may not have been aware of any MAGI limitations for making Roth IRA contributions. Other individuals, while aware of the MAGI limitations, found out they were ineligible for contributing to a Roth IRA for 2025 when they received their 2025 W-2 and 1099 income statements in January 2026. The question is: Is there anything that these individuals can do to undo their 2025 Roth IRA contributions? The answer is yes. It is called a Roth IRA contribution recharacterization.

Why Would a Roth IRA Owner Have to Recharacterize a 2025 Roth IRA Contribution?

There is one of two reasons that a Roth IRA owner would have to recharacterize a 2025 Roth IRA contribution, namely: (1) The Roth IRA owner and spouse, if married, had no earned income during 2025; and (2) The Roth IRA owner’s MAGI exceeded the upper MAGI limit for the owner’s 2025 tax filing status.

The following example illustrates how an individual made a Roth IRA contribution during 2025 and determined that she was not eligible to contribute to her Roth IRA for 2025 because her MAGI was above the upper limit.

Margaret, age 54, is a federal employee who contributed $8,000 to her Roth IRA in October 2025. While gathering her 2025 income statements (W-2 and 1099s) in January 2026, in order to prepare her 2025 federal tax returns, Margaret determined her 2025 MAGI was $172,500. The $172,500 exceeds the $165,000 MAGI limit for a single tax filer. As explained below, Margaret will have to recharacterize her 2025 Roth IRA contribution of $8,000.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

How to Recharacterize a 2025 Roth IRA Contribution

In order to recharacterize a 2025 Roth IRA contribution, the Roth RIA owner must directly transfer the Roth IRA in which the contributions were made to a second IRA called a nondeductible traditional IRA. A direct transfer is a “trustee-to-trustee” transfer in which none of the Roth IRA is sent directly to the Roth IRA owner.

The deadline to directly transfer the Roth IRA to the nondeductible traditional IRA is April 15, 2026. However, if the Roth IRA owner files his or her 2025 federal income tax by April 15, 2026, then a six-month extension to October 15,2026 is allowed in order to perform the 2025 Roth IRA contribution recharacterization.

The following are the steps that an individual must perform in order to recharacterize a 2025 Roth IRA contribution:

Step 1. The Roth IRA owner must instruct the Roth IRA custodian to directly transfer the 2025 Roth IRA contributions, and nay net income allocable to the contributions, to the second traditional (nondeductible) IRA.

Step 2 The Roth IRA owner must report the recharacterization on his or her 2025 federal income tax return.

Step 3. The Roth IRA owner must trat the 2025 Roth IRA contribution as being a 2025 traditional (nondeductible) IRA contribution that was made on the same date during 2025 as the contribution was made to the Roth IRA during 2025.

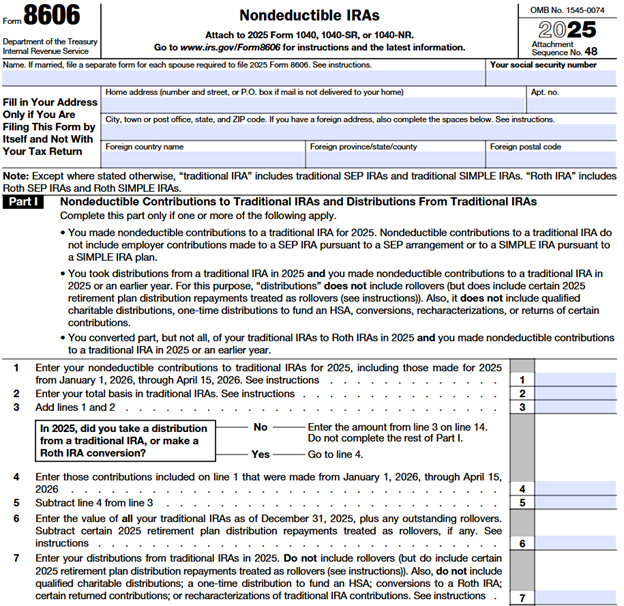

Step 4 Roth IRA owner who recharacterizes a 2025 Roth IRA contribution to a traditional (nondeductible) IRA needs to report the amount of the contribution being transferred to the traditional IRA on IRS Form 8606 – Part I (Nondeductible IRAs). A copy of IRS Form 8606 Part I Line 1 for the year 2025 is shown here:

The following chart summarizes the reporting of a recharacterization of a 2025 Roth IRA contribution.

|

Initial Contribution |

Recharacterization |

Report on IRS Form 8606 Part I, line 1. |

Include as “IRA Distribution” on Form 1040, Line 4a: Recharacterization and contribution in 2025. |

| Contribution to Roth IRA | Transfer to a traditional IRA | Only the part, if any, that is recharacterized as a contribution to the traditional IRA to the extent it is nondeductible | Amount transferred from the Roth IRA to the traditional IRA. Attach a statement to Form 1040 explaining the recharacterization. |

Returning to the example above with Margaret, who mistakenly contributed $8,000 to her Roth IRA for the year 2025, Margaret fills out the chart as follows:

|

Initial Contribution |

Recharacterization |

Report on IRS Form 8606 Part I, line 1. |

Include as “IRA Distribution” on Form 1040, Line 4a: Recharacterization and contribution in 2025. |

| Contribution to Roth IRA =

$8,000. |

Transfer to a traditional IRA = $8,200*. | Only the part, if any, that is recharacterized as a contribution to the traditional IRA to the extent it is nondeductible = $8,000. | Amount transferred from the Roth IRA to the traditional IRA = $8,200. Margaret will attach a statement to her 2025 federal income tax return (Form 1040) explaining why she is recharacterizing her $8,000 Roth IRA contribution. |

* Includes $200 of earnings

Individuals should be aware that the IRS penalty for not recharacterizing a Roth IRA contribution is 6 percent of the amount of the Roth IRA contribution that should have been recharacterized but was not. The penalty is imposed for each year that the contribution is not recharacterized. With Margaret, if she fails to recharacterize her $8,000 Roth IRA contribution by October 15, 2026, she will be subject to an IRS penalty of 6 percent of $8,000, or $480.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

This is a hypothetical story and not indicative of any specific situation or client. It is presented only as an example and not intended as investment advice. Investing involved risk and there is no assurance that any investment strategy will be successful.

IRAs: Contributions to a traditional IRA may be tax-deductible depending on the taxpayer’s income, tax-filing status, and other factors. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty.

Roth IRA: Like Traditional IRAs, contribution limits apply to Roth IRAs. In addition, with a Roth IRA, your allowable contribution may be reduced or eliminated if your annual income exceeds certain limits. Contributions to a Roth IRA are never tax deductible, but if certain conditions are met, distributions will be completely income tax free. Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted.

Roth Conversions: Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Additionally, each converted amount may be subject to its own five-year holding period. Converting a traditional IRA into a Roth IRA has tax implications. Investors should consult a tax advisor before deciding to do a conversion.

RMDs: RMD's are generally subject to federal income tax and may be subject to state taxes. Consult your tax advisor to assess your situation.

You Might Also Enjoy This Podcast

Ed Zurndorfer, EA, ATA, CFP®, CLU®, ChFC®, CEBS®, ChFEBC℠: Federal Employee Benefits Expert

A former career Federal employee, Ed has published a staggering 1,200+ separate articles on Federal Benefits and Retirement!

Just “Google” his name, and you are likely to find a plethora of sites that contain his writings. Drawn to its mission to reach, teach

and serve Feds, Serving Those Who Serve is the only financial planning practice with which Ed has chosen to affiliate in over

20 years teaching. In addition to conducting Federal Benefits seminars for Serving Those Who Serve, you can find Ed’s

writings here on our blog in the FedZone, and on Fed-Soup, MyFederalRetirement, FederalNews Radio and NITP.

He is a member of the Maryland Society of Accountants, the National Association of Enrolled Agents, the International Society of Certified Employee Benefits Specialists, the Financial Planning Association, the National Association of Health Underwriters,

and the Society of Financial Service Professionals. Since 1999, Ed has taught many thousands of Federal employees about

their benefits, in person and at Federal agencies all over the country. Ed is a true national treasure.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.