Effective January 1,2018 following the passage of the Tax Cuts and Jobs Act of 2017 (TCJA), individual federal marginal tax rates were reduced to the lowest rates in the 100-year history of the federal individual income tax. While the TCJA legislation reduced individual tax rates only temporarily (until December 31, 2025), the One Big Beautiful Bill Act (OBBBA) (passed into law in July 2025) extended the low rates through 2035. Many federal employees are taking advantage of these low individual tax rates by contributing every year to a Roth IRA. With a Roth IRA, the contributions to a Roth IRA are made with after-taxed dollars, and earnings grow tax-free because all qualified Roth IRA withdrawals are income-tax free. There are two reasons why many financial advisors recommend that their clients contribute to a Roth IRA. The first reason is that with low-income tax rates currently but income tax rates expected to increase sometime in the future, a Roth IRA comes ahead. The second reason is that a Roth IRA owner is never subject to required minimum distributions (RMDs).

The only restriction when it comes to contributing to a Roth IRA is there are adjusted gross income (AGI) limitations. The following table shows the modified adjusted gross income limitations for individuals contributing to a Roth IRA for the year 2025:

Roth IRA Contribution “Phase-Out” (2025) Limitations

| Filing Status | MAGI1 “Phase-Out Range”2 |

| Married filing Joint, Qualified Surviving Spouse

Single, Head of Household Married Filing Separate |

$236,000 – $246,000

$150,000 - $165,000 $0 - $10,000 |

1 MAGI for Roth IRA contribution equals: Adjusted Gross Income (AGI)

- Income from Roth IRA conversions

+ Deduction for traditional IRA contributions

+ Student loan interest

+ Foreign earned income exclusion

+ Foreign housing exclusion or deduction

+ Exclusion of qualified bond interest used for education

2The IRS in IRS Publication 590-A (Contributions to IRAs) has worksheets to determine the contribution phase-out amount based on MAGI. Go to https://www.irs.gov/pub/irs-pdf/p590a.pdf,.

In the past - and still true under the OBBBA - high income individuals have used the “back-door” Roth IRA strategy to move traditional IRA funds into Roth IRAs. This column discusses how the “back-door” Roth IRA strategy works and how it can benefit in particular high income Federal employees. The “back-door” Roth IRA strategy allows individuals to move funds into a Roth IRA even if they do not qualify to contribute to a Roth IRA because their income exceeds the allowable limits. To do so, these individuals, or if they are married their spouses, must have earned income (salary, wages or net self-employment income). No matter the amount of their annual income, they are eligible to contribute to a nondeductible traditional IRA - as much as $7,000 ($8,000 if over age 49) during 2025 (the deadline to make an IRA contribution for 2025 is April 15, 2026), and then immediately convert that contribution to a Roth IRA. This is the case no matter their age, income or tax filing status. Congress and the IRS have said that the “back-door” Roth strategy is a perfectly legal strategy, and many high- income individuals have successfully used the strategy over the years.

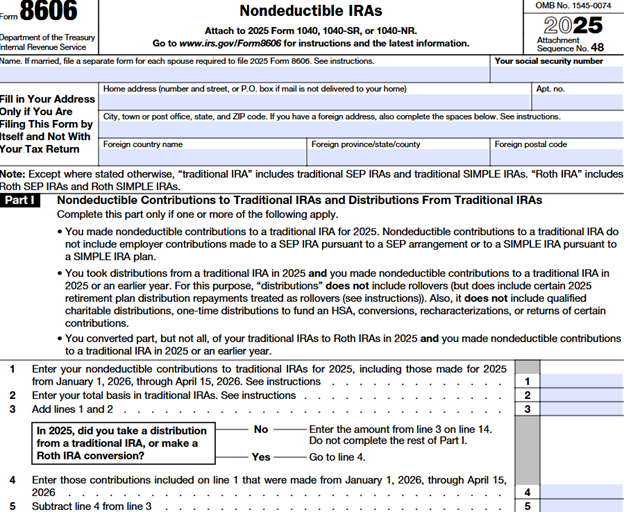

The following suggestions are for federal employees who intend to convert a nondeductible traditional IRA that they may have already contributed to (or will before April 15,2026) for the year 2025 to a Roth IRA using the “back-door” Roth IRA strategy. Note that with a nondeductible traditional IRA, contributions are made with after-taxed dollars and any earnings grow tax-deferred. A federal employee who contributes to a nondeductible traditional IRA in any year needs to file with his or her federal income tax return that year IRS Form 8606 (Nondeductible IRAs). By filing Form 8606, the traditional IRA owner notifies the IRS that the contribution to the IRA was made with after-taxed funds.

- Employees and/or if married, their spouses, must have earned income during 2025. For married couples, each spouse can perform a “back door” Roth IRA conversion. The maximum that can be contributed to a traditional IRA for 2025 is $7,000 for employees younger than 50, and $8,000 for employees who were over age 49 as of December 31, 2025.

- Employees have until April 15,2026 to make their 2025 traditional IRA contributions and file Form 8606 with their 2025 Federal income tax return. If they have already filed their 2025 federal income tax return, they can file the 2025 Form 8606 by itself, reporting the 2025 traditional IRA contribution. The following shows a portion of Form 8606 for the year 2025.

- The “back-door” Roth IRA conversion strategy works no matter the age of the employee/traditional IRA owner, even if the employee has reached his or her required beginning date (RBD – currently age 73) for taking traditional IRA required minimum distributions (RMDs). However, an employee who has reached the RBD must still take his or her traditional RMD that year even though the employee is performing a “back-door” conversion.

- The pro-rata rule applies to “back-door” Roth IRA conversions. This means that all owned traditional IRAs, (including contributory traditional IRAs, rollover traditional IRAs. SEP traditional IRAs and SIMPLE traditional IRAs are included in the “pro-rata” calculations in order to determine how much of the traditional IRA funds will be taxable upon conversion. What this means is that some portion of the Roth IRA conversion will likely be taxable. Federal employees with pre-taxed traditional IRAs and TSP accounts can avoid paying taxes on the conversion by first transferring any pre-tax traditional IRAs into their traditional TSP accounts. They may do so by going online to their online TSP accounts and requesting a transfer of traditional IRAs into their traditional TSP).

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

Note that the “pro-rata” traditional IRA determination is calculated as follows:

Tax-free portion of converted traditional IRA funds equals:

Amount of converted IRA funds times (after-tax IRA balance) / (total IRA account balance)

Taxable portion of converted traditional IRA funds equals:

Amount of converted IRA funds times (before-tax IRA account balance) / (total IRA account balance)

The following example illustrates:

Jan is a single federal employee whose modified adjusted gross income (MAGI) during 2025 was $200,000, far above the $185,000 MAGI limit for contributing to a Roth IRA. Jan contributes $7,000 to her traditional IRA. Because Jan is covered by a pension plan (FERS) and because Jan contributes to the TSP, Jan’s $7,000 contribution to her traditional IRA is nondeductible. Jan files IRS Form 8606 with her 2025 Federal income tax return reporting the $7,000 traditional IRA contribution. In so doing, Jan is notifying the IRS that the $7,000 IRA contribution was already taxed and therefore will be withdrawn from the IRA tax-free.

Jan owns three IRAs. One IRA is a rollover IRA from a previous employer’s traditional 401(k) plan that is currently worth $50,000. Jan also has a traditional SEP-IRA (also from a previous employer) that is worth $40,000, and she has a $10,000 traditional IRA that consists entirely of after-taxed contributions of $10,000 and no earnings.

Under the pro-rata rule, Jan’s IRA account has a balance of $100,000 ($50,000 plus $40,000 plus $10,000). Of the $100,000, with the $10,000 consisting of only taxed funds. The other $90,000 is money that has never been taxed. This means that if Jan were to convert the $7,000 traditional IRA contribution to a Roth IRA, only 10 percent of the conversion is tax-free. The other 90 percent of the conversion is taxable, as shown here:

Tax-free portion: $7,000 times $10,000/$100,000 equals $700.

Taxable portion: $7,000 times $90,000/$100,000 equals $6,300.

Note that Jan is paying tax on 90 percent of her converted IRA funds even though her $7,000 traditional IRA contribution she made during 2025 was made with after-taxed funds. To avoid paying tax again on 90 percent of her converted IRA funds, Jan should have first transferred her $50,000 pre-taxed traditional IRA and $40,000 SEP IRA into her TSP account. If she had done that, then her IRA account would have had a total balance of $10,000 consisting of already-taxed funds. In that case, 100 percent of the conversion will be tax-free, as shown here:

Tax-free portion: $7,000 times $10,000/$10,000 equals $7,000.

Taxable portion: $7,000 times $0/$10,000 equals $0.

**The above hypothetical example is for illustrative purposes only.

- The traditional IRA funds that are converted to the Roth IRA via a “back-door” conversions are considered Roth IRA converted funds and not Roth IRA contributions. As such, individuals under age 59.5 who perform a “back-door” conversion must wait five years for penalty-free access to those funds. On the other hand, if the funds went in as Roth IRA contributions, the contributions would be accessible immediately, tax- and penalty-free.

Federal employees who are interested in performing a “back-door” Roth IRA conversion before the April 15,2026 federal income tax filing deadline are advised to talk to their tax advisor before performing a conversion. The advisor should be able to answer any questions the employee may have and most importantly, advise the employee what to do in order to pay the minimum amount of taxes resulting from a “back-door” Roth IRA conversion.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.