![]()

Your salary and benefits are likely excellent as a mid-career fed. However, the chances are pretty good that you don’t have buckets of cash available to pay for your child’s college career.

This is where financial aid can help. To take advantage of what’s out there, you need to share information about income, assets, contributions, and accounts through the Free Application for Federal Student Aid (FAFSA) or the College Scholarship Service Profile (CSS).

Additionally, early planning helps improve financial support as your child launches their collegiate years.

Two Applications, Different Purposes

The FAFSA and CSS are similar in a couple of ways:

- They analyze your income and assets to determine appropriate aid packages for your student.

- They should be completed early in your student’s senior year of high school.

Here’s how they differ:

- The FAFSA establishesyour student’s eligibility for federal aid, including government-backed loans, work-study funds, and grants.

- The CSS is usedby colleges, universities, and scholarship programs to determine eligibility for non-federal student aid.

- Required FAFSA federal employee income information differs from that mandated by the CSS. Additionally, FAFSA parent asset formula calculations differfrom those in CSS.

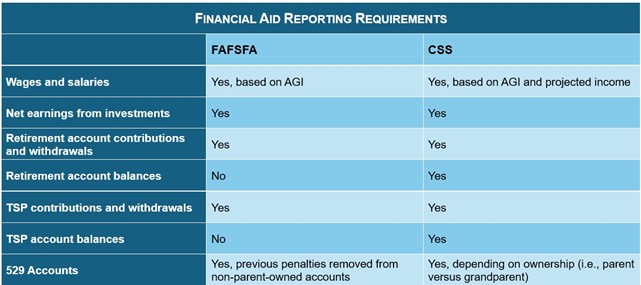

The chart, below, provides additional information.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

In summary:

- Both CSS and the FAFSA need your income information.

- TSP contributions and withdrawals must be reported; the CSS also requires account balance information.

- 529 accounts must be reported, though calculations and penalties depend on the account’s owner (parent, grandparent, or student).

- Each application has specific financial calculations to determine available aid packages.

The Do’s and Don’ts of Tuition Planning

Consider the following when determining how to support your student’s higher education career financially.

Actions to Take

DO start saving for college costs early on through 529 plans or other investment vehicles; the more you put aside now, the better financially prepared you’ll be

DO analyze the total cost of your child’s education before filling out FAFSA and CSS forms; be sure to add tuition, room and board, and inflation to the mix.

DO avoid income spikes like bonuses or large, taxable withdrawals during the base years used for financial aid calculations.

Actions to Avoid

DON’T wait until the last moment to fill out CSS or FAFSA forms. Start researching during your child’s junior year to understand the requirements and paperwork needed.

DON’T sacrifice retirement contributions to save for a college education; consider automatic deposits into your TSP to ensure continual funding.

DON’T make assumptions about the impact of 529 accounts on FAFSA or CSS analyses. The requirements differ, and rules consistently change, so do your homework.

DON’T assume that a high income cuts your student off from financial aid. Not all awards or loans are need-based.

Start Preparing Now

Advanced planning is essential when sending your kid to college. You should also understand how your federal income, asset values, and 529 accounts might impact FAFSA and CSS requirements. The more you prepare, the less daunting or frustrating the paperwork will seem.

For additional help on college and retirement planning, reach out to the Fed-focused CERTIFIED FINANCIAL PLANNERS® at Serving Those Who Serve. These experienced individuals are ready to work with you to provide guidance and programs to help cover college costs while shoring up your retirement dreams.

To set up a no-obligation meeting, visit the website or email [email protected].

The information has been obtained from sources considered reliable but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Serving Those Who Serve writers and not necessarily those of RJFS or Raymond James. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy suggested. Every investor’s situation is unique and you should consider your investment goals, risk tolerance, and time horizon before making any investment or financial decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. **