Over the past 20 years, many Americans including federal employees have been staying on the job longer. Workers aged 75 and over are expected to have the largest growth in labor force participation of any age bracket over the next 10 years. The Bureau of Labor Statistics projects that 10.2 percent of people aged 75 and older will be working in 2034. This is compared to 6.1 percent in 2004.

For those federal employees who continue working in federal service past their early 70’s, the “still-working” exception is a way to delay required minimum distributions (RMDs) from their Thrift Savings Plan (TSP) accounts. This column discusses the TSP RMD “still-working” exception and how it can benefit older federal employees.

How the “Still-Working” TSP RMD Exception Works

The TSP required beginning date (RBD) is currently April 1 following the year a retired federal employee becomes age 73. The current TSP RBD applies to retired federal employees born between January 1,1951 and December 31, 1958. For federal employees born after December 31, 1958, the TSP RBD is April 1 following the year a retired federal employee becomes age 75.The still-working TSP RMD exception also applies to those federal employees born before 1951, and whose RBD is age 70.5 (born before July 1,1949) or age 72 (born between July 1,1949 and December 1,1950).

If a TSP participant continues working in federal service past his or her RBD, then the participant is not subject to TSP RMD until the participant retires from federal service. Note the following: (1) The “still-working” TSP RMD exception for a federal employee applies only to the traditional TSP. Since January 1, 2024, a TSP participant’s Roth TSP account balance has not been included in the calculation of the TSP RMD; (2)The “still-working” exception does not apply to traditional IRAs. That is, if a TSP participant owns a traditional IRA, a SEP-IRA and/or a SIMPLE IRA, then once the participant reaches his or her RBD, the participant must begin IRA RMDs; and (3) If the “still-working” TSP participant previously participated in employer-sponsored qualified retirement plans (such as a 401(k), 403(b) or 457 retirement plan), then the TSP participant must take RMDs from those plans upon reaching his or her RBD.

What Constitutes “Still-Working”?

The IRS has not provided any official information or rules with respect to what constitutes “still working.” That being said, it is possible that an individual could work quarter-time (10 hours a week) or half-time (20 hours a week) and still be considered as “still-working”. But there is no requirement that a TSP participant who reaches his or her RBD work 40 hours a week in order for the “still-working” exception to apply. Presumably, a TSP participant could retire from federal service and immediately be rehired back as a “rehired annuitant,” working half-time and therefore be eligible for the “still-working” exception

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

When Do TSP RMDs Begin?

Under the “still-working” exception, a TSP participant who is older than his or her RBD must take their first TSP RMD in the year of separation from federal service. This is the case, even if the last day of federal service is December 31. The RBD then is April 1 of the year after the year of separation from federal service. The following example illustrates:

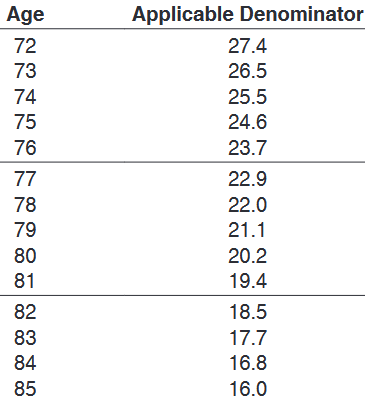

Paul, age 75, retired from federal service on December 31, 2025. Paul has a TSP account and must take his first TSP RMD no later than April 1, 2026. Note that Paul’s first TSP RMD is for the year 2025, the year he separated from federal service. This TSP RMD is calculated using Paul’s traditional TSP account balance as of December 31,2024 and Paul’s life expectancy, obtained from the IRS Uniform Lifetime Table, for age 75 (24.6 years).

For federal employees who separate from federal service after reaching their RBD and who want to rollover traditional TSP funds to a traditional IRA, any TSP RMD must be paid to the retired employee before funds can be rolled over to the traditional IRA. There are several rules that separating federal employees should be aware, namely: (1) All traditional TSP distributions to a traditional IRA or to a traditional qualified retirement plan are considered to be rollovers; (2) TSP RMDs cannot be rolled over; and (3) The first funds distributed out of the traditional TSP are considered RMDs. It does not matter that a retiring TSP participant could defer an RMD until April 1 following the year of separating from federal service. The RMD must be paid out prior to any rollover.

In the example above with Paul, if Paul elected to directly rollover his entire traditional TSP account to a traditional IRA shortly after retiring from federal service on December 31, 2025, he must take his 2025 TSP RMD before he rolls over any portion of his traditional TSP account.

Moving Traditional TSP and Qualified Retirement Plan Funds to the Traditional TSP

The TSP allows traditional TSP participant to rollover traditional IRA and qualified retirement plans into their traditional TSP accounts. To do so, a TSP participant must go online to their TSP account, fill out and submit TSP Form TSP-60. By moving any before-tax funds out of a traditional IRA and/or traditional qualified retirement funds to the traditional TSP, they can leverage the still-working exception to avoid RMDs on the dollars consolidated in their traditional TSP account.

What Happens When the Still-Working Exception Ends?

When a federal employee working past his or her RBD officially retires from federal service, the still-working TSP RMD working exception ends. Those federal employees who are considering or are currently using the still-working exception are advised to consider the impact of future TSP RMDs.

Since those TSP participants who continue in federal service past their RBD will begin taking their TSP RMDs at an older age, the life expectancy factor used in the calculation of the TSP RMD will be shorter, as shown here from the IRS Table III Uniform Lifetime:

The retired TSP participant will also have a larger traditional TSP account balance since more contributions (and, for FERS employees, matching contributions) have been made and RMDs have been delayed. A larger traditional TSP account balance divided by a shorter life expectancy likely results in a larger TSP RMD. Larger TSP RMDs result in more taxable income, meaning more federal and state income taxes have to be paid. Larger TSP RMDs also likely results in a larger adjusted gross income (AGI), resulting in higher Medicare Part B and Medicare Part D monthly premiums, as well as possible loss of federal tax deductions and federal tax credits. For these reasons, those TSP participants who are considering retiring from federal service after reaching their RBD are advised to discuss the future impact of delaying their retirement from federal service with their financial advisors.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.