![]()

One goal of retirement planning is nest-egg protection.

You also need to consider what that nest egg can actually buy once you separate from service.

Cash, CDs, and other cash-alternative investments can be great for principal preservation. However, they don’t always protect you from inflation.

This doesn’t mean that you should immediately yank your money out of such investments. It means that, as you plan for retirement, you should plan for inflation and make decisions to prevent it from eroding your purchasing power.

Inflation, Bread Loaves, and G Funds

Inflation is defined as the increase in the prices of goods and services in a particular economy over time.

And that increase means you pay more for everything from food to energy. For example, the average price of a loaf of bread was approximately $1.50 in July 2021. By April 2026, that average price had risen to approximately $1.87.

While inflation raises bread prices, it also erodes the purchasing power of your savings. Let’s say that you need $50,000 per year to maintain your current retirement lifestyle. In an economy with an annual 3% inflation rate, you’ll need approximately $121,000 per year in 30 years for that same lifestyle.

If too much of your portfolio remains in cash or cash alternatives for too long, inflation may outpace your returns and reduce your purchasing power over time.

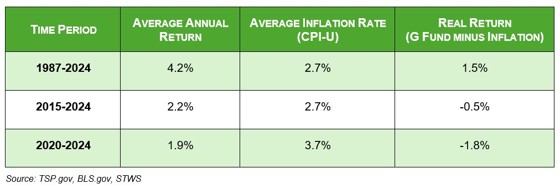

Here are the returns generated from the Thrift Savings Plan’s “safer” G Fund.

The above shouldn’t suggest that the G Fund is bad. It can be helpful for principal preservation while offering a place to put your cash for short-term needs.

However, more is required to help ensure that your accounts preserve your purchasing power as you move into your post-service years.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

Maintaining Your Purchasing Power

Here are some ways to help ensure that you have enough money to help mitigate the impacts of inflation before and during your retirement:

Put a plan in place. Portfolio decisions should align with your spending needs, risk tolerance, and time horizon. These can shift, depending on how close you are to your retirement. Once that plan is determined, re-evaluate it annually and make changes as necessary.

Focus on diversification. You don’t have to pursue aggressive stocks to manage inflation risk. A conservative retirement portfolio can combine growth-oriented investments with dividend-generating stocks and cash alternatives. These different buckets can help preserve purchasing power while supporting long-term account growth.

Avoid emotional decision-making. Screaming headlines can trigger panic, leading you to make poor decisions. Instead, stick to your long-term objectives. If you have questions or concerns, connect with a CERTIFIED FINANCIAL PLANNER©, such as those with Serving Those Who Serve.

Managing Inflation Risk in Retirement

Cash is king in some instances. But cash and cash-alternative investments might not be in your best interest when it comes to what you need in retirement.

Your best course of action is to develop a long-term plan that protects your funds from inflation while ensuring you have the purchasing power you need in retirement.

If you’re not sure where or how to start, contact the CFPs© at Serving Those Who Serve. These fed-focused experts have in-depth experience with understanding and managing federal benefits, retirement plans, and other financial matters.

For more information or to set up your no-obligation appointment, email [email protected] or visit the Serving Those Who Serve website.

The information has been obtained from sources considered reliable but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Serving Those Who Serve writers and not necessarily those of RJFS or Raymond James. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy suggested. Every investor’s situation is unique and you should consider your investment goals, risk tolerance, and time horizon before making any investment or financial decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. **