What you need to know about taxable income, Social Security, and challenging a Medicare B Premium notice.

Edward A. Zurndorfer–

By this time at the end of 2022, all individuals who are currently enrolled in Medicare Part B (Medical Insurance) will have received their notice from the Social Security Administration (SSA) as to what their Medicare Part B monthly premiums will be during 2023. During 2023, most Medicare Part B enrollees will pay the base premium for Medicare Part B of $164.90 per month. However, some senior citizens will pay more, up to a monthly premium of $560.50 per individual per month.

This additional premium is called an Income-Related Monthly Adjusted Amount, or IRMAA. The SSA determines the size of an individual’s IRMAA by comparing their modified adjusted gross income (MAGI) from two years ago, to the current IRMAA thresholds. MAGI is calculated by adding tax-exempt interest to an individual’s regular adjusted gross income (AGI). Individuals whose MAGI is over an income threshold by just $1 are issued that threshold’s IRMAA as their Medicare premiums. The following table illustrates Part B total premiums for high-income beneficiaries with Medicare Part B coverage:

| Beneficiaries who file individual tax returns with 2021 modified adjusted gross income (MAGI) | Beneficiaries who file joint tax returns with modified gross income | Income-Related Monthly Adjustment Amount (IRMAA) | Total Monthly Premium Amount During 2023 |

| Less than or equal to $97,000 | Less than or equal to $194,000 | $0.00 | $164.90 |

| Greater than $97,000 and less than or equal to $123,000 | Greater than $194,000 and less than or equal to $246,000 | $65.90 | $230.80 |

| Greater than $123,000 and less than or equal to $153,000 | Greater than $246,000 and less than or equal to $306,000 | $164.80 | $329.70 |

| Greater than $153,000 and less than or equal to $183,000 | Greater than $306,000 and less than or equal to $366,000 | $263.70 | $428.60 |

| Greater than $183000 and less than $500,000 | Greater than $366,000 and less than $750,000 | $362.60 | $527.50 |

| Greater than or equal to $500,000 | Greater than or equal to $750,000 | $395.60 | $560.50 |

The following example illustrates:

Example 1. Rachel, age 67, retired from federal service on December 31, 2021. Rachel is single and her 2021 MAGI was $136,570. She will pay an IRMAA of $164.80 in 2023 for a total Medicare Part B monthly premium during 2023 of $329.70. Given that Rachel retired on December 31,2021 and that she was fully retired throughout 2022, her MAGI has fallen sharply since 2021. Fortunately, IRMAA relief is possible with Rachel filing a formal request.

Appealing an IRMAA

Those Medicare Part B enrollees who are issued an IRMAA will receive in the mail an initial IRMAA Determination Notice from the SSA. This Determination Notice can be questioned through an appeal process. Knowing the rules of the appeal process will facilitate the appeal process hopefully leading to a favorable ruling by the SSA.

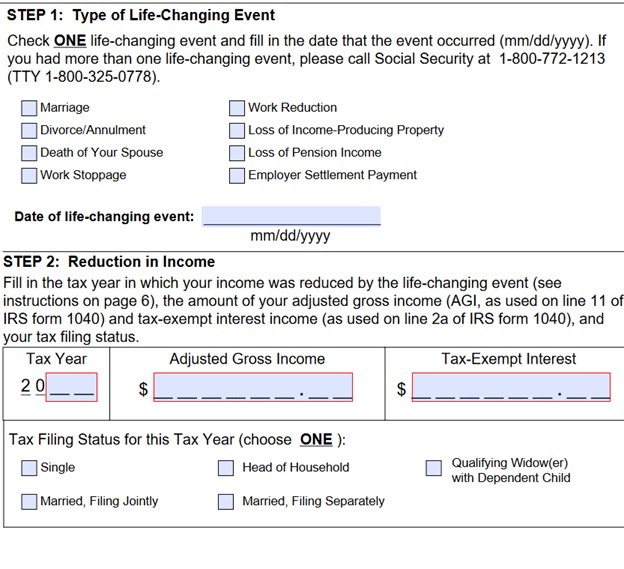

The SSA has defined seven life-changing events that can change how an IRMAA is calculated. The four most common of these life-changing events are: (1) Getting married; (2) Getting divorced; (3) Death of a spouse; and (4) Reducing or stopping work hours. The other three less common life-changing events are: (1) Loss of income-producing property; (2) Loss of pension income; and (3) An employer settlement payment.

No-Cost Webinar, ft. Ed Zurndorfer

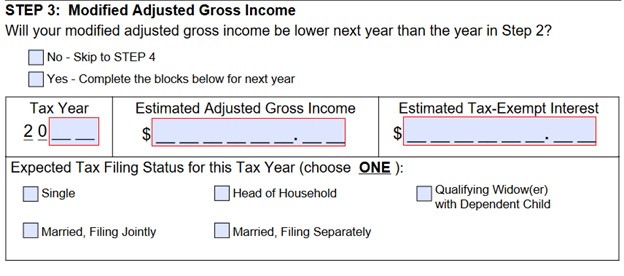

If one of these seven life-changing events affects a Medicare Part B enrollee’s gross income, he or she can appeal the amount of the monthly premium assigned to him or her by notifying the SSA using Form SSA-44 (Medicare Income-Related Monthly Adjustment Amount- Life-Changing Event). This form is completed, one per impacted person. A portion of Form SSA-44 is shown here:

On Form SSA-44, an impacted Medicare Part B enrollee reports: (1) The type and date of the life-changing event in Step 1; (2) The MAGI from the year in which the event in Step 2 occurred: (3) The following year’s lower MAGI in Step 3; and (4) Evidence of the event.

According to the Code of Federal Regulations, the SSA uses more recent information than the two-year MAGI when it is available. For example, if the SSA has a life-changing form that reports an estimated 2022 income, that income would be used to calculate 2023 IRMAAs instead of a 2020 o 2021 tax return. The following example illustrates:

Example 2. Same facts as in Example 1. Rachel retired from federal service on December 31, 2021. Her 2021 MAGI was $136,570, consisting almost entirely of her gross salary of $124,000. During 2022, the first year that Rachel was retired and not working, her gross income consisted of a $52,000 FERS annuity and $24,000 of Social Security for a total MAGI of $76,000. Rachel’s income tier level will go from the third income tier level, in which she is due to pay $329.70, per month in Medicare Part B monthly premiums, to the first income tier level of $164.90 per month in Medicare Part B monthly premiums.

Depending on when Form SSA-44 is filed, it is possible that the SSA could issue reimbursement for already paid IRMAA surcharge. It is also possible that if the estimates on the life-changing event form prove to be inaccurate, the SSA can retroactively reissue an IRMAA.

When Lower Income is Anticipated

For federal employees, the most common life-changing event for an IRMAA occurs when an employee continues to work in federal service post their 65th birthday. They are enrolled in a Federal Employees Health Benefits (FEHB) program health plan and Medicare Part A (Hospital Insurance) but are not enrolled in Medicare Part B because they are still working. They will enroll in Medicare Part B when they retire during the eight-month Special Enrollment period and will not be subject to a late-enrollment penalty for Medicare Part B. However, since their income will most likely decrease immediately after retiring from federal service, these recent retirees are encouraged to be proactive and submit a Form SSA-44 to the SSA reporting a drop in their income. The retiree would check “work stoppage” as a type of life-changing event in Step1 of Form SSA-44.

When Projecting Future Income Does Not Result in a Qualifying Life Event

There are some occasions when a Medicare enrollee projects future income to be substantially lower but does not have a qualifying life-changing event. The following example illustrates:

Example 3. Margaret, age 68 and enrolled in Medicare parts A and B, converted $50,000 of her traditional IRA to a Roth RIA during 2021. This conversion was performed only one time during 2021 and the full $50,000 conversion amount was included in 2021 MAGI. Margaret cannot appeal her 2023 Medicare Part B premium because her 2022 and future MAGI will not include a Roth IRA conversion.

The SSA has made it very clear that one-time income “spikes” will affect a Medicare Part B enrollee’s MAGI for that one affected year. Despite the SSA policy, Medicare Part B enrollees are encouraged to talk to the SSA and ask for an IRMAA exception.

You Might Also Enjoy This Podcast

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.