You can receive income from the Federal Employees Retirement System (FERS) as a federal government retiree. The three pillars of FERS include the Basic Benefit Plan and Social Security, with distributions based on your salary. There is also the Thrift Savings Plan (TSP); here, you can contribute as much as you want.

However, in a high-inflationary environment, the value of your retirement savings could be eroded, leaving you short of funds for food, housing and other things. Counteracting high inflation means shifting your strategy to protect your investments and income.

Inflation and Federal Retirement Impact

Inflation is the rate of price increases for goods and services. When prices rise, more money is needed to buy them.

In addition, you could experience the following.

- Investment value erosion. Inflation could decrease the value of your savings and investments, so what you allocate to your TSP could be worth less in the future.

- Retirement fixed-income issues. Your account withdrawals might increase, leaving less money for your post-career life.

On the positive side, two key parts of your FERS pension include cost-of-living adjustments (COLA):

- Social Security COLA increases annually based on inflation.

- FERS COLA applies once you turn 62, but if inflation is 2% or higher, the adjustment may not fully keep up with those rates.

There is no COLA for your TSP. However, you can protect this investment by applying two anti-inflationary approaches: realigning fund allocations or rolling the TSP into an IRA.

Reallocation and TSP Funds

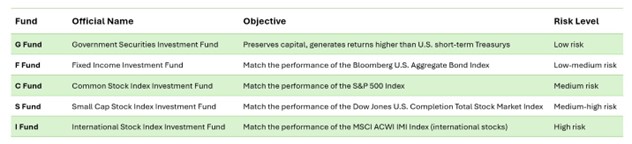

Taking care of your TSP investment means reallocating your distributions to different funds based on several factors, including returns and risk. Available TSP funds are:

One approach might be a “bucket system,” in which you allocate your TSP distributions to various funds. Through this system, your money is placed into the following three buckets:

- Short-term: High liquidity for immediate cash needs (G Fund)

- Intermediate-term: Lower-risk investments that can generate guaranteed returns (F Fund or G Fund)

- Long-term: Medium to higher-risk investments for long-term growth (S Fund, C Fund or I Fund)

You could also use TSP Lifecycle Funds (L Funds), which automatically direct your contributions to the other funds based on your investment goals and risk appetite. Allocations are based on assumptions about future returns, economic growth, inflation, and interest rates.

L Funds might be a good option if you want an expert to direct your distributions to funds that could protect investments from inflation.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer –

TSP Rollover Investment Options

If you’ve changed jobs or are retiring, rolling over your retirement assets to an IRA can be an excellent solution. It is a non-taxable event when done properly, and it can give you access to a much wider range of investments and the convenience of having consolidated your savings in a single location. In addition, flexible beneficiary designations may allow for the continued tax-deferred investing of inherited IRA assets.

In addition to rolling over your 401(k) to an IRA, there are other options. Here is a brief look at all your options. For additional information and what is suitable for your particular situation, please consult us.:

- Leave money in your former employer’s plan, if permitted.

Pro: This may keep fees low, since TSP is fairly cheap. Not a taxable event.

Con: Lack of investment options, doesn’t offer the simplicity of consolidated assets, no professional management. - Roll over the assets to your new employer’s plan, if one is available and it is permitted.

Pro: Keeping it all together and larger sum of money working for you, not a taxable event

Con: Not all employer plans accept rollovers. - Rollover to an IRA.

Pro: Likely more investment options, not a taxable event, consolidating accounts and locations often brings simplicity. This also allows you to work with an investment professional who is familiar with your financial planning context.

Con: Usually there is a fee involved with professional management, potential termination fees. - Cash out the account.

Pro: If you need money, this is an option, although it may come with significant tax consequences and penalties, depending on your age.

Con: This is a taxable event, and creates a loss of investing potential. Costly for young individuals under 59 ½; there is a penalty of 10% in addition to income taxes. Be sure to consider all of your available options and the applicable fees and features of each option before moving your retirement assets.

Ensure That Inflation Doesn’t Impact Investments

Inflation erodes purchasing power and investment value. Because of this, determining an anti-inflation strategy for your FERS strategy is essential. In addition to redirecting TSP allocations to different funds, you could also roll over the amount into an IRA.

Contact the professionals at Serving Those Who Serve to aid in your decision-making. Our Fed-Focused CFPs® have the experience and knowledge to help your investments grow while protecting them in high-inflation environments.

Schedule your no-obligation appointment by visiting stwserve.com or emailing [email protected].

The information has been obtained from sources considered reliable but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Serving Those Who Serve writers and not necessarily those of RJFS or Raymond James. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy suggested. Every investor’s situation is unique and you should consider your investment goals, risk tolerance, and time horizon before making any investment or financial decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. **