Understanding How Federal Employee Retirement Benefits Are Taxed by the IRS – both FERS and CSRS (Part 1)

Edward A. Zurndorfer

Upon retiring from federal service, a federal employee will be the recipient of three distinct types of retirement income including

- (1) A CSRS or FERS annuity being paid by the Office of Personnel Management (OPM);

- (2) Thrift Savings Plan (TSP) withdrawals being paid by the TSP; and

- (3) Social Security monthly retirement benefits being paid by the Social Security Administration (SSA).

Like other types of income, retirement income is subject to federal income tax rules. This column is the first of six FEDZONE columns discussing how the IRS taxes federal retirement benefits. This column presents some general tax-related information that applies to both CSRS and FERS retirees.

Refund (Lump Sum Payment) of CSRS or FERS Contributions

If a federal employee leaves federal service or transfers to a job not under the CSRS or FERS, then the departing employee can elect to receive a lump sum payment that is composed of a refund of the employee’s contributions (made via payroll deduction each pay period while employee was in federal service) to either the CSRS or FERS Retirement and Disability Fund. In order to request this refund of CSRS contributions (made via payroll deduction), a departed CSRS or CSRS Offset employee must fill out and submit Form SF 2802 (Application for Refund of Retirement Deductions) (Civil Service Retirement System). A departed FERS employee requesting a refund of FERS contributions (made via payroll deduction) must fill out and submit Form SF 3106 (Application for Refund of Retirement Deductions) (Federal Employees Retirement System).

The refund will include regular contributions made to the CSRS or FERS Retirement and Disability funds plus any interest payable. If the refund is composed of only the departed employee’s contributions, then none of the refund is taxable. If the refund includes any interest paid by OPM (interest is paid if the departed employee had less than five years of CSRS or FERS service at the time of departure), then the interest portion is taxable unless the departed employee rolls over the interest directly into a qualified retirement plan or into a traditional IRA. OPM pays the refund and interest. OPM withholds federal income tax at a rate of 20 percent if interest is included in the lump sum payment

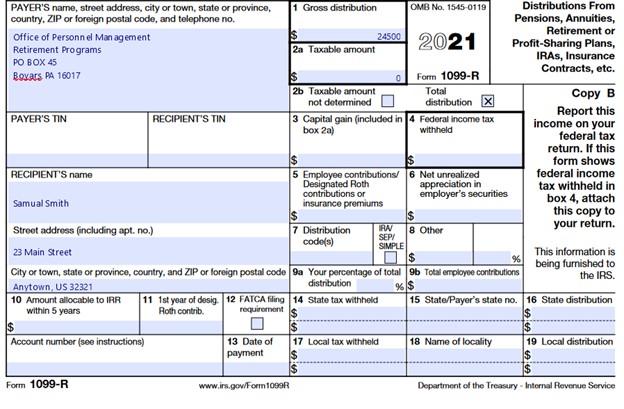

Refunds of retirement contributions made by OPM to former federal employees are reported by OPM to the former employees on IRS Form 1099-R (Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.). A copy of the Form 1099-R is sent by OPM to the IRS. An example of a 2021 Form 1099-R (fictitious) is presented below. Shown in the (made-up) example is a non-taxable lump sum payment of $24,500 (no interest paid) of Samuel Smith’s FERS contributions that he made via payroll deduction to the FERS Retirement and Disability Fund while he was in Federal service between 2008 (when he was hired) and 2021 (when he left federal service).

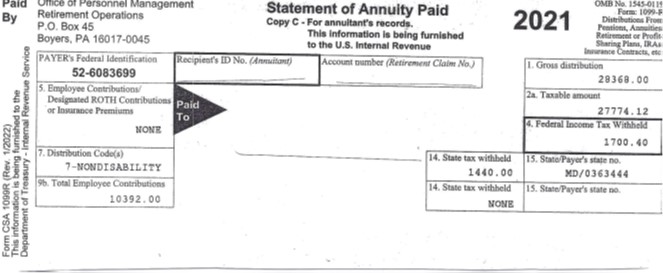

Form CSA 1099-R

Form CSA 1099-R (Statement of Annuity Paid) is mailed by OPM each January to recipients of a CSRS or FES annuity during the preceding calendar year. Among the items shown on a Form CSA 1099-R are:

- (1) An annuitant’s gross CSRS or FERS annuity (including the Retirement Annuity Supplement paid to FERS annuitants who retire before age 62) and for most annuitants, the annuitant’s taxable CSRS or FERS annuity;

- (2) any federal income taxes withheld;

- (3) any state and local income taxes withheld;

- (4) dental, health and/or vision insurance premiums paid; and

- (5) for CSRS or CSRS Offset annuitants, the total amount of CSRS contributions made via payroll deduction (and deposits and redeposits) made to the Civil Service Retirement and Disability; for FERS annuitants, the total amount of FERS contributions (including deposits and redeposits) made to the Federal Employment Retirement and Disability Fund made via payroll deductions during the FERS annuitant’s years of federal service.

Annuitants can view and download their current year Form CSA 1099-R by visiting the OPM Web site here. To log onto their account, an annuitant will need his or her retirement CSA claim number, Social Security number and password.

A sample CSA 1099-R is presented here:

Choosing No Withholding on Payments Outside the US

Annuitants who have chosen to live outside the US or its possessions cannot as a rule elect to have no federal income tax withholding be applied to their CSRS or FERS annuities.

In order to choose no federal income tax withholding, an annuitant who is a US citizen or a resident alien must provide OPM with a home address in the United States or its possessions. Otherwise, OPM is required to withhold federal income tax.

If an annuitant does not provide a home address in the US or its possessions, then the annuitant can choose not to have federal income tax withheld but only if the annuitant certifies to OPM that he or she is not a US citizen or a US resident alien. But in so certifying, the annuitant may be subject to the 30 percent flat federal income tax withholding that applies to nonresident aliens.

Withholding Certificate

If an annuitant gives OPM a federal income tax withholding certificate for pensions (a W-4P), then the annuitant can choose either to not to have federal income taxes withheld or choose to have federal income taxes withheld. The amount of federal income tax withheld depends on the annuitant’s marital status, the number of withholding allowances and any additional amount the annuitant designates to be withheld. If no choice is made, then OPM must withhold as if the annuitant were married with three withholding allowances.

Federal Income Tax Withholding from TSP Payments

A distribution that a Thrift Savings Plan (TSP) participant receives from his or her traditional TSP account is subject to federal income tax withholding. A nonqualified distribution of a TSP participant’s Roth TSP account may be subject to federal income tax withholding. The amount of federal income tax withheld is equal to:

- 20 percent if the distribution is an eligible rollover distribution:

- 10 percent if it is nonperiodic distribution other than an eligible rollover distribution; or

- an amount determined as if the TSP participant were married with three withholding allowances, unless the TSP participant submits a federal income tax withholding certificate (Form W-4P), if it is a periodic distribution.

TSP participants can usually choose not to have federal income tax withheld from TSP payments other than eligible rollover distributions.

Filing Requirements for Federal Income Taxes

An annuitant does not have to file a federal income tax return in any year unless his or her gross income, which includes the taxable portion of the FERS or CSRS annuity, is more than a certain amount. The gross income filing requirements for the tax year are in the instructions for Form 1040.

A surviving spouse of a deceased federal employee or annuitant who is receiving a CSRS or FERS survivor annuity check will have to file a federal income tax return in any year that his or her gross income (including the taxable portion of the CSRS or a FERS survivor annuity check) together with other gross income is more than the annual filing requirement amount.

Form CSF 1099-R (Statement of Survivor Annuity Paid) is mailed each year by January 31 to survivor annuities receiving the survivor annuity benefits during the preceding calendar year. Some surviving spouses of a deceased federal employee or annuitant receive their own survivor annuity check and a survivor annuity for one or more children.

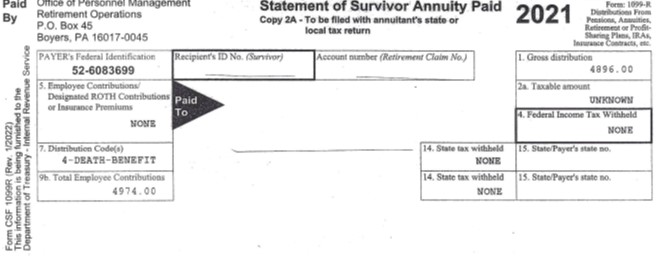

A sample 2021 CSF 1099-R is presented here:

Note that each child’s survivor annuity check counts as his or her income (not the surviving spouse’s) for federal income tax purposes. If a child can be claimed as a dependent of the surviving parent, then the taxable part of the child’s annuity should be treated as unearned income when applying the filing requirements for a dependent.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.