Understanding How Federal Employee Retirement Benefits Are Taxed by the IRS – Part II of a series of FEDZONE columns discussing how federal employee retirement benefits are taxed by the IRS

This is the second of a series of FEDZONE columns discussing how federal employee retirement benefits are taxed by the IRS. This column discusses how non-disability CSRS and FERS retirement annuities are taxed. Those employees who retire under a disability retirement receive what is called a CSRS or FERS disability retirement annuity. The taxation of disability retirement benefits will be discussed in a future FEDZONE column.

Shortly after retiring from federal service, a CSRS or FERS employee will receive from the Office of Personnel Management (OPM) a booklet that explains to the just-retired employee important items related to the employee’s recent retirement from federal service. Important items included in the booklet are: (1) the employee’s effective date of retirement and commencing date of the retired employee’s CSRS or FERS annuity; (2) the amount of the retired employee’s starting gross CSRS or FERS annuity; and (3) the retired employee’s total contributions (made via payroll deduction) to the CSRS or FERS Retirement and Disability Fund. Note that because an employee’s contributions to the CSRS or FERS Retirement and Disability Fund are made with after-taxed dollars, the total contributions represent the retired employee’s “cost” in his or her retirement. The total contributions information will be used to calculate the tax-free recovery of the total contributions during the employee’s years collecting his or her annuity as a CSRS or FERS annuitant.

A CSRS or FERS annuitant’s monthly annuity payment contains an amount on which the annuitant previously paid income tax while in federal service. This amount (made via payroll deduction every pay period) represents the annuitant’s contribution to the CSRS or FERS Retirement and Disability Fund. These contributions were deducted from the employee’s paycheck (with after-tax dollars) and then contributed to the CSRS or FERS Retirement and Disability Fund on behalf of the employee.

Note that if an annuitant (while in federal service) repaid any CSRS or FERS contributions that had been withdrawn when the annuitant previously left federal service but then returned to federal service, then those redeposits, and any interest paid are included in the annuitant’s “cost” in the plan. Also, any deposits made for military service or temporary federal service in which no contributions to either the CSRS or FERSR were made by the annuitant, and interest paid, are part of the “cost” in the retirement plan. In other words, both deposits and redeposits are included with regular employee contributions made via payroll deduction to the CSRS or FERS Retirement and Disability Fund and the total constitutes the annuitant’s “cost” in his or her CSRS or FERS retirement.

Recovering an Annuitant’s “Cost” in the Retirement Plan Tax-Free

Any employee who retired from federal service after Nov. 18, 1996, must use the Simplified Method to determine the tax-free recovery of the “cost” in either their CSRS or FERS retirement. Under the Simplified Method, an annuitant’s monthly annuity payment is made up of two parts: (1) The tax-free part that is a return of the annuitant’s “cost” in either the CSRS or FERS retirement; and (2) the taxable part that is the amount of the annuitant’s agency (s) contributions to the CSRS or FERS retirement on behalf of the retired employee and interest earnings that have accrued tax-deferred over the years within the retirement plan.

The tax-free portion of the annuity is a fixed dollar amount (as calculated by the Simplified Method, see below). The tax-free portion amount remains the same, even as the annuity increases over time with cost-of-living adjustments (COLAs).

CSRS or FERS Annuity Starting Date After July 1, 1986

If a federal annuitant’s annuity starting date is after July 1, 1986, then the total amount of CSRS or FERS annuity income that a CSRS or FERS annuitant (or the survivor annuitant) can exclude from taxation over the years cannot exceed the annuitant’s “cost” in the retirement. Any annuity payments an annuitant or a survivor annuitant receives after the “cost” in the plan has been recovered are fully taxable. The following example illustrates:

Example 1. Jeffrey retired from federal service in 2000 and contributed a total of $120,000 to the CSRS Retirement and Disability Fund during his 32 years of federal service. Under the Simplified Method (see next section) Jeffrey excludes $400 a month from federal and state tax. After 300 months (25 years), Jeffrey will have received all of his $120,000 “cost” in his retirement. Thereafter, his entire CSRS annuity will be fully taxable.

Simplified Method to Determine the Tax-Free Portion of a CSRS or FERS Annuity

Any federal retiree receiving a CSRS or FERS annuity after Nov. 18, 1996, must use the Simplified Method to figure the tax-free portion of the retiree’s CSRS or FERS annuity. Note that OPM has been determining the tax-free portion of the CSRS or FERS annuity since 2002. That means any federal employee who has retired from federal service since 2002 has seen on their CSA 1099-R statement (received every January reporting a summary of the previous year’s annuity payments) both the gross annuity and the taxable annuity portion that they had received during the previous calendar year. OPM is using the Simplified Method to determine the tax-free portion of a CSRS or FERS annuitant’s monthly annuity.

Under the Simplified Method, one determines the tax-free portion of each full monthly payment by dividing one’s “cost” in the retirement plan by the number of months based on one’s age in the year of the effective date of retirement. This number will differ depending on whether the annuity starting date is before Nov. 19, 1996, or after Nov. 18, 1996. If the annuity start is after 1997 and the annuity includes a survivor benefit for one’s spouse, then the number of months divisor factor is based on the combined annuitant’s age and the spousal survivor annuitant’s age in the year of the effective date of the retirement.

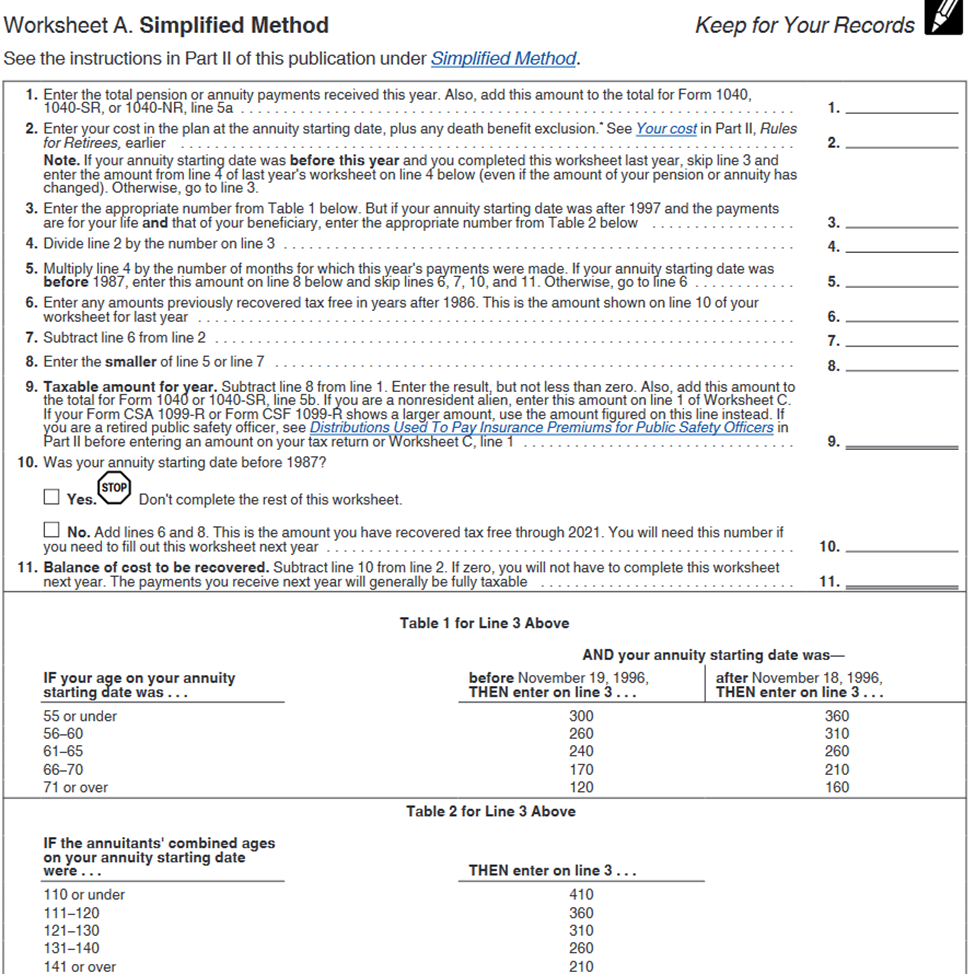

A copy of the Simplified Method worksheet (reprinted from IRS Publication 721) is presented below:

It is important to explain some important line items on the Simplified Method Worksheet:

• Line 2. “Your cost in the plan”. This amount represents the annuitant’s contributions to the CSRS or FERS Retirement and Disability Fund via payroll deductions while they were in federal service. It also includes deposits and interest paid for temporary service and/or military service and redeposits (and interest paid).

• Line 3. The number entered on Line 3 is the appropriate number from Table 1 or Table 2 (see above, Simplified Method Worksheet below line 11). For any annuity starting date after December 31, 1996, an annuitant uses: (1) Table 1 for a CSRS or FERS annuity without a survivor benefit; or (2) Table 2 for a CSRS or FERS annuity with a survivor benefit.

If the annuity starting date is before January 1, 1997, then Table 1 is used.

• Line 6. “Amounts previously recovered tax-free”. If an annuitant received CSRS or FERS retirement contributions before 2021, then the total amount of CSRS or FERS contributions recovered tax-free that the annuitant must enter on line 6 is the total amount from line 10 on the 2020 Simplified Method Worksheet.

The following example illustrates:

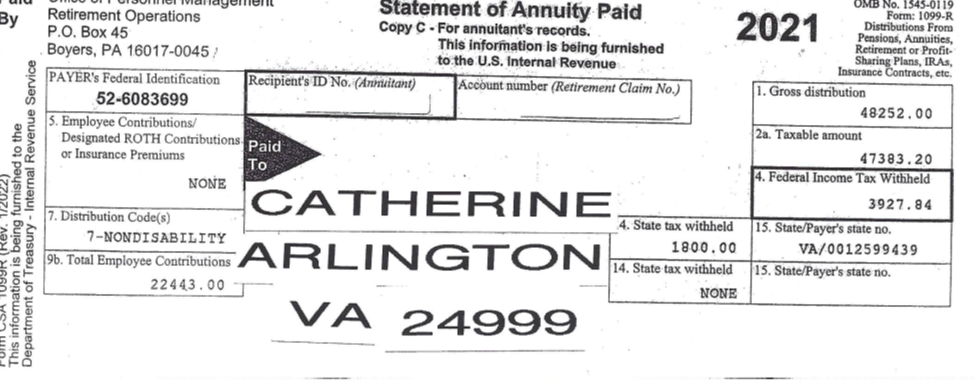

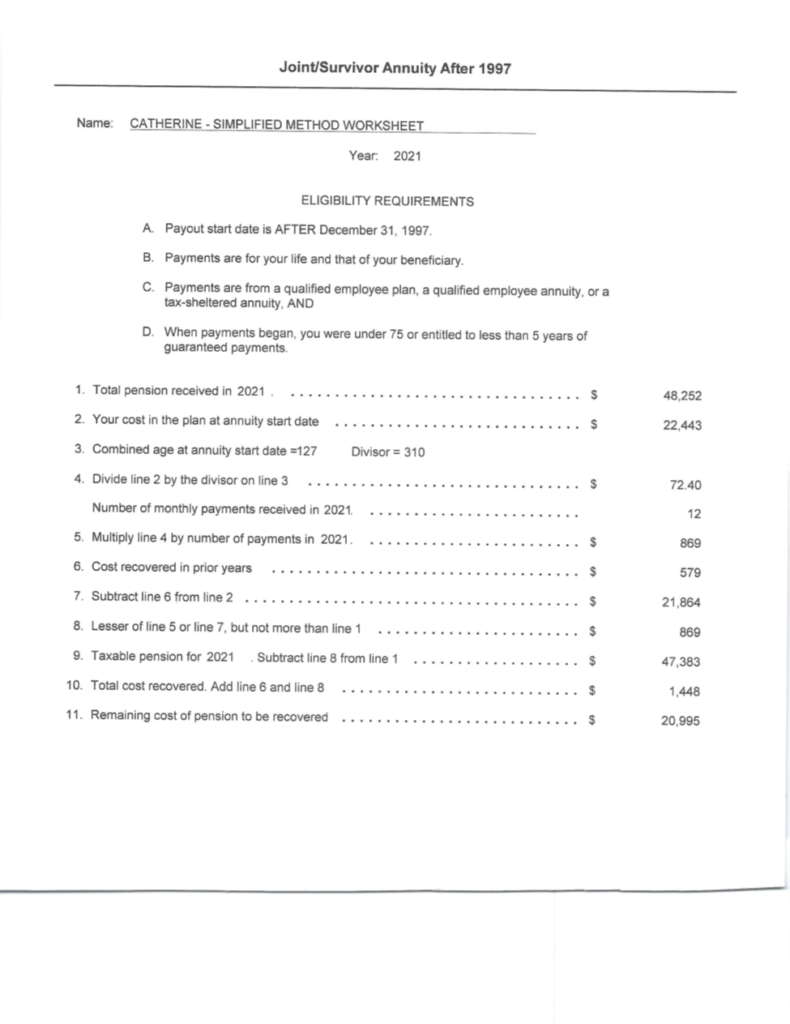

Example 2. Catherine retired from federal service after 32 years of federal service under FERS on March 31, 2020. Catherine is married to Ken and elected to give a full FERS spousal survivor annuity to Ken. Catherine’s 2021 Form CSA 1099-R is presented below (with all personal information not shown).

Note the following:

- Box 1: Gross distribution equals $48,252

- Box 2a: Taxable distribution equals $47,383

- Box 9b: Total employee contributions equals $22,443

To confirm that the taxable portion of her 2021 FESR annuity (equal to $47,383) is correct, Catherine uses the Simplified Method Worksheet, which is shown here:

Catherine’s gross annuity during 2021 was $48,252 or $48,252/12, $4,021 gross monthly annuity. Catherine had contributed a total of $22,443 to the FERS Retirement and Disability Fund during her 32 years of federal service. At her annuity starting date of April 1, 2020, she was age 66 and her husband Ken was 61 years old. The $22,443 is shown on line 2 of the Simplified Rule Worksheet.

To complete line 2 of the Simplified Method Worksheet, Catherine used Table 2 at the bottom of the worksheet and found that 310 is the number in the second column that includes 127 (Catherine’s and Ken’s combined ages). On line 3, Catherine puts 310. On line 4, Catherine divides the amount on line 2 ($22,443) by the amount on line 4 (310) and produces $72.40. The $72.40 represents the amount of Catherine’s monthly annuity that comes from the $22,443 and therefore is not taxable. By multiplying the $72.40 by 12 ($869), Catherine produces the annual portion of her annuity that is not taxable, shown on line 5. Since Catherine’s 2021 gross annuity was $48,252, her taxable annuity was $48,252 less $869, or $47,383, s shown on line 9 of the Simplified Method Worksheet and Box 2a of Catherine’s 2021 CSA 1099-R.

If Catherine does not live to collect 310 monthly payments and her husband Ken begins to receive monthly annuity payments (in the form of a spousal survivor annuity), Ken will also exclude $72.40 per month ($869 per year) from each of his monthly survivor annuity payments until 310 payments have been received (between Catherine and Ken). Catherine should also fill out and submit to OPM Form SF 3102 (Designation of Beneficiary FERS Contributions) naming someone other than Ken (such as children or siblings) as a beneficiary of any of her FERS contributions that were not paid to Catherine and Ken in the event both Catherine and Ken die before 310 months have elapsed since Catherine’s annuity starting date of April 1, 2020.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.