This is the fourth in a series of FEDZONE columns discussing how federal employee retirement benefits are taxed by the IRS. This column discusses how Social Security disability and retirement benefits are taxed.

This is the fourth in a series of FEDZONE columns discussing how federal employee retirement benefits are taxed by the IRS. This column discusses how Social Security disability and retirement benefits are taxed. There is also a discussion on some strategies to minimize the amount of federal and state income taxes that has to be paid in Social Security benefits.

The following are some key facts concerning how the IRS taxes Social Security benefits:

- 1. Up to 50 percent of an individual’s Social Security benefits are taxable for individuals with gross income (including 50 percent of Social Security benefits) of at least $25,000 (lower “base amount” for single or head of household tax filers) and less than $34,000 (upper “base amount” for single or head of household tax filers), or for a married couple filing jointly with a combined gross income (including 50 percent of Social Security benefits) of at least $32,000 (lower “base amount” for married filing jointly tax filers) and less than $44,000 (upper “base amount” for married filing jointly tax filers).

- 2. Up to 85 percent of an individual’s Social Security benefits are taxable for individuals with a gross income (including 50 percent of Social Security benefits) of at least $34,000, or for a married couple filing jointly with a combined gross income (including 50 percent of Social Security benefits) of at least $44,000.

- 3. Retirees who have minimum income other than Social Security benefits in most cases will not be taxed on their Social Security benefits.

- 4. Those retirees who own Roth accounts (Roth IRAs, Roth 401(k), Roth TSP) can minimize the amount of taxes they have to pay on their Social Security benefits.

How Social Security Income is Taxed

Before the year 1983, none of Social Security benefits were taxed. Starting in 1983, after Congress passed into law some major modifications to the Social Security system including raising the full retirement age from age 65 to age 67, the IRS started taxing Social Security benefits, but only for individuals whose total income exceeded certain limits. No inflation adjustments have been made to those income limits nearly 40 years later. This has resulted in most individuals receiving Social Security benefits and with other sources of retirement income (including nearly all federal annuitants and survivor annuitants) paying federal income tax on their Social Security benefits.

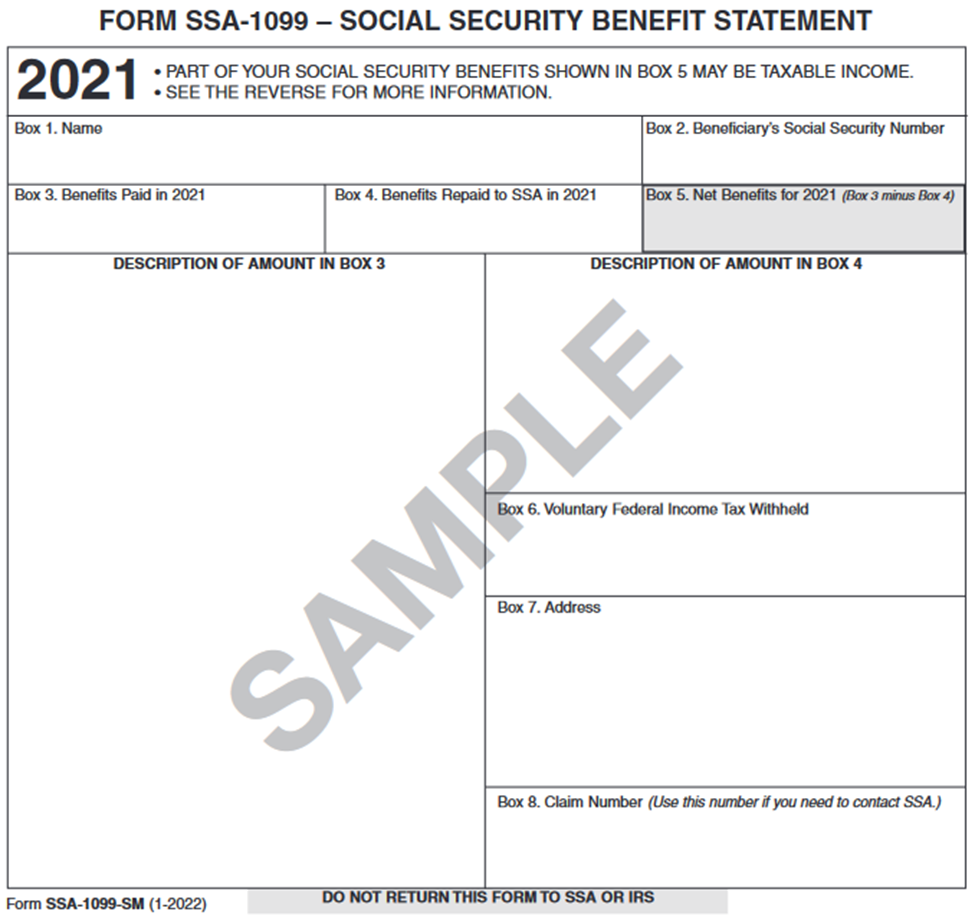

It is important to mention that under current IRS rules, no individual receiving Social Security benefits will pay federal income tax on all of their Social Security benefits, no matter how much income he or she has. The maximum amount of an individual’s Social Security benefits included in one’s income in any year is 85 percent of the total Social Security benefits received that year. The following is a worksheet used to determine how much of Social Security disability and/or retirement benefits that an individual receives during the year are taxable:

Worksheet Used to Determine Taxability of Social Security Benefits

| 1. Amount from Box 5 of all Forms SSA-1099 received for the year. Include the full amount of any lump-sum benefits received during the year for the current and any prior years ……… | 1)__________ |

| 2. One-half of the amount on line 1………………………………………………………………………………. | 2) _________ |

| 3. All other taxable income including pensions, wages, interest and dividends…………………… | 3)__________ |

| 4. Add any tax-exempt interest such as interest on municipal bonds ………………………………. | 4)__________ |

| 5. Add lines 2, 3, and 4 (“provisional income”) …………………………………………………………………… | 5)__________ |

The calculation begins with obtaining from Box 5 of Form SSA-1099 (“Net Benefits”) that a Social Security recipient receives in January following the year in Social Security benefits were paid. A sample Form 1099-SSA for the year 2021 is presented below. Included in Box 5 is the full amount of any lump-sum benefits received during the year for the current and any prior years. Once that amount is obtained, 50 percent of that income is then added to other income including pensions, traditional IRA distributions, wages, interest, dividends, capital gains, net rental income and other reportable income. In addition, tax-exempt interest (such as interest on municipal bonds) is added on line 4 to the other income on lines (2) and (3). The resulting “provisional income” is line 5 of the worksheet above.

The amount on line 5 (“provisional income”) is compared to the “base amounts”, discussed above, depending on whether an individual is single or married, namely: (1) Single individual with “provisional income”- from $25,000 to $34,000, the individual may have to pay federal income tax on up to 50 percent of his or her benefits. If “provisional income” is more than $34,000; the individual may have to pay federal income tax on up to 85 percent of his or her Social Security benefits; (2) Married (filing joint) with “provisional income” from $32,000 to $44,000, the married couple may have to pay federal income tax on up to 50 percent of their combined Social Security benefits. If “provisional income” more than $44,000, the couple may have to pay federal income tax on up to 85 percent of their combined Social Security benefits.

The following example illustrates:

Carl and Patricia are each age 67, with each receiving Social Security benefits during 2021 and filing a joint tax return for 2021. In January 2022, Carl received a 2021 Form 1099-SSA showing net benefits of $15,378 in Box 5. Patricia received a 2021 Form 1099-SSA showing net benefits of $24,774 in Box 5. In addition to Social Security retirement benefits, Carl and Patricia had $142,460 of other income. They did not receive any tax-exempt income nor any adjustments to their income. They used the Social Security Benefits worksheet tax above to determine how much of their Social Security benefits will be included in their taxable income for 2021:

Worksheet Used to Determine Taxability of Social Security Benefits

| 1. Amount from Box 5 of all Forms SSA-1099 received for the year. Include the full amount of any lump-sum benefits received during the year for the current and any prior years ……… | 1) $40,152 |

| 2. One-half of the amount on line 1………………………………………………………………………………. | 2) $20,076 |

| 3. All other taxable income including pensions, wages, interest and dividends…………………… | 3) $142,460 |

| 4. Add any tax-exempt interest such as interest on municipal bonds ………………………………. | 4) $0 |

| 5. Add lines 2, 3, and 4 (“provisional income”) …………………………………………………………………… | 5) $162,536 |

Since Carl and Patricia file as married filing joint and line (5) (“provisional income”) is more than $44,000, 85 percent of their total Social Security benefits received during 2021 ($40,152 as shown on line 1 of the worksheet) is taxable and added to their taxable income for 2021.

0.85 times $40,152 equals $34,129

Carl and Patricia must include $34,129 of Social Security retirement benefits to their other income of $142,460 resulting in total taxable income of $176,589 for 2021.

Social Security Benefits Tax Tool

The IRS has an Interactive Tax Assistant (ITA) (found here) that will assist individuals determine how much of their Social Security benefits are taxable. IRS Publication 915 (Social Security and Equivalent Railroad Retirement Benefits) discusses the tax rules associated with Social Security and equivalent Railroad Retirement benefits. Publication 915 may be downloaded here.

Taxability of Social Security – Spousal, Survivor and Disability Benefits

Spousal Benefits Including Widow/Widower Survivor Benefits

Those individuals who receive Social Security benefits of their own but who are eligible and collect a higher spousal Social Security benefit, the rules on taxation of benefits are the same as for all other Social Security recipients. That is, if an individual’s “provisional income” is above $25,000 and less than $34,000, then the individual will owe taxes on up to 50 percent of the total Social Security benefit. The percentage increases to 85 percent if the individual’s “provisional income” is above $34,000.

Survivor Benefits Paid to Children

Survivor benefits paid to children are rarely taxed because few children have other income that reaches the taxable ranges. The parents or guardians who receive the benefits on behalf of the children do not have to report the benefits as part of their income.

Disability Benefits

Social Security disability benefits follow the same rules on taxation as the tax rules applied to Social Security retirement benefits.

State Taxes on Social Security Benefits

Thirteen states – Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, North Dakota, Rhode Island, Utah, Vermont and West Virginia – tax at some portion of an individual’s Social Security benefits. As with how the federal government taxes Social Security benefits, how a state taxes Social Security benefits varies by income and other criteria.

Three Ways to Avoiding or Minimizing Taxes on Social Security Benefits

The most obvious way to keep Social Security benefits from being taxed is to keep one’s adjusted gross income and tax-exempt interest income below the thresholds that would result in some of the benefits being subject to federal income tax. For most retirees, that strategy may not be a realistic way to live and being able to pay their bills. But there are some ways to limit the amount of federal income tax that an individual has to pay on their Social Security benefits. These ways are presented here:

• Keeping some retirement income in Roth accounts.

Qualified Roth IRA and Roth TSP withdrawals are income tax-free and therefore not included in adjusted gross income. Distributions from Roth accounts will therefore will not affect the taxable income calculation of Social Security benefits.

• Withdraw fully taxable retirement income before starting to receive Social Security benefits.

Another suggested way to minimize the taxable amount of Social Security benefits is to withdraw more fully taxable retirement income before starting to receive Social Security benefits. For example, if an individual is at least age 59.5, then the individual can make penalty-free withdrawals from traditional IRAs. Although federal and state income taxes have to be paid in the year withdrawals are made, the after-taxed withdraw funds can be reinvested into non-retirement accounts and subsequently withdrawn at any time. The strategy is to withdraw the fully taxable retirement accounts before one starts to receive Social Security in order to reduce the amount of taxable income by the time one starts his or her Social Security. This strategy has another benefit; namely: By making these withdrawals to boost one’s income when an individual is just retired, then the individual might be able to delay applying for Social Security benefits, which will increase the amount of their Social Security monthly payments.

• Buy a qualified longevity annuity (QLAC) contract.

A QLAC is a deferred annuity funded with a lump sum direct transfer of funds from a qualified retirement plan or a traditional IRA. QLACs can provide monthly payments for life. As long as the QLAC complies with IRS requirements, it is exempt from the required minimum distribution (RMD) rules until payouts begins at the mandatory starting date of age 85. By reducing mandatory withdrawals from traditional IRAs and qualified retirement plans (minimizing RMDs) and therefore decreasing taxable income during one’s post-age 72 years (when RMD rules apply), QLACs can help minimize adjusted gross income and the amount one’s Social Security benefits subject to income tax. Under current rules, an individual can transfer up to 25 percent or $135,000 (whichever is less) of a traditional IRA to purchase a QLAC with a single premium.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.