This column discusses the mortgage interest income tax deduction changes resulting from the passage of the One Big Beautiful Bill Act of 2025 (OBBBA). Before discussing these changes which could affect individual tax returns starting the 2026 tax year, it is important to review the history of federal income tax mortgage interest deduction.

The Revenue Act of 1913 (which established the federal income tax) allowed for all interest paid on personal indebtedness – which included all types of interest paid, such as credit cards, personal loans, etc.

The Tax Reform Act of 1986 overhauled the tax code, eliminating most personal interest deductions including credit card interest, car loan interest, and interest on personal bank loans. However, mortgage interest on a primary residence and one second home (such as a vacation home) was preserved. Internal Revenue Code (IRC) section 163 (h) allowed interest on up to $1 million of “acquisition indebtedness” as a potential deduction. IRC section 163(h) also limited deductible “home equity” interest to the interest paid on up to $100,000 of home equity debt.

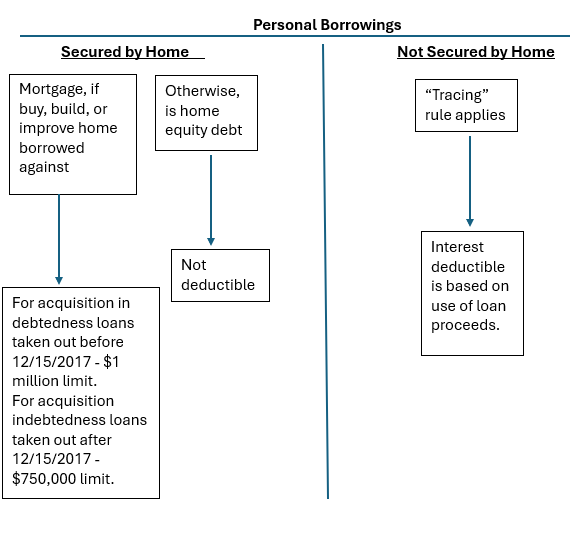

IRC section 163(h) defines acquisition indebtedness as any indebtedness which: (1) Is incurred in acquiring, constructing or substantially improving any qualified residence of an individual; and (2) Is secured by such residence. The Tax Cuts and Jobs Act of 2017 (TCJA) imposed a new limit of $750,000 of acquisition indebtedness on new mortgage loans taken out after December 15, 2017, and eliminated the deduction for home equity interest.

OBBBA Changes to the Mortgage Interest Deduction

Section 70108 of the OBBBA permanently extended the IRC section 163(h) $750,000 limitation on mortgage interest from “acquisition indebtedness” allowed for the mortgage interest deduction after December 31, 2025. In addition, mortgage insurance premium paid after December 31,2025 are now considered as paid mortgage interest starting after December 31, 2025.

Some Discussion on the Mortgage Deduction Resulting from TCJA and OBBBA Changes

Mortgage interest on both - in total and not individually – on a primary and one secondary residence may be deducted starting January 1,2026 as an itemized deduction on Schedule A, subject to the following limitations:

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

‧ Mortgages taken out before October 13, 1987. For these mortgages (“grandfathered debt”) there are no limits on deductible interest paid on both the first (primary) and the second home acquisition indebtedness . “Grandfathered debt” which has been refinanced after October 13,1987 qualifies as “grandfathered debt” only to the extent of the grandfathered debt refinanced, and only to the extent of the remaining term of the original grandfathered debt. Additional debt over the grandfathered amount is treated as acquisition debt, if used for capital improvements, or equity debt.

‧ Interest paid on mortgages after October 13, 1987. Interest paid on mortgages taken out after October 13,1987 and before December 15,2017 to buy, build, or improve a home, (called home acquisition debt) is fully deductible. This is provided that throughout the tax year these mortgages, plus any grandfathered debt totaled $1 million or less ($500,000 if filing as married filing separately). After December 15, 2017, the acquisition limit indebtedness is $750,000.

The following examples illustrate:

Example 1. Joan purchased a home (principal residence) for $250,000 in 2014 and borrowed $200,000 of qualified acquisition debt. In 2025, when the remaining mortgage principal balance was $140,000, Joan refinanced with a new $200,000 mortgage. Joan’s acquisition debt remains at $140,000 – interest on that portion of the new mortgage is fully deductible, and home equity debt is $60,000. This assumes that none of the $60,000 was used for home improvements.

Example 2. Warren purchased a home (principal residence) for $250,000 in 2015 and borrowed $200,000 of qualified acquisition debt. In 2025, when the remaining mortgage balance due was $140,000, Warren refinanced with a new $200,000 mortgage and used the additional $60,000 of borrowed money to renovate a kitchen (capital improvement). The entire $200,000 debt is acquisition debt and fully deductible on Schedule A as mortgage interest.

Example 3. Francine purchased a home (principal; residence) for $250,000 in 2016 and borrowed $200,000 as qualified acquisition debt. In 2025, when the remaining balance due was $40,000, Francine refinanced with a new $200,000 mortgage. Acquisition debt is now only $40,000; home equity debt is $100,000 and personal debt is $60,000. This is assuming that the refinancing proceeds were used for improvements. Note that none of the interest paid on the $60,000 personal debt is deductible unless the entire proceeds are used for capital improvements to the home – such as renovating a kitchen and/or bathroom or building onto the home.

The passage of the TCJA resulted in the removal of the deduction for the interest on home equity debt. TCJA became effective January 1, 2018. OBBBA extended the removal of the home equity loan interest deduction past December 31,2025 when the removal was due to expire. OBBBA permanently extends the removal of the interest deduction on home equity debt. This means that the interest paid on home equity loans is not deductible except for interest paid on home equity loans used to buy, build or improve the home borrowed against.

The following chart summarizes interest paid on personal debt:

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

You Might Also Enjoy This Podcast

Ed Zurndorfer, EA, ATA, CFP®, CLU®, ChFC®, CEBS®, ChFEBC℠: Federal Employee Benefits Expert

A former career Federal employee, Ed has published a staggering 1,200+ separate articles on Federal Benefits and Retirement!

Just “Google” his name, and you are likely to find a plethora of sites that contain his writings. Drawn to its mission to reach, teach

and serve Feds, Serving Those Who Serve is the only financial planning practice with which Ed has chosen to affiliate in over

20 years teaching. In addition to conducting Federal Benefits seminars for Serving Those Who Serve, you can find Ed’s

writings here on our blog in the FedZone, and on Fed-Soup, MyFederalRetirement, FederalNews Radio and NITP.

He is a member of the Maryland Society of Accountants, the National Association of Enrolled Agents, the International Society of Certified Employee Benefits Specialists, the Financial Planning Association, the National Association of Health Underwriters,

and the Society of Financial Service Professionals. Since 1999, Ed has taught many thousands of Federal employees about

their benefits, in person and at Federal agencies all over the country. Ed is a true national treasure.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.