This is the first of four FEDZONE columns discussing the withdrawal options that are available to separated Thrift Saving Plan (TSP) participants. In these columns, a “separated” TSP participant means a civilian federal employee or a member of the uniformed services who has separated from that employment. A “beneficiary” TSP participant is a spouse beneficiary of a deceased civilian or deceased uninformed service TSP participant who had a TSP account established in his or her name. These columns will present information about the TSP withdrawal process, the rules that govern withdrawals, and the tax implications of each withdrawal option.

Given that a TSP participant may need their TSP retirement savings to last into their 90’s, there are some questions a TSP participant should ask himself/or herself before deciding to withdraw from their TSP account, including:

- When should the participant start withdrawing the account?

- How much does the participant think things will really cost during the participant’s retirement?

- Will the participant have enough income to cover all their expenses during retirement?

- Will the participant’s savings last for his or her whole life?

- Does the participant need to provide income for is or her dependents or heirs?

Leaving One’s Money in the TSP

Unless a TSP participant is subject to required minimum distribution (RMDs) or has a total TSP account balance of less than $200 (this includes the combined balance of the traditional TSP and the Roth TSP), there are no requirements for a TSP participant to make withdrawals from his or her TSP account. The entire account can be left in the TSP, continuing to grow over-time tax-deferred in the traditional TSP, and tax-free over-time in the Roth TSP. However, a retired TSP participant is not allowed to make direct contributions to either their traditional TSP or to their Roth TSP accounts. This is because all direct contributions to TSP accounts must be made payroll deduction. Separated participants can make indirect contributions to TSP accounts by transferring funds into their traditional TSP accounts via direct rollovers from traditional qualified retirement plans (401(k), 403(b) plans, SEP-IRAs, SIMPLE IRAs) and traditional contributory IRAs. They can also transfer funds into their Roth TSP accounts via direct rollovers from Roth qualified retirement plans (Roth 401(k), Roth 403(b) and Roth 457 plans). Note that Roth IRAs are not allowed to be directly rolled over to a Roth TSP account. Also, a TSP beneficiary participant is not permitted to directly rollover retirement accounts to either their traditional beneficiary TSP account or to their Roth beneficiary TSP account.

There are three basic methods of withdrawing money from a TSP account as a separated or beneficiary participant: (1) Installment payments; (2) Partial/total/distributions; and (3) Annuity purchases. This column discusses TSP installment payments.

A TSP participant can choose to receive installment payments from their account monthly, quarterly (every three months) or annually. A TSP participant may schedule a date up to six months in the future for these installments to begin. These payments will continue until the TSP participant stops them, or until the TSP total account balance equals zero. This is true even if the TSP participant chooses to have the installment payments come from the traditional TSP balance first or from the Roth TSP account balance first. When the TSP participant runs out of money in the participant’s chosen TSP account, then payments will continue from the TSP account that the TSP participant did not choose.

There are two ways of setting the payment dollar amount, a fixed dollar amount or payments based on life expectancy. Both payment methods are discussed.

- (1) Installment payments of a fixed dollar amount. The TSP participant chooses the amount he or she wants to receive. Minimum payment is $25.

Making changes to fixed dollar installment payments

A TSP participant can stop or make changes to his or her fixed dollar installment payments at any time. Using My Account, the TSP participant can stop existing installments and request new installments. To make certain changes without stopping the TSP installment payments, the TSP participant must call the ThriftLine (1-877-968-3778).

To make the following changes to installments, the TSP participant must first stop existing installment payments and then request new installment payments, which the TSP participant can perform going online to My Account or by calling the ThriftLine (1-877-968-3778):

- start, stop, or change direct deposit of the TSP participant’s installments if payments go to more than one destination.

- change the dollar amount of the TSP participant’s payments.

- change the frequency (monthly, quarterly or annually) of the TSP participant’s payments.

- change the source TSP account (traditional TSP or Roth TSP) of the TSP installments (traditional, Roth, or both).

- change the installment type (fixed dollar amount or based on life expectancy).

- switch from the Single Life Table to the Uniform Lifetime Table when taking required minimum distributions (RMDs).

A TSP participant can make the following changes without stopping installments if the TSP participant calls the ThriftLine (1-877-968-3778):

- start, stop, or change direct deposit of the TSP participant’s installments if payments go to a single destination.

- change the amount of the TSP participant’s federal income tax withholding.

- start rolling over traditional TSP money (not Roth TSP money) from the TSP participant’s installment payments to a traditional IRA or to an eligible employer-sponsored traditional qualified retirement plan (only if installments are of a fixed dollar amount and expected to last less than 10 years).

- change or stop rollovers (if the TSP participant is currently doing rollovers).

Expected duration of installment payments and federal income tax withholding.

The rules for federal tax withholding and eligibility to roll over money to an IRA or to an eligible employer plan are different depending on how long your installments are expected to last. The TSP determines the expected duration of a TSP participant’s installment payments using the TSP participant’s account balance, the payment amount the TSP participant has chosen, and an assumed earnings rate.

If the expected duration of a TSP participant’s installments is less than 10 years, the following IRS rules apply:

- The TSP must withhold 20 percent in federal income taxes of any amount that a TSP participant did not roll over for federal income tax.

- The TSP participant can instruct the TSP to withhold a percentage that’s greater than 20 percent, but you cannot have less federal income withheld or waive federal income tax withholding.

- The TSP participant may roll over all or part of a traditional TSP account installment payments to a traditional IRA or to an eligible employer-sponsored traditional qualified retirement plan.

If the expected duration of the TSP participant’s installment payments is 10 years or more or they are based on life expectancy, the following IRS rules apply:

The TSP is required to withhold federal taxes from any taxable amount as if the TSP participant is single with zero exemptions unless the TSP participant elects a different option (installments payments initiated before 2023 will continue to have withholding as if the TSP participant is married with three dependents unless the TSP participant chooses a different option or does so in the future ). The TSP participant can request that a different percentage be withheld or that nothing be withheld.

- The TSP participant cannot roll over any part of his or her annual TSP required minimum distribution (RMD) to an IRA or eligible employer plan.

The following events will trigger a recalculation of a TSP participant’s expected installment duration:

- The TSP participant changes the dollar amount or frequency of installment payments.

- The TSP participant makes a rollover contribution to his or her TSP account.

- The TSP participant takes a distribution or purchases a TSP annuity in addition to the TSP participant’s installment payments.

- (2) Installment payments based on life expectancy. A TSP participant will have the TSP compute the annual distribution (and paid in 12 equal monthly payments) based on one of two IRS life expectancy tables. The initial payment will be based on the TSP participant’s age and the participant’s traditional TSP account balance at the time of the first payment. Note that life expectancy payments are calculated using the participant’s entire traditional TSP account balance. Each January, the TSP will recalculate the amount of the installment payment for that year. The recalculation will be based on the TSP participant’s current year age and the traditional TSP account balance at the end of the preceding year.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

- As mentioned above, the TSP uses one of two IRS life expectancy tables to compute the annual distribution: The following is information about these life expectancy tables:

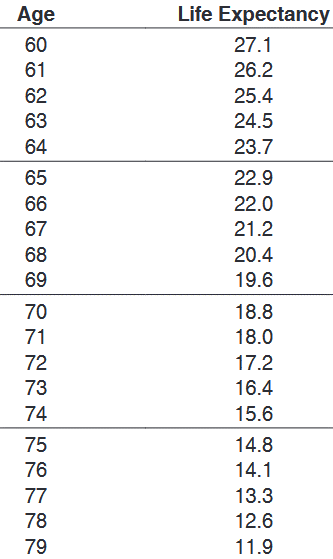

IRS Life Expectancy Tables—IRS Single Life Table, Treas Reg § 1 401(a)(9)-9, Q&A 1, is used to calculate

installments based on life expectancy for participants who have not yet reached the required minimum

distribution (RMD) age when installments begin. These participants may choose to switch to the Uniform

Lifetime Table, Treas Reg § 1 401(a)(9)-9, Q&A 2, when they reach RMD age This decision cannot be

Reversed. The Uniform Lifetime Table will be used for participants who have already reached the RMD age

when payments begin There is no option to switch to the Single Life Table for these participants.

A portion of the IRS Single Life Table, Treas Reg § 1 401(a)(9)-9, Q&A 1 is presented here*:

*From 2025 IRS Publication 590-B (https://www.irs.gov/pub/irs-pdf/p590b.pdf)

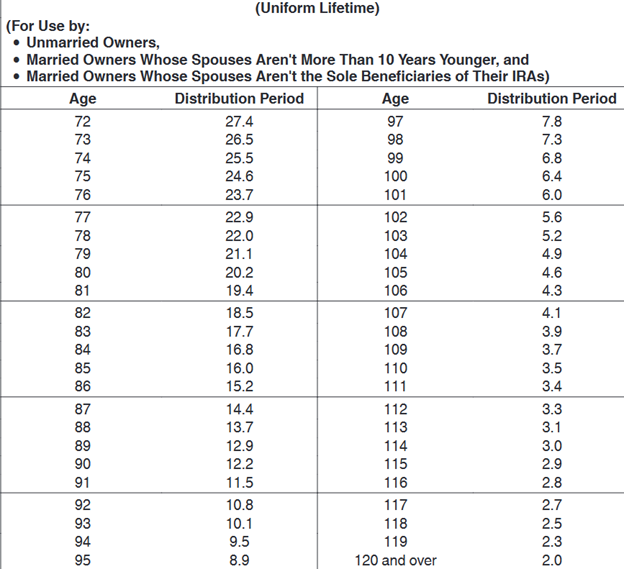

A portion of the Uniform Lifetime Table, Treas Reg § 1 401(a)(9)-9, Q&A 2 is presented here*::

*From 2025 IRS Publication 590-B (https://www.irs.gov/pub/irs-pdf/p590b.pdf).

The following is an example of a federal employee who retired from federal service and elected TSP installment payments based on life expectancy:

(1) Name of TSP participant: George

(2) Age of participant: 65

(3) Retired from Federal service on December 31,2021 at age 65..

(4) About one month after retiring from federal service, George requests online (using Form TSP-99: Withdrawal Request for Separated and Beneficiary Participants – Civilians) that starting immediately (for the year 2022) he will receive monthly payments based on life expectancy from his traditional TSP account. His traditional TSP account balance as of 12/31/2021 was equal to $1,100,000.

(6) The TSP will compute George’s monthly payments for the year 2022 based on the $1,100,00 account balance as of 12/31/2021, and George’s single life expectancy (age 66 during 2022) from the IRS’ “single life expectancy table” (shown above). Monthly payments in future years will be recomputed based on the account balance on the previous December 31 and George’s new life expectancy factor.

For 2022 (when George will become age 66): George’s annual payment is computed as follows:

$1,100,000 (account balance as of December 31,2021)/22.0 (life expectancy factor for age 66)

= $50,000 (annual payment for the year 2022)

or $4,166 (monthly payment for the year 2022)

George’s annual and monthly TSP payments for the years 2022-2025 based on life expectancy are summarized in the following table:

George’s TSP Installment Payments Based on Life Expectancy for the Period 2022 -2025

|

Year |

(a)

Account Balance Previous Dec. 31 |

John’s Age |

(b)

Life Expectancy Factor* |

(c)

(a)/(b) Annual Payment |

(d)

(c)/12 Monthly Payment |

|

2022 2023 2024 2025

|

$1,100,000 $1,062,300 $1,015,245 $973,580

|

66 67 68 69

|

22.0 21.2 20.4 19.6

|

$50,000

$50,108 $49,617 $49,672 |

$4,167

$4,176 $4,135 $4,139 |

*Single Life Expectancy Table.

Some observations from the table that illustrates George’s annual and monthly payments for the years 2022 through 2025:

- As George gets older, the life expectancy factor decreases.

- George’s $1,100,000 starting traditional TSP account balance (as of 12/31/2021) generally decreases through the years. His annual payment will fluctuate from one year to the next depending on the investment performance of the account during the year.

- If George is concerned or uneasy with the variation in the annual payment for the purpose of meeting his annual budget needs, he is allowed to switch to fixed dollar installment payments (monthly, quarterly or annually) (minimum monthly amount $25) that he can increase, decrease, or even stop.

- If George does switch to fixed dollar payments, then effective January 1,2021 under the new TSP rule (effective August 2020) George can switch back to receiving payments based on life expectancy.

- Once George becomes age 73 (reaches his required beginning date and therefore his traditional TSP account is subject to required minimum distributions), he can switch to the Uniform Lifetime Table in the determination of his annual payment. The reason that George may want to make that switch is because the life expectancy factors in the Uniform Lifetime table are generally larger than the life expectancy factors in the Single Life Expectancy table. This switch may result in a smaller annual payment (and therefore smaller federal and state income tax liabilities on traditional TSP payments).

- Before George reaches his required beginning date of age 73 in 2029, the TSP will withhold from each monthly payment a minimum 20 percent federal income tax. Once George turns 73 and informs the TSP to use the Uniform Lifetime Table to compute his monthly payment, the TSP will hold a minimum 10 percent federal income tax.

- The TSP does not withhold state income taxes from traditional TSP payments. If George lives in a state which has a state income tax, then George must make arrangements to pay the state income tax due on his traditional TSP payments.

- To request a fixed installment payment or installment payments based on life expectancy, a TSP participant must log into his or her “My Account” at www.tsp.gov and check on the “Withdrawals and Changes to Installment Payments” link on the menu. From there, a TSP participant will have access to an online tool with which to start withdrawals.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

You Might Also Enjoy This Podcast

Ed Zurndorfer, EA, ATA, CFP®, CLU®, ChFC®, CEBS®, ChFEBC℠: Federal Employee Benefits Expert

A former career Federal employee, Ed has published a staggering 1,200+ separate articles on Federal Benefits and Retirement!

Just “Google” his name, and you are likely to find a plethora of sites that contain his writings. Drawn to its mission to reach, teach

and serve Feds, Serving Those Who Serve is the only financial planning practice with which Ed has chosen to affiliate in over

20 years teaching. In addition to conducting Federal Benefits seminars for Serving Those Who Serve, you can find Ed’s

writings here on our blog in the FedZone, and on Fed-Soup, MyFederalRetirement, FederalNews Radio and NITP.

He is a member of the Maryland Society of Accountants, the National Association of Enrolled Agents, the International Society of Certified Employee Benefits Specialists, the Financial Planning Association, the National Association of Health Underwriters,

and the Society of Financial Service Professionals. Since 1999, Ed has taught many thousands of Federal employees about

their benefits, in person and at Federal agencies all over the country. Ed is a true national treasure.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.