The Tax Cuts and Jobs Act of 2017 (TCJA) made two changes to the state and local taxes deduction included as an itemized deduction on IRS Form 1040 Schedule A. These two changes were: (1) Foreign real estate property taxes are not deductible; and (2) An aggregate deduction limit applies to state and local income taxes, real and personal property taxes, and local general sales taxes. The limit is called the State and Local Tax (SALT) limit and was $10,000 ($5,000 for individuals filing married filing separately).

The One Big Beautiful Bill Act of 2025 (OBBBA) which was passed into law in July 2025, increases the SALT deduction cap from $10, 000 ($5,000 if married filing separately) to $40,000 ($20,000 if married filing separately). The amount is set to increase to $40,400 in 2026 and will then be indexed for inflation annually before it reverts back in 2030 to the $10,000 cap that it was during the years 2018 through 2025.

The increase cap on SALT is subject to a “phaseout” for individuals with modified adjusted gross income (MAGI) above $500,000 ($250,000 for individuals filing as married filing separately). MAGI is calculated by taking an individual’s adjusted gross income (AGI) and adding back specific deductions and non-taxable income including student loan interest, deductible IRA contributions, foreign earned income and tax-exempt interest. The increased $40,000 SALT cap is reduced by 30 percent of the excess MAGI over $500,000 ($250,000) but not below $10,000 ($5,000). The phase down threshold is also increased by 101 percent for each subsequent taxable year after 2025.

The SALT deduction cap under OBBBA applies to state and local real and personal property taxes, state and local general sales taxes, and state, local and foreign income, war profits and excess profit taxes. Tables 1 and 2 respectively illustrate the SALT deduction cap and the MAGI “phaseout” per the OBBBA:

Table 1. SALT Deduction Cap1 for the Years 2025 through 2029

| Tax Year | SALT Deduction Cap2 | MAGI Phaseout Threshold3 |

| 2025 | $40,000 | $500,000 |

| 2026 | 40,400 | 505,000 |

| 2027 | 40,804 | 510,050 |

| 2028 | 41,212 | 515,150 |

| 2029 | 41,624 | 520,302 |

| 2030 and forward | 10,000 | N/A |

1 These amounts reflect MFJ filing status. For MFS, the amounts are half of the amounts listed in the table.

2 The SALT deduction cap and the MAGI phaseout threshold both increase by 1% each year through 2029. Starting in 2030, the SALT deduction cap reverts to $10,000 ($5,000 MFS) and the phaseout rules no longer apply.

3 For 2025 – 2029, the increased cap is phased out for high-income taxpayers by 30% of the excess MAGI over the threshold, but the deduction cannot be reduced below $10,000.

Table 2. MAGI “Phaseout” for the Year 2025

| MAGI | Phaseout Amount1 | SALT Deduction |

| $500,000 | 0 | $40,000 |

| 510,000 | 3,000 | 37,000 |

| 520,000 | 6,000 | 34,000 |

| 530,000 | 9,000 | 31,000 |

| 540,000 | 12,000 | 28,000 |

| 550,000 | 15,000 | 25,000 |

| 560,000 | 18,000 | 21,000 |

| 570,000 | 21,000 | 18,000 |

| 580,000 | 24,000 | 15,000 |

| 590,000 | 27,000 | 13,000 |

| 600,000 | 30,000 | 10,000 |

| >610,000 | 30,0002 | 10,000 |

1 The phaseout amount is calculated as 30% of the excess of MAGI over $500,000 for 2025.

2 For MAGI above $600,000, the deduction remains at $10,000 due to the statutory floor.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

The following three examples illustrate SALT limit and the MAGI “phaseout” for the year 2025:

Example 1. During 2025, Howard and Elizabeth, who live in New York, paid $24,500 in state and local income taxes. They also paid in property taxes $15,500. For tax year 2025, Howard and Elizabeth itemize their deductions on Schedule A and their 2025 MAGI is $398,500. Since state and local tax deductions total $40,000 and their MAGI is below the phaseout threshold of $500,000 for 2025, Howard and Elizabeth can deduct the entire $40,000 as a SALT deduction for 2025.

Example 2. During 2025, Vincent paid a total of $30,000 in state and local taxes and $15,700 in property taxes. Vincent’s 2025 MAGI is $317,500. Although Vincent’s MAGI for 2025 is less than $500,000, Vincent is limited to the SALT deduction cap of $40,000.

Example 3. Francine paid a total of $26,000 in state and local income during 2025 and $7,000 in property taxes. Her MAGI during 2025 is $530,000. Since her MAGI is over the $500,000 “phaseout” threshold, the SALT deduction will be reduced below $40,000 cap. At $530,000 MAGI, the phaseout is 30% x ($530,000 - $500,000) = $9,000. Francine’s maximum 2025 SALT deduction is equal to $40,000 - $9,000, or $31,000.

These are hypothetical stories and not indicative of any specific situations or client. It is presented only as an example and not intended as investment advice. Investing involved risk and there is no assurance that any investment strategy will be successful.

Some Other Issues Related to the SALT Deduction

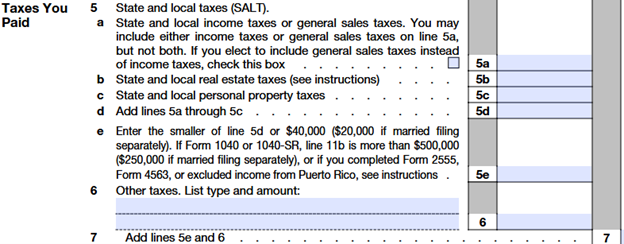

The following is a snapshot of the SALT deduction that appears on the IRS Form 1040 Schedule A:

Some discussion on what appears in lines 5 through 7:

- State and local income taxes. State and local income taxes are potentially deductible on Schedule A in the year paid. The taxes paid may be paid either through payroll withholding, estimated tax payments or payments from prior year state income tax returns.

- State and local sales taxes. Individuals can elect to deduct state and local sales taxes rather than state and local income taxes. Individuals who make the election (by checking the box on line 5a Schedule A) can deduct either: (1) The actual sales tax amounts they spent during 2025 based on their records; or (2) Predetermined deduction figures from IRS tables. A Sales Tax Deduction Calculator can be found at: www.irs.gov/credits-deductions/individuals/use-the-sales-tax-deduction-calculator

In addition to the IRS sales tax table amounts, an individual can also deduct actual sales tax amounts from purchases of motor vehicles, including leased vehicles. If the sales tax on a motor vehicle is higher than the general rate, then only the amount that would have resulted from charging the lower general sales tax rate.

- Real estate taxes. A real estate taxi is deductible in the year it is both paid and imposed or assessed. Prepaid real estate taxes can generally be deducted in the year of prepayment. This is true if an individual is on a cash basis and does not live in an area in which the prepayment would be considered a deposit by the taxing authority. Penalties and interest imposed on late payments are not deductible.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

You Might Also Enjoy This Podcast

Ed Zurndorfer, EA, ATA, CFP®, CLU®, ChFC®, CEBS®, ChFEBC℠: Federal Employee Benefits Expert

A former career Federal employee, Ed has published a staggering 1,200+ separate articles on Federal Benefits and Retirement!

Just “Google” his name, and you are likely to find a plethora of sites that contain his writings. Drawn to its mission to reach, teach

and serve Feds, Serving Those Who Serve is the only financial planning practice with which Ed has chosen to affiliate in over

20 years teaching. In addition to conducting Federal Benefits seminars for Serving Those Who Serve, you can find Ed’s

writings here on our blog in the FedZone, and on Fed-Soup, MyFederalRetirement, FederalNews Radio and NITP.

He is a member of the Maryland Society of Accountants, the National Association of Enrolled Agents, the International Society of Certified Employee Benefits Specialists, the Financial Planning Association, the National Association of Health Underwriters,

and the Society of Financial Service Professionals. Since 1999, Ed has taught many thousands of Federal employees about

their benefits, in person and at Federal agencies all over the country. Ed is a true national treasure.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.