April 1,2025 is the deadline for federal employees and retirees born between January 1 and December 31 ,1951 owning traditional IRAs to take their first traditional IRA required minimum distribution (RMD) for the year 2024. This column discusses what a traditional IRA RMD is and how the RMD is calculated.

What is a traditional IRA RMD?

A traditional IRA RMD is the minimum amount a traditional IRA RMD owner must withdraw from their traditional IRA account every year once the traditional IRA owner reaches his or her required beginning date (RBD). Until January 1, 2020, the RBD was April 1 following the year the traditional IRA owner became age 70.5. With the passage of the SECURE Act in December 2019, the RBD was changed as shown in the following table.

|

Year Of Birth |

Required Beginning Date (RBD): April 1 following the year traditional IRA owner becomes ......... |

| Before July 1, 1949

July 1, 1949 – December 31, 1950 January 1, 1951 – December 31, 1959 After December 31, 1959 |

70.5

72 73 75 |

For the first year, only a traditional IRA owner must take their traditional IRA RMD no later than April 1 following the year they become aged 70.5, 72,73, or age 75. Subsequent RMDs in future years must be taken by December 31 of that year.

From the table, any federal retiree or employee born during 1951 and who owns any type of traditional IRA - a contributory traditional IRA, a rollover traditional IRA, a SEP traditional IRA, or a SIMPLE traditional IRA - must take his or her first traditional IRA RMD by April 1, 2025.

How is the traditional IRA RMD calculated?

A traditional IRA RMD is calculated for any year using the following steps:

Step 1. For all traditional IRAs owned, obtain the account balance of each traditional IRA owned as of December 31 of the previous year and add up the account balances.

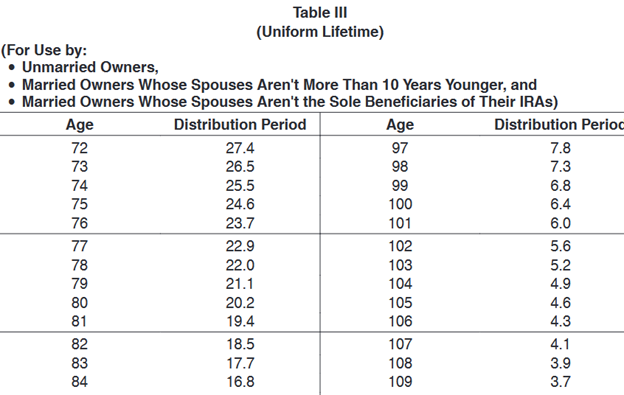

Step 2. Divide the total traditional IRA balance as of December 31 of the prior year obtained in Step 1 by a life expectancy factor available in IRS Publication 590-B (Distributions from Individual Retirement Arrangements), available at https://www.irs.gov/pub/irs-pdf/p590b.pdf. A traditional IRA owner will select one of two life expectancy tables depending on his or her situation. The following is a description of each table:

- Uniform Lifetime Table III. This table is used if a spouse is not the sole traditional IRA beneficiary, or a spouse is the sole beneficiary and is not more than 10 years younger than the traditional IRA owner.

- Joint and Last Survivor Table II. This table is used if the sole beneficiary of the traditional IRA is a spouse, and the spouse is more than 10 years younger than the traditional IRA owner.

The following presents a portion of Table III (Uniform Lifetime) from IRS Publication 590-B:

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

Note that while a traditional IRA owner who owns multiple traditional IRAs must calculate the annual RMD for each IRA and add up the RMDs to determine the total annual RMD, the total RMD may be taken from any one or a combination of the traditional IRAs owned. The following example illustrates:

Carolyn, a federal retiree, became aged 73 in October 2024. She owns three traditional IRAs. Her first traditional IRA RMD is due no later than April 1, 2025. One of her contributory traditional IRAs (Traditional IRA 1) had an account balance of $22,300 on December 31, 2023. A second contributory IRA (Traditional IRA 2) had an account balance of $56,725 on December 31, 2023. Carolyn also owns a rollover traditional IRA (traditional IRA 3). She rolled over her traditional TSP to the rollover traditional IRA 3) after retiring from federal service in 2019. Traditional IRA 3 had a balance of $877,528 as of December 31, 2023.

The combined balance of Carolyn’s three traditional IRAs as of December 31,2023 is:

$22,300 + $56,725 + $877,528 = $956,553.

Carolyn is married and named her spouse, who is two years older than Carolyn, as the sole beneficiary of her traditional IRAs.

Using the IRS’ Table III (Uniform Lifetime), Carolyn calculates her first year (2024) traditional IRA RMD as follows:

Combined traditional IRA balance as of December 31, 2023/Table III (Uniform Lifetime) life expectancy (age 73) equals.

$956,553/26.5 years = $36,096.34

Note the following:

- Carolyn has until April 1,2025 to withdraw her $36,096.34 traditional IRA RMD for the year 2024.

- Carolyn can withdraw the $36,096.34 from traditional 2 or traditional IRA 3 or spread the withdrawal over traditional 1, traditional 2, and traditional 3.

- Carolyn must take a second traditional IRA RMD during the year 2025. This second traditional IRA RMD is for the year 2025 and must be taken no later than December 31, 2025. The 2025 traditional IRA RMD is calculated based on Carolyn’s total traditional IRA balance as of December 31,2024 and Carolyn’s life expectancy factor from Table III (Uniform Lifetime) for age 74, equal to 25.5. This is because Carolyn will be aged 74 during 2025.

Other information with respect to traditional IRA RMDs

Traditional IRA owners should be aware of the following with respect to traditional IRA RMDs:

- Although most traditional IRA custodians will calculate the traditional IRA RMD for a traditional IRA owner, a traditional IRA owner is ultimately responsible for taking the correct traditional IRA RMD each year.

- Prior to the passage of SECURE Act 2.0, the IRS penalty for not taking the correct traditional IRA RMD was 50 percent of what should have been withdrawn by the IRA owner but was not. SECURE Act 2.0 decreased the excess penalty to 25 percent (possibly 10 percent if the RMD deficiency is corrected within two years).

- A traditional IRA owner subject to the annual traditional IRA RMD is allowed to withdraw more than the annual RMD in any year. However, a distribution in excess of the RMD for one year cannot be applied to the RMD for the next year.

- The excess penalty for not taking a traditional IRA RMD can be waived if the traditional IRA owner can establish that the traditional IRA RMD withdrawal shortfall was due to reasonable error and that reasonable steps are being taken to remedy the RMD shortfall. In order to qualify for IRS relief, the IRA owner must file IRS Form 5329 (Additional Taxes on Qualified Plan Including IRAs and Other Tax-Favored Accounts) and attach a letter of explanation.

- A traditional IRA RMD cannot be directly rolled over into another tax-deferred traditional account, including a traditional qualified retirement plan (401(k) and 403 (b) plan), the traditional TSP, or another traditional IRA.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

You Might Also Enjoy This Podcast

Ed Zurndorfer, EA, ATA, CFP®, CLU®, ChFC®, CEBS®, ChFEBC℠: Federal Employee Benefits Expert

A former career Federal employee, Ed has published a staggering 1,200+ separate articles on Federal Benefits and Retirement!

Just “Google” his name, and you are likely to find a plethora of sites that contain his writings. Drawn to its mission to reach, teach

and serve Feds, Serving Those Who Serve is the only financial planning practice with which Ed has chosen to affiliate in over

20 years teaching. In addition to conducting Federal Benefits seminars for Serving Those Who Serve, you can find Ed’s

writings here on our blog in the FedZone, and on Fed-Soup, MyFederalRetirement, FederalNews Radio and NITP.

He is a member of the Maryland Society of Accountants, the National Association of Enrolled Agents, the International Society of Certified Employee Benefits Specialists, the Financial Planning Association, the National Association of Health Underwriters,

and the Society of Financial Service Professionals. Since 1999, Ed has taught many thousands of Federal employees about

their benefits, in person and at Federal agencies all over the country. Ed is a true national treasure.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.