In January 2025, federal agencies were directed to end remote work, requiring their employees to return to the office full-time.

As a Fed, you could be okay with the RTO mandate. Perhaps you like the idea of in-person collaboration and a separation between the workplace and your home life.

On the other hand, you might be reluctant to come back due to long commutes, a lack of flexibility and the potential for work-life erosion. You could dislike the idea so much that you’re considering early retirement.

However, you should consider several factors before impulsively separating from your federal career. Whether you’re nearing retirement age or are ten years or more from that event, it’s essential to determine:

- How early retirement might impact your benefits

- If you’re prepared for an early retirement

Consideration #1: Pension and Other Benefits

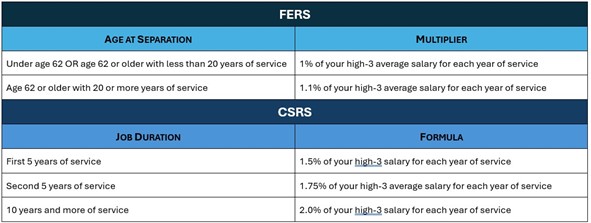

Your retirement benefits are handled by the

- CSRS: Civil Service Retirement System if you were hired before 1987

- FERS: Federal Employees Retirement System if you were hired in 1987 or later

You contribute a certain amount each month to fund your retirement, and you receive annuities when you separate from your government job. An early retirement could impact your retirement distributions.

To determine how much you might receive for an early retirement, the formula consists of:

- The average of your highest earnings over three years (“high-3”)

- A multiplier, representing a percentage for each year of your service

Additional issues to consider with early retirement include the following.

Social Security

Early retirement might also impact your Social Security benefits. You could apply for and start receiving your Social Security benefits at 62. However:

- What you receive at 62 is less than what you receive at full retirement age (see the chart below)

- Once you apply for those benefits, that’s the amount you receive for the rest of your life (aside from Cost of Living Adjustments)

- You will receive your largest distribution when you apply for benefits at age 70

As such, it’s important to determine your Social Security benefits before deciding on the early retirement route.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer –

FERS: Thrift Savings Plan

If you’re contributing to the FERS Thrift Savings Plan (TSP), your payout could be lowered if you retire early. And if that retirement occurs before the age of 59 1/2, https://www.fedweek.com/tsp/tsp-early-withdrawal-penalty-roth-and-traditional/ in addition to being taxed as ordinary income.

Additional Benefits

If you separate from service before retirement age, you could continue your Federal Employee Health Benefits as long as you:

- Retire on an immediate FERS or CSRS pension

- Have been continuously enrolled in any FEHB plan for five years before your retirement date

Also, you can continue with your Federal Employees’ Group Life Insurance (FEGLI) if you separate from your job before age 65. You’ll be responsible for paying premiums until age 65. At that point, you can select free coverage (free from premiums). In exchange, your coverage is reduced.

Options like VERA or discontinued service retirement are making the possibility of retiring before MRA with benefits increasingly possible in the current federal government environment. You can learn more about those options by registering for our SPECIAL “Early Retirement Planning for Federal Employees” webinar here.

Consideration #2: Assessing Early Retirement Readiness

Part of early retirement readiness means understanding your income and expenses after you leave your job. If you find that your calculated income won’t cover anticipated expenses in retirement, consider:

- Participating in a phased planor part-time work options

- Increase contributions to your retirement annuity (CSRS) or TSP (FERS)

It’s also a good idea to enlist the assistance of experienced CERTIFIED FINANCIAL PLANNERS™ like those with Serving Those Who Serve. These fed-focused experts can analyze your retirement readiness and advise you on improving income through contributions and investments. These CFP profeesionals® can also work with you on a separation strategy from your federal job.

Deciding on Your Departure

Early retirement could offer a solution if the federal government’s return-to-office mandate has you concerned or anxious. However, you should definitely figure out your expenses, income, and other issues before taking that step. This is a measure twice, cut once situation.

CPFs® at Serving Those Who Serve are on hand to advise you about CSRS/FERS retirement and in-office mandates. These skilled professionals can work with you on developing a workable plan, whether you stay in place or plan to separate from your job.

To schedule a no-obligation meeting, visit stwserve.com or email [email protected].

The information has been obtained from sources considered reliable but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of Serving Those Who Serve writers and not necessarily those of RJFS or Raymond James. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Investing involves risk and you may incur a profit or loss regardless of strategy suggested. Every investor’s situation is unique and you should consider your investment goals, risk tolerance, and time horizon before making any investment or financial decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. **