This is the first of two FEDZONE columns discussing the tax consequences of selling one’s personal residence.

Edward A. Zurndorfer

Although the COVID-19 pandemic wreaked havoc on many parts of the U.S. economy during 2020, one part of the U.S. economy had an exceptional year. Residential real estate sales soared to their best year ever in many parts of the U.S, partially a result of the lowest mortgage rates in sixty years. Perhaps even better news is that most residential homeowners sold their homes during 2020 at a net gain.

Two questions for personal residence owners who sold their residences now arise, namely: (1) What are the tax consequences of selling one’s personal residence at a net gain; and (2) how a personal residence sale is reported on one’s 2020 federal income tax return. This is the first of two FEDZONE columns discussing the tax consequences of selling one’s personal residence.

The following are the tax rules with respect to the sale of an individual’s primary personal residence, as detailed in Internal Revenue Code (IRC) Section 121.

- A primary personal residence is an individual’s main personal residence and may include: (1) a house; (2) a houseboat; (3) a mobile home; (4) a cooperative apartment or condominium; or (5) a home outside the United States. Vacant land is not considered part of the main home unless the main home is adjacent to the land containing the home and the vacant land is used as part of the main home for pleasure or for recreation.

- Only the sale of the primary personal residence qualifies for the personal residence capital gains tax exclusion (discussed in next week’s FEDZONE column). A secondary personal residence or a vacation home sale is potentially taxable. It is impossible to have two primary personal residences at the same time. The following examples illustrate:

Example 1. Jean owns a home located in Washington, DC. She also owns a home in Boca Raton, Florida which she uses during the winter (December, January and February). The house in Washington, D.C. is Jean’s primary personal residence because she lives there most of the calendar year.

Example 2. Peter owns a home in Fairfax, VA, but he lives in Ft. Lauderdale, Florida, in a home that he rents. The home in Ft. Lauderdale is his main home and would not qualify for the capital gain exclusion if sold because he rents it and does not own it.

Individuals who live in more than one residence use the simple rule of where they live for most of the year in order to determine their primary personal residence. In some situations, other factors may be involved, including: (1) Place of employment; (2) location of family members’ main home; (3) mailing address; (4) legal address for tax returns, driver’s license; (5) banking location; and (6) location of clubs and churches to which taxpayer belongs.

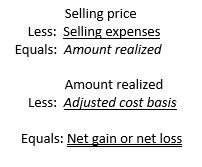

Determining Gain or Loss Upon the Sale of Primary Personal Residence

The following is a short version of determining the gain or loss resulting from the sale of a personal residence:

Note the following:

- The selling price does not include personal property such as furniture.

- The selling price does include mortgages or notes assumed by the personal residence purchaser.

- Payments from an employer to an employee (the home seller) to reimburse for a loss on a home sale are included on the employee’s Form W-2 in the year of sale and should not be included as part of the selling price.

IRS Form 1099-S (Proceeds from Real Estate Transactions) is used to report the home sales price. Some problems associated with Form 1099-S include: (1) the form does not include loan assumptions or services rendered; and (2) the form may not be issued if the settlement company (or settlement real estate attorney) believes that the entire sale proceeds are excludable from taxation (the exclusion of capital gains tax upon the sale of a personal residence is discussed in the next FEDZONE column).

Other Points Related to Primary Personal Residence Sales

- Foreclosures and repossessions are also treated as sales;

- Transfers to a spouse as a result of a divorce are generally not taxable or reportable;

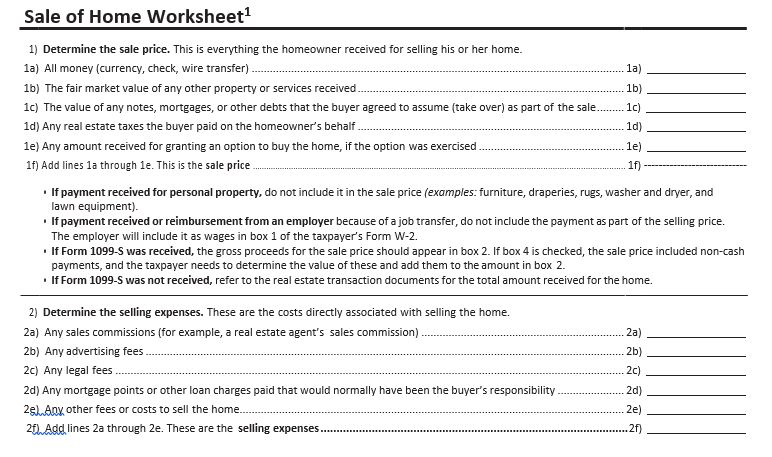

- Selling expenses include a number of items as reprinted below from The Tax Book: Sale of Home Worksheet;

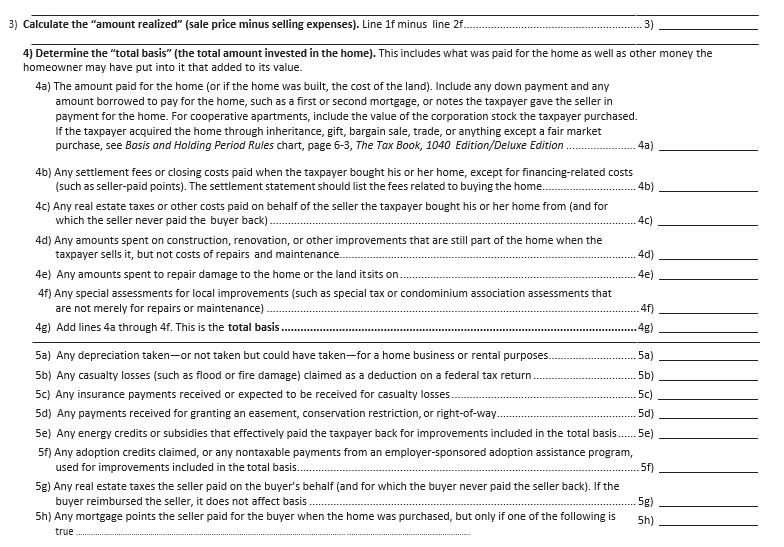

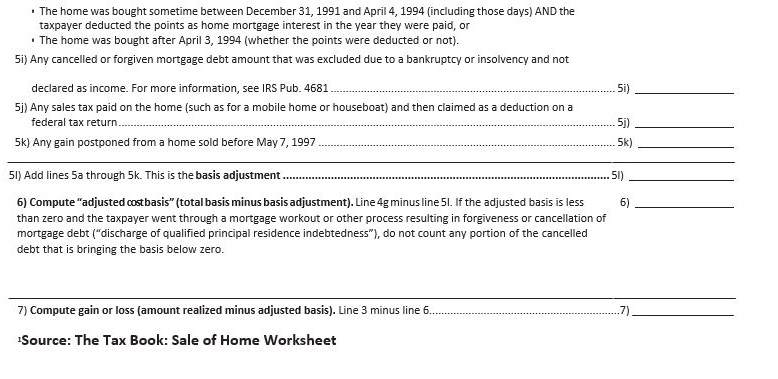

- Adjusted or total basis includes purchase price plus any improvements the homeowner may have made to the home that added to its value.

The worksheet below summarizes how the amount realized or adjusted cost basis in the home are calculated:

If the there is a net gain on line 7, then the net gain may qualify for a capital gains exclusion from taxation. If there is a net loss on line 7, the net loss cannot be deducted on one’s income taxes. But in case of a net loss, the home seller does not need to pay any tax on the net sale proceeds received from selling the home.

The next FEDZONE column will discuss the reporting of a personal residence home sell on one’s federal income tax return, including calculating the exclusion of capital gain from taxation.

You Might Also Enjoy This Podcast:

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.