This is the second FEDZONE column discussing the tax consequences of selling one’s personal residence. Read Part One Here.

Edward A. Zurndorfer

The previous FEDZONE column discussed the tax consequences of selling one’s primary personal residence at a net gain or net loss. The column explained that a home sale resulting in a net gain is potentially taxable while a home sale resulting in a net loss is not tax deductible. But the net proceeds from a home sale resulting in a net loss are not taxable.

This week’s column discusses when the sale of a personal residence results in a net gain and can be excluded from federal income taxes under Internal Revenue Code Section 121. The exclusion from tax applies to an individual’s primary personal residence, and not to a second home, a vacation home or a to rental property.

An individual can exclude from income up to $250,000 of capital gain from the sale of a personal residence if the following three tests are met:

- Ownership. The individual must have owned the personal residence for at least two of the five years prior to its sale.

- Use. The individual must have used the personal residence for at least two of the five years prior to the sale (two years do not need to be consecutive).

- Frequency limitation. The exclusion applies to only one sale every two years.

Note the following: (1) a personal residence sale gain attributable to a period of nonqualified use cannot be excluded from taxation. A period of nonqualified use is generally any time (after 2008) that the property is not used as the individual’s primary personal residence; (2) unmarried individuals who jointly own a primary principal residence may each exclude up to $250,000 of capital gain if the three tests above (ownership, use and frequency) are met.

Capital Gain Exclusion Rules for Married Couples

Married couples filing a joint return can exclude up to $500,000 of capital gain under the following conditions:

- Ownership. Either or both spouses must have owned the personal residence for at least two of the five years prior to the sale.

- Use. Both spouses must have used the personal residence as their primary residence for at least two out of the five years prior to the sale.

- Frequency limitation. During the two-year period ending on the date of the sale, neither spouse excluded gain from the sale of another personal residence.

Note that on a married filing joint tax return, up to $500,000 of capital gain can be excluded from capital gains tax as long as either spouse meets the ownership test. Both spouses must meet the use test and neither spouse has excluded a capital gain in the last two years. The following example illustrates:

Example. Carl purchased a home for $150,000 on May 20, 2005. On June 30,2014, Carl married Susan who then moved into Carl’s house. They sell the house on August 1, 2021 for $650,000. They can exclude the entire $500,000 of capital gain because Carl meets the two-year ownership test and both spouses meet the two-year use and frequency test.

Variation. Same facts except that Susan did not move into the house until she and Carl were married on February 1, 2020. On August 1, 2020, when they sell the home Susan does not meet the use test. Carl can exclude only $250,000 of gain even if they file married filing joint.

If both spouses own homes and each meets the ownership, use and frequency tests, then each spouse can exclude up to $250,000 of gain on his or her own home. The following example illustrates:

Example. On June 15, 2020, Larry and Janice got married and purchased a new home. During 2020, they both sold personal residences they both had previously owned and lived in for more than two out of the last five years. Neither Larry nor Janice had excluded a personal residence capital gain in the prior two years. Larry recognized a capital gain of $180,000 upon the sale of his personal residence and Janice recognized a capital gain of $400,000 upon the sale of her personal residence. Their total capital gain exclusion is $180,000 (Larry) and $250,000 (Janice- her capital gain exclusion is limited to $250,000), or $400,000. Larry may not exclude any of Janice’s excess capital gain.

Surviving Spouses

The $500,000 capital gain exclusion amount that applies to individuals filing a joint tax return also applies to unmarried surviving spouses if the sale occurs within two years of the death of their spouses. To qualify: (1) either the surviving spouse or the deceased spouse must meet the two-year ownership requirement for the residence immediately before the spouse dies; (2) both spouses must meet the two-year use requirement immediately before the spouse dies; and (3) neither of the spouses may have used the exclusion during the past two years. The following example illustrates:

Example. Howard and Betty are married and have owned and used their personal residence since March 1, 2002. On April 17, 2020, Howard died, and Betty inherits his interest in the home. IF Betty sells the residence before April 17, 2022, she will qualify for the $500,000 capital gain exclusion.

The above rule for a surviving spouse does not apply if the surviving spouse remarries before the sale of the personal residence within the two-year period. Also, the above rule for a surviving spouse will be most useful in the case of surviving spouse who solely owned the personal residence. In that case, the cost basis of the personal residence will not be stepped up to its fair market value when the other spouse dies. If the spouse who died had an ownership interest in the personal residence, some or all of the cost basis will usually be stepped up to 50 percent of the home’s fair market value on the day of death. This will likely reduce the amount of capital gain on a subsequent sale.

Suspending the Ownership and Use Test Periods

Certain individuals can elect to suspend for up to 10 years the five-year period for the ownership and use test. The election is available for any period that they (or their spouses) are on “qualified official extended” duty. To be on “qualified official extended” duty, the individual or the individual’s spouse must also be: (1) serving at a duty station at least 50 miles from the individual’s primary personal residence; or (2) residing in government quarters under government orders.

Eligible individuals include: (1) members of the Uniformed Services (Army, Navy, Air Force, Marines, Coat Guard); (2) members of the Foreign Service; (3) members of the Intelligence community (CIA, Homeland Security); (4) Peace Corps employees outside the U.S.; and (5) Peace Corps volunteers and volunteer leaders serving outside of the U.S. The following example illustrates:

Example. Curt bought and moved into a personal residence in 2011. He lived there as his primary personal residence for three years through 2014. For the next six years, he did not live in it because he was on qualified official extended duty overseas in the Foreign Service. He then sold his personal residence in 2020 at a gain. To meet the “use test”, Curt elected to suspend the five-year rule test period for the six years he was on qualifying official extended duty. He meets the ownership and use tests because he owned and lived in the home for three years during the test period.

Two-Year Rules

The following is a summary of the two-year test rules for excluding the $250,000/$500,000 capital gain resulting from the sale of a personal residence:

- The two-year periods for ownership and use do not have to be at the same time, nor do they have to be continuous.

- The actual rule states 24 full months or 730 days during the 5-year period, ending on the date of sale.

- Short absences for vacations or seasonal reasons, even if rented out during that period, are counted as periods of use.

- Death of spouse before sale – as long as the surviving spouse does not remarry before the sale date, the deceased spouse’s time of ownership and use counts as the surviving spouse’s time.

- A home transferred from one spouse to the other spouse in a divorce also transfers the ownership period.

Reduced Exclusion Rules

Individuals who do not meet the two-year ownership and use tests or who use the $250,000/$500,000 capital gains exclusion more than once in a two-year period may qualify for a reduced exclusion. A reduced exclusion is available if the primary reason the individual sold his or her primary personal residence was due to: (1) change in place of employment; (2) health; or (3) unforeseen circumstance. Note that for each of these reasons a “safe harbor” is available. If the safe harbor is not met, an individual can still satisfy the conditions based on facts and circumstances.

- Change in place of employment. A reduced exclusion will apply if the individual’s primary reason for the sale is a change in the location of a qualified individual’s employment. A qualified individual includes: (1) the personal residence owner or a spouse; (2) a co-owner of the personal residence; or (3) another individual whose main home is the same as the personal residence owner.

- Health. The sale is due to health if the primary reason for the sale is to obtain, provide, or facilitate the diagnosis, cure, mitigation or treatment of disease, illness, or injury of a qualified individual. The sale of a home is not because of health if the sale merely benefits a qualified individual’s general health or well-being. Qualified individuals include: (1) the personal residence owner or spouse; (2) co-owner of the residence; (3) parent; (4) grandparent; (5) stepmother or stepfather; (6) child; grandchild, stepchild or adopted child (7) brother or sister; (8) mother-in-law; (9) uncle or aunt; (10) nephew or cousin; (11) brother-in-law or sister-in-law; or (12) son-in-law or daughter-in-law. A “safe harbor” is based on a doctor’s recommendation. If, for one or more of the reasons listed above, a doctor recommends a change of residence, the primary reason for the sale in considered to be due to health.

- Unforeseen circumstances. Reduced exclusion rules if the primary reason for the sale is the occurrence of an event the individual did not anticipate before purchasing and occupying the residence. An individual does not qualify for a reduced capital gains exclusion if the primary reason for the sale is a preference for a different home or an improvement in financial circumstances. Safe harbor is based on a specific event.

The following events qualify as unforeseen circumstances: (1) an involuntary conversion of the home; (2) natural or man-made disasters; (3) loss of job resulting in being eligible for unemployment compensation; (4) divorce or legal separation; (5) multiple births resulting from the same pregnancy.

Reduced Exclusion Calculation

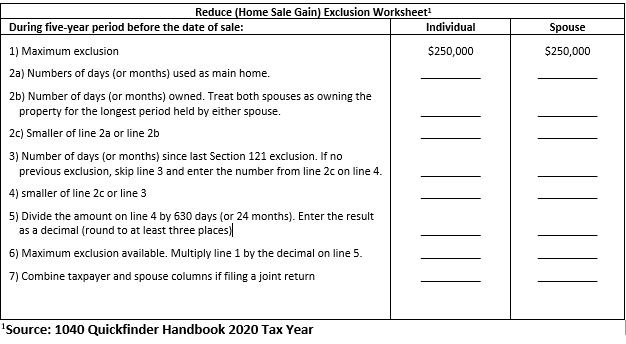

Pro-rated capital gain exclusion is based on the smaller of the time period the homeowner meets the ownership and use requirements of the time period between the most recent sale of a home using the $250,000/$500,000 exclusion and the current sale. Either days or months (but not both) can be used in the calculation. The following is a reduced home sale gain exclusion worksheet:

The following example illustrates: Frank and Joan, a married couple, bought their home in Virginia on May 1, 2019. They lived in the home for 13 months. Due to a job relocation, they sell the Virginia home on June 1, 2020 and move to Chicago. Since the move was job-related, they qualify for a reduced exclusion, shown as follows:

Number of months owned and used as main home…………………………….13

Divided by 24 months = 13/24………………………………………………………0.542

Multiply by $500,000 (maximum exclusion) = 0.542 x $500,000…. $271,000

The result is that Frank and Joan can exclude up to $271,000 of capital gain on a house they owned for only 13 months.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.