IRS Form 5498 (IRA Contribution Information) is vitally important for individuals who own any type of Individual Retirement Arrangement (IRA). The Form 5498 is completed by every IRA custodian meaning that any individual who owns multiple IRAs will likely receive more than one Form 5498.

Form 5498 is an informational reporting form and not filed with an IRA owner’s federal income tax return. The form is provided to both the IRA owner and to the IRS. IRA custodians have until May 31 (about six weeks after the April 15 filing deadline) to release the form. IRA owners can expect to receive their 2025 Form 5498 by May 31, 2026.

Many federal employees and retirees own different types of IRAs including contributory traditional IRAs and Roth IRAs, rollover traditional IRAs and rollover Roth IRAs, and converted Roth IRAs. Some may also own SEP IRAs and SIMPLE IRAs. To help these employees and retirees understand Form 5498, this column explains some of the important details reported on the form.

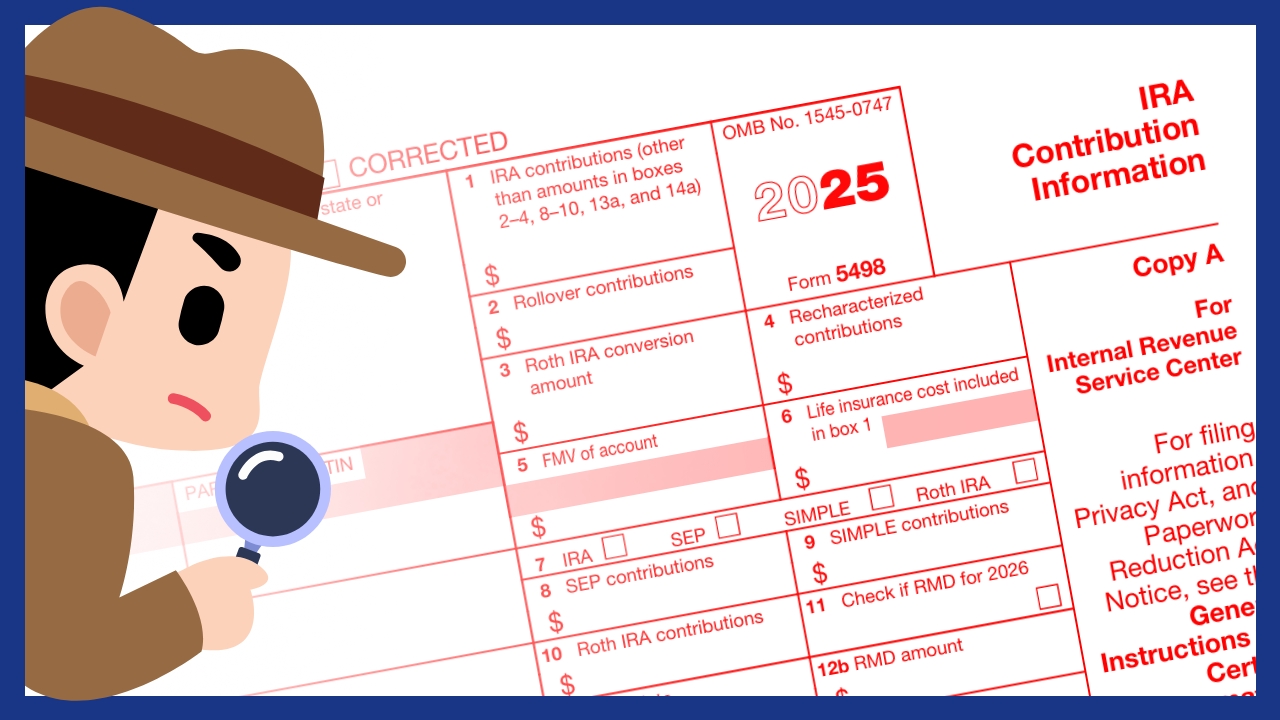

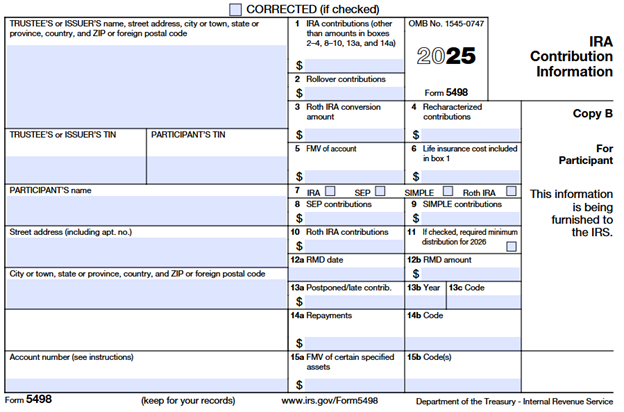

The following is a copy of the 2025 Form 5498:

The following presents a brief discussion and explanation of the information shown in the various boxes of IRS Form 5498:

- Box 1 (IRA contributions). This box shows the amount of traditional IRA contributions for the previous year (the year noted on the top right-hand corner of the form). Note that since Form 5498 is not released until after the individual income tax filing deadline of April 15, Box 1 will also include traditional IRA contributions made between January 1 and April 15 of the current year. These IRA contributions were made for the previous year. If traditional IRA contributions were made between January 1 and April 15 of the current year, then these traditional IRA contributions will appear in Box 1 of Form 5498 for the following year. The following examples illustrate:

Example 1. Joan made a $7,000 traditional IRA contribution in February 2026. She specified to her custodian that her IRA contribution is for 2025.In late May 2026, Joan will receive a 2025 Form 5498 from her IRA custodian showing a $7,000 traditional IRA contribution for calendar year 2025.

Example 2. Phillip made a $7,000 traditional IRA contribution in March 2026. He specified to his IRA custodian that his IRA contribution is for 2026, not for 2025. In late May 2027, Phillip will receive a 2026 Form 5498 from his IRS custodian showing a $7,000 traditional IRA for calendar year 2026.

Note that Box 1 of Form 5498 does not specify whether the traditional IRA contribution is deductible or not deductible. It only shows that a traditional IRA contribution was made. To report a nondeductible traditional IRA contribution, the traditional IRA owner must report the contribution on IRS Form 8606 (Nondeductible IRA) as part of that year’s federal income tax return. A deductible traditional IRA contribution will appear on the traditional IRA owner’s federal income tax return as an adjustment to income.

- Box 2 (Rollover contributions). This box shows proof that a requested rollover (including a direct rollover) from an IRA or qualified retirement plan (including the Thrift Savings Plan or TSP), was successfully rolled over, either directly or within 60 in the previous calendar year. The IRS will receive a copy of the 1099-R showing the distribution from either a qualified or IRA. Box 2 of Form 5498 is evidence that the distribution was subsequently rolled over and no federal income taxes are due. The following example illustrates:

Example 3. Richard took a $300,000 distribution from his traditional TSP in October 2025. He used the funds to make a downpayment on a new house. This withdrawal generated a 2025 1099-R. In November 2025, Richard sold his own home and uses the sale proceeds to roll $300,000 into his traditional IRA. This was within 60 days of the TSP distribution in October 2025. This rollover will generate a 2025 Form 5498 showing the $300,000 rollover in Box 2. Richard will report on his 2025 federal income tax return that the $300,000 was rolled and should not be taxable. The IRS will receive sometime in late May 2026 Form 5498 showing Richard’s nontaxable $300,000 rollover contribution.

- Box 3 (Roth IRA conversions amount. Every Roth IRA conversion will carry its own five-year clock determining if the distributions coming out of the converted Roth IRAs are subject to the IRS’ 10 percent early withdrawal penalty. Box 3 reports the total dollar amount of all Roth IRA conversions for the year completed under the authority of the IRA custodian who generates Form 5498. In addition, the tracking of each Roth IRA is recorded on Form 5498. In particular, a Roth IRA conversion is essentially time -stamped January 1 for the year noted on Form 5498. Add five years and a Roth IRA owner under age 59.5 will know exactly when those Roth IRA conversion dollars are available with no penalty. The following example illustrates:

Example 4. Sharon, age 45 and a federal employee, performed her first Roth IRA conversion in 2025 for $25,000. Sharon had not previously made any contributions to a Roth IRA. The $25,000 Roth IRA conversion generated a 1099-R showing the $25,000 distribution from Sharon’s traditional IRA. The conversion also produced a 2025 Form 5498 which reported $25,000 in Box 3. Any of Sharon’s Roth IRA conversions performed during 2025 receive a January 1,2025 starting date for the purpose of the “five-year” rule. Based on her 2025 Form 5498, Sharon knows she will have full access to the $25,000 of converted Roth IRA dollars, both tax- and penalty-free as of January 1, 2030. Sharon will have to wait until she is 59.5 in 2039 in order to withdraw income tax-free any of the earnings on her 2025 Roth IRA conversion.

If Sharon performs any more Roth IRA conversions in future years, then she will receive another Form 5498 in the year of each conversion. Sharon will know the precise amount of all her Roth IRA conversions, and when these specific conversion dollars are available income tax- and penalty-free by referring to the annual Form 5498 forms.

- Box 5 (Fair Market Value of account). The fair market value as of December 31,2025 of all investments in the IRA account is shown in Box 5. Perhaps the most important use of Box 5 information is to help accurately calculate the required minimum distribution (RMD) for traditional IRA owners. In order to determine an individual’s annual traditional IRA RMD, the traditional IRA owner must add up the prior-year end balances of all traditional IRAs owned, as shown in Box 5 of each Form 5498 received. That is, one Form 5498 for each traditional IRA owned with a different IRA custodian. The total is then divided by the applicable RMD factor.

- Box 10 (Roth IRA contributions). Similar to what is done for all Roth IRA conversions performed during the year, Roth IRA contributions for the year are shown in Box 10 of Form 5498. Roth IRA owners should be aware that there is no place on a Roth IRA owner’s federal income tax return to report a Roth IRA contribution. This leads to the questions: “How does the IRS know when an individual made his or her first Roth IRA contribution, thereby setting the five-year forever clock for making income-tax-free distributions of Roth IRA earnings? The answer is Box 10 of Form 5498 for the year a Roth IRA owner made his or her first Roth IRA contribution. The following example illustrates:

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

Example 5. Carlos, age 43, made his first Roth IRA contribution in 2008 in the amount of $2,000. Carlos received a 2008 Form 5498 from his IRA contribution indicating in Box 10 his Roth IRA contribution of $2,000. The $2,000 Roth IRA contribution was Carlos’ first Roth IRA contribution and also locks in his Roth IRA starting date for the “five-year forever” clock as of January 1, 2008. Carlos subsequently contributed $5,000 a year to his Roth IRA for the next 17 years (2009 – 2025) a total of $85,000. Carlos’ custodian continues to send Carlos and the IRS a new Form 5498 each year. In 2026, Carlos’ total Roth IRA balance is $175,000. Carlos needs cash to cover an emergency expense. By totaling the amounts in Box 10 of Form 5498 for all the years he contributed to his Roth IRA, Carlos determines that he has access to $87,000 ($2,000 plus $85,00) that is free-and-clear of any taxes or early withdrawal penalties. Note that a Roth IRA owner always has access to his or Roth IRA contributions, no matter the Roth IRA owner’s age. That means the Roth IRA owner can withdraw some or all of the Roth IRA contributions with no income tax consequences.

- Box 11 (Check if RMD for 2026). An “X” placed in Box 11 lets the IRS know which traditional IRA owners are subject to required minimum distributions during 2026. Note that while IRA custodians are required to notify the IRS of all traditional IRA owners who are subject to RMDs, they are not required to calculate the actual amount.

- Box 12a (RMD date). The date shown in Box 12a is the deadline by which the RMD amount in Box 12a must be distributed in order for the traditional IRA owner to avoid the missed RMD penalty resulting from the undistributed amount.

- Box 12b (RMD amount). If a traditional IRA owner is required to take a traditional IRA RMD, then the IRA custodian must notify the traditional IRA owner by January 31 of the RMD year. This obligation can be fulfilled by sending either Form 5498 ( with information shown in Box 12a and in 12b) by the date or providing a separate statement offering to calculate the RMD.

Traditional IRA owners should be aware that the amount shown in Box 12b may not be accurate for the following reasons: (1) Use of the wrong life expectancy table; (2) There may have been an outstanding rollover at the end of the year; and (3) Box 12b is indicative of the RMD for only the traditional IRA held with that IRA custodian. If the traditional IRA owner owns other traditional IRAs held with other institutions, then those traditional IRAs will have their own RMDs. Most importantly, a traditional IRA custodian is not obligated to properly calculate an RMD. That responsibility belongs to the traditional IRA owner.

- Box 13a, 13b, and 13c (Postponed/late contribution; year; code). Late rollovers (that is, beyond the normal 60-day rollover window) may be accepted by the IRS. This is done by the traditional IRA owner providing the receiving financial institution with “self-certification” as to the reason for the late rollover. Form 5498 requries the late rollover information to be included in Boxes 13a,13b and 1c. The “Code” shown in Box 13c include: (1) FD-extension of the contribution due date because of a federal designated disaster; (2) PO – a rollover of a qualified retirement plan or TSP loan offset; and (3) SC – the self-certification procedure for a late rollover contribution.

- Box 15a (Fair Market Value of certain specified assets). IRA owners can purchase unconventional assets in their accounts without creating a prohibited transaction. The IRA owner’s challenge, however, is to place a value on alternative assets. Frequently, it is up to the IRA owner to provide an accurate annual valuation of nontraditional investments to the custodian who ultimately reports the value in Box 15a of Form 5498. Note that if the IRA custodian fails to receive a fair market value and leaves Box 15a blank, this could raise a red flag with the IRS.

- Box 15b (Codes). If unusual or hard-to-value investments are held in an IRA and if Box 15a reports a value, the IRS will want to know what the investment is. Box 15b provides several codes for clarification. For example, Code C is for ownership interest in an LLC, and Code D is for real estate.

Form 5498 has additional information about recharacterized IRA contributions (Box 4), the type of IRA (Box 7) and details about any repayment of a distribution taken for allowable reasons such as a qualified disaster, birth or adoption, or withdrawal by a terminally ill individual (Box 14a and 14b).

IRA owners who have problems or questions concerning the information shown on their Form 5498 are advised to speak with a tax professional who is knowledgeable in retirement plans and IRAs.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

TSP: The Thrift Savings Plan (TSP) is a retirement savings and investment plan for Federal employees and members of the uniformed services, including the Ready Reserve. The TSP is a defined contribution plan, meaning that the retirement income you receive from your TSP account will depend on how much you (and your agency or service, if you're eligible to receive agency or service contributions) put into your account during your working years and the earnings accumulated over that time. The Federal Retirement Thrift Investment Board (FRTIB) administers the TSP.

RMDs: RMD's are generally subject to federal income tax and may be subject to state taxes. Consult your tax advisor to assess your situation.

IRAs: Contributions to a traditional IRA may be tax-deductible depending on the taxpayer’s income, tax-filing status, and other factors. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty.

Roth IRA: Like Traditional IRAs, contribution limits apply to Roth IRAs. In addition, with a Roth IRA, your allowable contribution may be reduced or eliminated if your annual income exceeds certain limits. Contributions to a Roth IRA are never tax deductible, but if certain conditions are met, distributions will be completely income tax free. Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted.

Roth Conversions: Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Additionally, each converted amount may be subject to its own five-year holding period. Converting a traditional IRA into a Roth IRA has tax implications. Investors should consult a tax advisor before deciding to do a conversion.

You Might Also Enjoy This Podcast

Ed Zurndorfer, EA, ATA, CFP®, CLU®, ChFC®, CEBS®, ChFEBC℠: Federal Employee Benefits Expert

A former career Federal employee, Ed has published a staggering 1,200+ separate articles on Federal Benefits and Retirement!

Just “Google” his name, and you are likely to find a plethora of sites that contain his writings. Drawn to its mission to reach, teach

and serve Feds, Serving Those Who Serve is the only financial planning practice with which Ed has chosen to affiliate in over

20 years teaching. In addition to conducting Federal Benefits seminars for Serving Those Who Serve, you can find Ed’s

writings here on our blog in the FedZone, and on Fed-Soup, MyFederalRetirement, FederalNews Radio and NITP.

He is a member of the Maryland Society of Accountants, the National Association of Enrolled Agents, the International Society of Certified Employee Benefits Specialists, the Financial Planning Association, the National Association of Health Underwriters,

and the Society of Financial Service Professionals. Since 1999, Ed has taught many thousands of Federal employees about

their benefits, in person and at Federal agencies all over the country. Ed is a true national treasure.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.