Those federal employees and retirees who owe additional federal income taxes when they file their 2024 federal income tax returns may have to make federal estimated tax payments during 2025.

Federal employees can use the general rule below as a guide to determine if they have enough federal income tax withholding or should increase federal income tax withholding from their salaries or retirement income (CSRS or FERS annuities, Thrift Savings Plan withdrawals and Social Security monthly benefit payments) whether or not to make federal estimated tax payments during 2025.

General rule for making federal estimated tax payments.

An individual should make federal estimated tax payments during 2025 if both of the following circumstances apply:

- The individual expects to owe at least $1,000 in federal income taxes for 2025 after subtracting the individual’s federal income tax withholding and tax credits.

- The individual expects their federal income tax withholding and tax credits to be less than the smaller of: (a) 90 percent of their 2025 federal income tax liability; or (b) 100 percent of their 2024 federal income tax liability as shown on their 2024 federal income tax return.

Note that if most of an individual’s potentially taxable income - this includes salary income, pension income, traditional IRA income and Social Security income - will be subject to federal income tax withholding, then the individual probably does not have to make federal estimated tax payments.

Married individuals

If an individual is married and therefore qualifies to make joint estimated tax payments, then the rules discussed here apply to the joint income of the individual and their spouse. The individual and their spouse can make joint estimated tax payments even if they are not living together.

However, an individual and their spouse cannot make joint estimated tax payments if any of the following circumstances apply:

- They are legally separated under a decree of divorce or separate maintenance.

- They have different tax years, or

- Either spouse is a nonresident alien, unless that spouse has elected to be treated as a resident alien for tax purposes.

Note that individuals who are in registered domestic partnerships, civil unions, or other similarly formed relationships that are not marriages under state law cannot make joint estimated tax payments. These individuals can take credit only for the estimated tax payments that he or she makes.

“Household” employers

Those individuals who are “household” employers – they employ a caretaker, a babysitter or as a nanny – should include household employment taxes (federal income tax, Social Security and Medicare Part A payroll taxes) they withhold, if either of the following applies:

- The individual will have insufficient federal income tax withheld from wages, pensions, annuities, gambling winnings, or other income in order to pay the household employment federal taxes.

- The individual would be required to make estimated tax payments to avoid a penalty even if the individual did not include household employees when figuring their federal estimated tax payments.

Higher income individuals

If an individual’s adjusted gross income (AGI) was more than $150,000 ($75,000 if an individual’s filing status for 2025 is married filing a separate return), then the 100 percent of the federal income tax liability shown on their 2024 federal income tax liability should be replaced with 110 percent.

For 2024, AGI is the amount shown on IRS Form 1040 or Form 1040-SR, line 11.

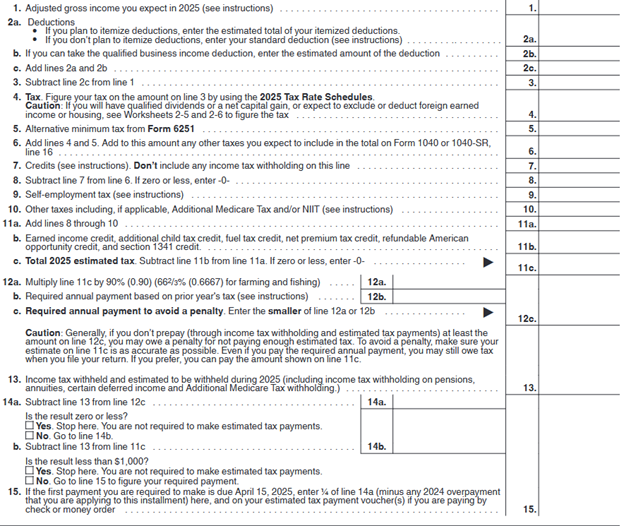

How to figure 2025 estimated tax payments

To calculate federal estimated tax payments, an individual must calculate their expected AGI for the year, taxable income for the year, federal income taxes deducted and any federal tax credits. When computing 2025 estimated tax, it may be helpful to use 2024 federal income tax deductions and federal tax credits as a starting point. An individual’s 2024 federal income tax return therefore should be used as a guide.

Learn more about your retirement benefits at our No-Cost webinars, featuring Ed Zurndorfer -

The following worksheet from IRS Publication 505 (Tax Withholding and Estimated Tax) can be used to determine 2025 federal estimated tax payments:

When to pay federal estimated tax

For estimated tax payments, the year is divided into four payment periods. Each period has a specific estimated tax payment due date. If an individual does not pay a sufficient amount of estimated federal income tax by the due date of each of the payment periods, the individual may be subject to an under withholding penalty. This is the case even if the individual is due to receive a refund when the individual files their federal income tax return the following spring.

If a federal estimated tax payment is mailed to an IRS Service Center, then the postmark date is considered the date of payment. The general payment periods and due dates for 2025 federal estimated tax payments are presented in the following table:

|

For the payment period |

Due Date |

Tax Year 2025 Due Dates |

| January 1 – March 31

April 1 – Mary 31 June1 – August 31 September 1 - December 31 |

April 15

June 15 September 15 January 15 of the next year |

April 15, 2025

June 16, 2025 September 15, 2025 January 15, 2026 |

When to start making federal estimated tax payments

An individual does not have to make federal estimated tax payments until the individual receives a significant amount of taxable income in which there is little or no federal income tax withholding. For example, if an individual sells an investment capital asset (for example, a stock) at a huge capital gain in in May 2025, then the individual will likely have to make an estimated tax payment that is due no later than June 16, 2025.

Individuals have several options when paying federal estimated taxes. An individual can: (1) Apply an overpayment from the previous year; (2) Pay all the estimated tax by the due date of the first estimated tax payment; or (3) pay in installments.

To avoid any estimated tax penalties, all installments must be paid by their due date and for the required amount.

State estimated tax payments.

Those individuals living in states with state and local income taxes are advised to ask about their state requires estimated tax payments. Similar to federal estimated tax payments, an individual who is in receipt of taxable income in which there is no state income tax withholding may have to make state estimated tax payments. Like the IRS, state tax and revenue departments impose penalties for under withholding of state and local income taxes.

Federal employees and retirees who have questions about their 2025 federal and state income tax withholding from their salaries, CSRS or FERS annuities, the Thrift Savings Plan and Social Security payments are advised to talk to their tax advisors.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

You Might Also Enjoy This Podcast

Ed Zurndorfer, EA, ATA, CFP®, CLU®, ChFC®, CEBS®, ChFEBC℠: Federal Employee Benefits Expert

A former career Federal employee, Ed has published a staggering 1,200+ separate articles on Federal Benefits and Retirement!

Just “Google” his name, and you are likely to find a plethora of sites that contain his writings. Drawn to its mission to reach, teach

and serve Feds, Serving Those Who Serve is the only financial planning practice with which Ed has chosen to affiliate in over

20 years teaching. In addition to conducting Federal Benefits seminars for Serving Those Who Serve, you can find Ed’s

writings here on our blog in the FedZone, and on Fed-Soup, MyFederalRetirement, FederalNews Radio and NITP.

He is a member of the Maryland Society of Accountants, the National Association of Enrolled Agents, the International Society of Certified Employee Benefits Specialists, the Financial Planning Association, the National Association of Health Underwriters,

and the Society of Financial Service Professionals. Since 1999, Ed has taught many thousands of Federal employees about

their benefits, in person and at Federal agencies all over the country. Ed is a true national treasure.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street - Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.