Understanding How Federal Employee Retirement Benefits are Taxed by the IRS – Part III- This column discusses the taxation of survivor benefits received by designated beneficiaries of deceased federal employees and retirees.

Edward A. Zurndorfer

This is the third of a series of FEDZONE columns discussing how federal employee retirement benefits are taxed by the IRS. This column discusses the taxation of survivor benefits received by designated beneficiaries of deceased federal employees and retirees.

Unpaid Compensation of a Deceased Federal Employee

Unpaid compensation (which includes salary/wages and unused annual leave hours) of a federal employee who died while in federal service and paid to the deceased employee’s designated beneficiary (designated on Form SF 1152 Designation of Beneficiary – Unpaid Compensation of a Deceased Civilian Employee) after the employee’s death is considered “income in respect of the decedent” and therefore fully taxable to the beneficiary recipient. The beneficiary should receive a W-2 or 1099-NEC from the deceased employee’s payroll processing office showing the amount of reportable taxable income. The beneficiary must report the income shown on their federal and state income returns.

Dependents of Deceased Public Safety Officers

The Public Safety Officers’ benefits program provides a tax-free death benefit to eligible survivors of federal public safety officers whose death is the direct and proximate result of a traumatic injury sustained in the line of duty. The death benefit is not includable in the decedent’s gross estate for federal or state estate tax purposes, nor is the death benefit included in the survivors’ gross income for federal income tax purposes.

A public safety officer is a law enforcement officer, firefighter, or member of a public rescue squad or ambulance crew. In certain circumstances a chaplain killed in the line of duty is also a public safety officer. The chaplain must have been responding to a fire, rescue or police emergency as a member or employee of a fire or police department.

The program is administered through the Bureau of Justice Assistance.

FERS Spousal Lump Sum Death Benefit Payment

A spouse of a deceased FERS employee who died in federal service (with at least 18 months of federal service) is entitled to a special death benefit in the form of a lump sum death benefit payment. The surviving spouse has the option of taking the lump sum death benefit in the form of a single payment or in the form of an annuity payable over a three-year period.

If the surviving spouse chooses the single payment option, then the following rules apply with respect to taxation:

- If a FERS survivor annuity is not paid, then at least part of the special death benefit is tax-free. The tax-free portion is equal to the deceased employee’s FERS contributions made via payroll deduction to the FERS Retirement and Disability Fund. These retirement contributions the deceased employee (made bi-weekly via payroll deduction to the FERS Retirement and Disability Fund) were made with after-taxed dollars.

- If a FERS spousal survivor annuity is also paid, then all of the special death benefit is taxable. The surviving spouse cannot allocate any of the deceased employee’s FERS retirement contributions to the special death benefit.

- If the surviving spouse chooses the three-year annuity payout option, then at least part of each monthly payment is tax-free, according to the following rules:

- If a FERS spousal survivor annuity is not paid, then the tax-free portion of each monthly payment is an amount equal to the deceased employee’s FERS contributions divided by 36.

- If a FERS survivor annuity is also paid, then the employee’s FERS contributions are allocated between the three-year annuity and the survivor annuity. The allocation is made in the same proportion that the expected return from each annuity bears to the total expected return from both annuities. The amount allocated to the three-year annuity is divided by 36. The result is the tax-free part of each monthly payment of the three-year annuity.

CSRS or FERS Spousal Survivor Annuity

Any survivor spouse of a deceased federal employee or annuitant who receives a spousal CSRS or FERS survivor annuity will recover the deceased spouse’s “cost” in the deceased spouse’s retirement income tax-free. The “cost” in the deceased employee or annuitants are CSRS or FERS contributions made while in federal service. The amount that the surviving spouse receives back tax-free each month depends on when the deceased spouse died, namely, while in federal service or after retiring.

Another factor that will affect the amount of the tax-free portion of a CSRS or FERS survivor annuity for a surviving spouse is whether there are any surviving children receiving “children survivor benefits” in the form of a monthly child survivor annuity paid by OPM. A child or multiple children under the age of 18 of a deceased federal employee or a federal annuitant are eligible for a monthly annuity from OPM until they are age 18. If an eligible child reaches age 18 and then attends a college or university full-time, then the monthly annuity continues until the child becomes age 22 provided the remains a full-time student. The following two situations with respect to the tax consequences of a surviving spouse receiving a survivor annuity are presented:

Situation #1. Surviving spouse with no eligible children receiving a survivor annuity following the death of their spouse who died after retiring from federal service and was receiving a CSRS or FERS annuity.

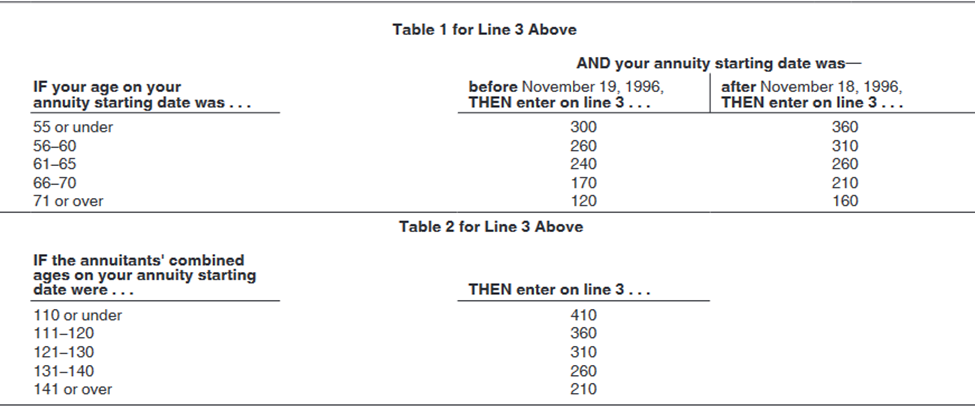

In the situation of a spouse named as the survivor annuitant of a CSRS- or FERS-covered retiree (who died after retiring from federal service), then the same monthly/annual amount of the deceased spouse’s CSRS or FERS annuity that was not taxable (according to the Simplified Method) applies to the spouse’s survivor annuity and therefore not be taxable. That amount was determined by the Simplified Method based on the retired employee’s total contributions to the CSRS or FERS Retirement and Disability Fund and the combined ages of the employee and spouse in the year the first CSRS or FERS annuity check was paid. Each annuity and survivor annuity payment contains a portion of what the employee had contributed to either the CSRS or FERS Retirement and Disability Fund on an after-taxed basis and therefore is not taxable. In short, the monthly payment returns a return of the employee’s “cost” in the employee’s CSRS or FERS retirement. The surviving spouse will continue to exclude the same amount from his or her monthly survivor annuity until the number of months has been attained according to Table 2 of the Simplified Method. That number of months was determined according to the combined ages of the annuitant and the survivor annuitant in the year that the annuitant received his or her first annuity check.

For informational purposes, both Table 1 and Table 2 from the IRS’ Simplified Method Worksheet in IRS Publication 721 (Tax Guide to U.S. Civil Service Retirement Benefits) is reproduced here:

The following example illustrates:

Example 1. (Same example from Part II of this series at https://stwserve.com/how-federal-retirement-benefits-are-taxed-part-ii/. Catherine retired from federal service under FERS on March 31, 2020. Catherine is married to Ken and elected to give Ken a full survivor annuity. Using the Simplified Method, Catherine determines that $72.40 of her monthly FERS annuity, or $869 per year, is a return of her $22,443 cost in the FERS retirement. Based on Catherine’s and Ken’s ages in the year 2020 when Catherine retired. The $72.40 monthly amount will continue to be paid and not taxable until 310 monthly payments have been made.

Unfortunately, Catherine died on December 20, 2021, and Ken became a survivor annuitant effective Dec. 21, 2021, with his first FERS survivor annuity check paid Jan. 1, 2022. At the time of her death Catherine was receiving a gross monthly survivor annuity of 50 percent, his starting monthly FERS survivor annuity is 50 percent of $4,021 ($2, 011) of which $72.40 is tax-free.

Situation #2. Surviving spouse with no eligible children receiving a survivor annuity following the death of a spouse who died in federal service with at least 10 years of federal service at the time of his or her death.

A surviving spouse of a federal employee who died while in federal service with at least 10 years of federal service is entitled to a spousal survivor annuity. The question is: How does the surviving spouse determine the tax-free recovery of the deceased employee’s “cost” in the CSRS or FERS retirement plan? The following discussion explains how the “cost” in the retirement is recovered.

For all spousal survivor annuities commencing after Nov. 18, 1996, the Simplified Method is used to determine the tax-free monthly portion of the survivor annuity. Under the Simplified Method, each of the monthly survivor annuity payments is made up of two parts:

- The tax-free part portion which is a return of the deceased employee’s “cost in their CSRS or FERS retirement plan; and

- The taxable portion that is the amount of each payment that is more than the portion that represents the employee’s “cost” in the retirement plan. The tax-free portion remains the same, even when the survivor annuity is increased by cost-of-living adjustments (COLAs). The following example illustrates:

Example 2. Steve was married to Olivia, a federal employee. Olivia died while in federal service at the age of 48 on July 25, 2021, with 18 years of federal service. At the time of Olivia’s death, Steve was also 48 years old. Olivia had contributed while in federal service (via payroll deduction) a total of $14,125 to the FERS Retirement and Disability Fund. Steve’s survivor annuity starting date was July 26,2021 and his first FERS survivor annuity check of $2,242 was paid on August 1, 2021. He received five survivor annuity checks of $2,242 each between Aug. 1, 2021 and Dec. 31, 2021, a total of five times $2,242, or $11,210. The $11,210 is the total amount of Steve’s gross spousal survivor annuity that he received during 2021. Steve wants to know the amount of his taxable spousal survivor annuity during 2021. To do so, Steve must use the Simplified Method. The following is Steve’s worksheet using the Simplified Method:

- 1. Total gross annuity received during 2021 = $11,210

- 2. Starting date of annuity = 8/01/2021

- 3. Retirement plan “cost” = $14,125

- 4. Age of survivor annuitant at annuity starting date = 48

- 5. Age factor (payment months) (Table 1, Simplified Method Worksheet) = 360

- 6. Divide Line 3 by Line 5 = $39.24

- 7. Number of months payments were made during 2021= 5

- 8. Multiply Line 6 by Line 7 = $196

- 9. Taxable portion of survivor annuity received during 2021 = $11,014 (line 1 less line 8)

- 10. Amounts previously recovered after 1986 = $0

- 11. Cost in plan remaining at beginning of 2022 = $13,929 (Subtract Line 8 from Line 3)

Note: Steve received the first 5 survivor annuity payments during 2021. There are 355 more monthly survivor annuity payments to be paid in which $39.24 will not be taxable. If Steve lives to receive the remaining 355 payments (a total of 360 payments), then he would have recovered all $14,125 of Olivia’s “cost” in the FERS retirement. Starting with his 361st monthly payment (assuming Steve lives to that time), Steve’s monthly survivor annuity payment will be fully taxable because at that point Olivia’s “cost” in the FERS retirement has been fully recovered.

Steve’s taxable survivor annuity for the year 2021 is therefore $11,014. Each year Steve will subtract $196 from the amount of the gross annuity he received that year in order to determine the taxable survivor annuity for that year.

Note: For most retiring federal employees, OPM’s Retirement Office does in fact calculate the taxable portion of a retired federal employee’s CSRS or FERS annuity throughout the retired employee’s years as a CSRS or FERS annuitant. On an annuitant’s CSA-1099R, both the “gross distribution” and the “taxable amount” will appear in separate boxes. However, that is not the case with a spousal survivor annuity. On a surviving spouse’s CSF 1099-R (reporting the survivor annuitant’s survivor annuity received during the year), OPM reports the “gross distribution” in one box of the CSF 1099-R but puts the word “UNKNOWN” in the box that reports the “taxable amount” of the survivor annuity. This means it is up to the survivor annuitant to determine the taxable portion of the survivor annuity received. Spousal survivor annuitants who prepare their own federal and state income tax returns should be aware of this. They will have to determine the taxable portion of their survivor annuity themselves, using the Simplified Method together with the information provided in IRS Publication 721 and in this column to assist them. Those spousal survivor annuitants who use the services of tax professional to prepare their federal and state income tax returns should make their tax preparers aware of the fact that the tax preparer will have to determine the taxable portion of the spousal survivor annuity.

PART VI >

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.